Estimated reading time: 7 minutes

Until week 39 of 2023, prices on the country’s fresh produce markets (FPMs) had consistently been on the rise, reaching unprecedented highs. Subsequently, a phase of stabilisation followed, characterised by sporadic price hikes in specific weeks and an overall acknowledgement of declining prices by the end of week 46.

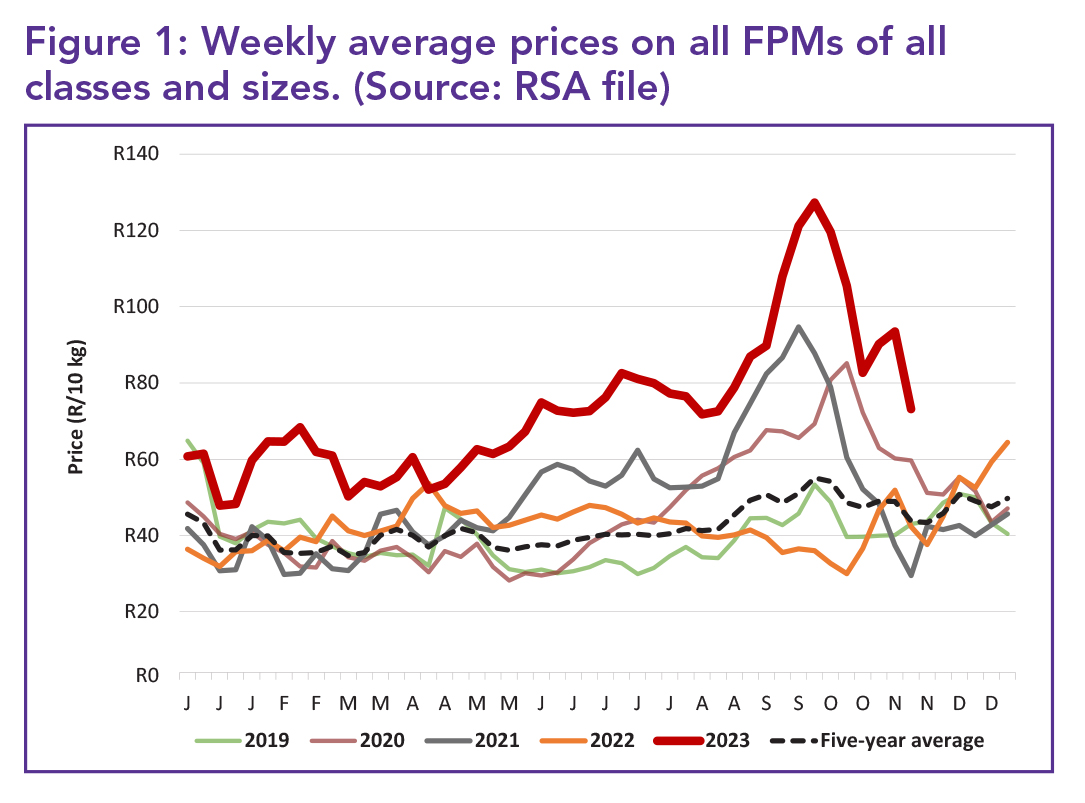

Figure 1 portrays the weekly average prices for a 10 kg bag of potatoes that had reached R73.15 at the conclusion of week 46. Since the start of October, the average prices showed a decline, dropping from R127.29 to R82.70 by the final week of October. However, in the first two weeks of November, prices rose to R93.48, only to drop again to R73.15 by the 46th week.

This overall decrease of 42.5% from week 40 to 46 coincided with an increase in deliveries, attributable to regions such as the Eastern Cape entering the market season.

Additionally, there was a modest increase in deliveries from the Sandveld during October. Although there was an increase in deliveries, it was still lower than the previous year, resulting in a significant shortfall of 1 454 546 x 10 kg bags in the current year for the same period.

Daily levels and prices

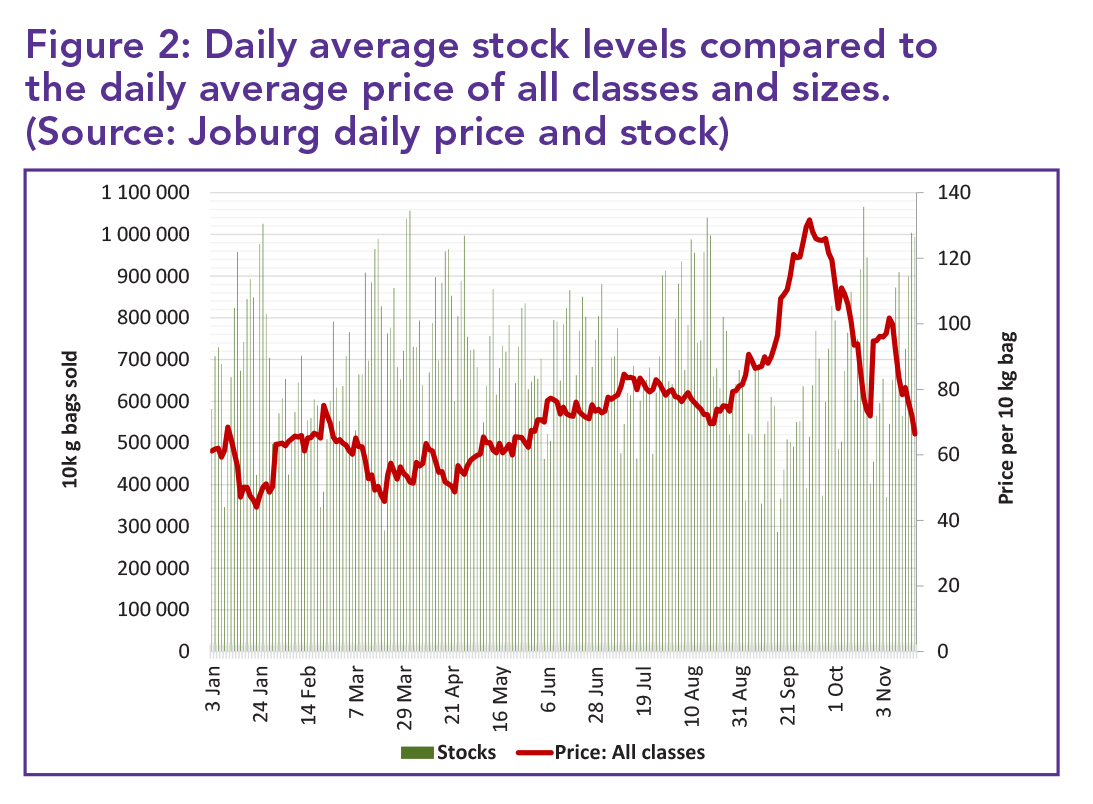

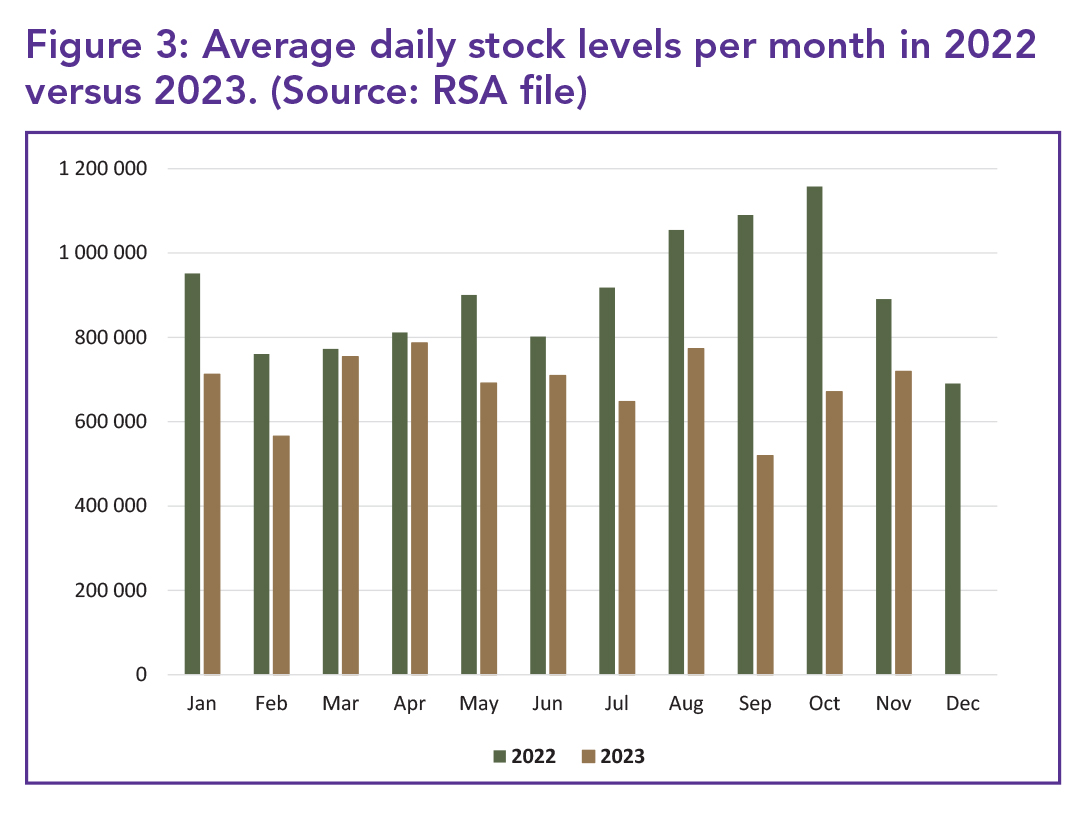

Figure 2 illustrates the daily average stock levels and corresponding daily average prices for the first 46 weeks of 2023. In turn, Figure 3 provides a comparative analysis of the average stock levels for each month as opposed to the corresponding months of the previous year. In November, daily average stock levels across all national FPMs amounted to 719 000 x 10 kg bags, a decline of 171 000 bags compared to the same month last year and an increase of 483 000 bags compared to October 2023.

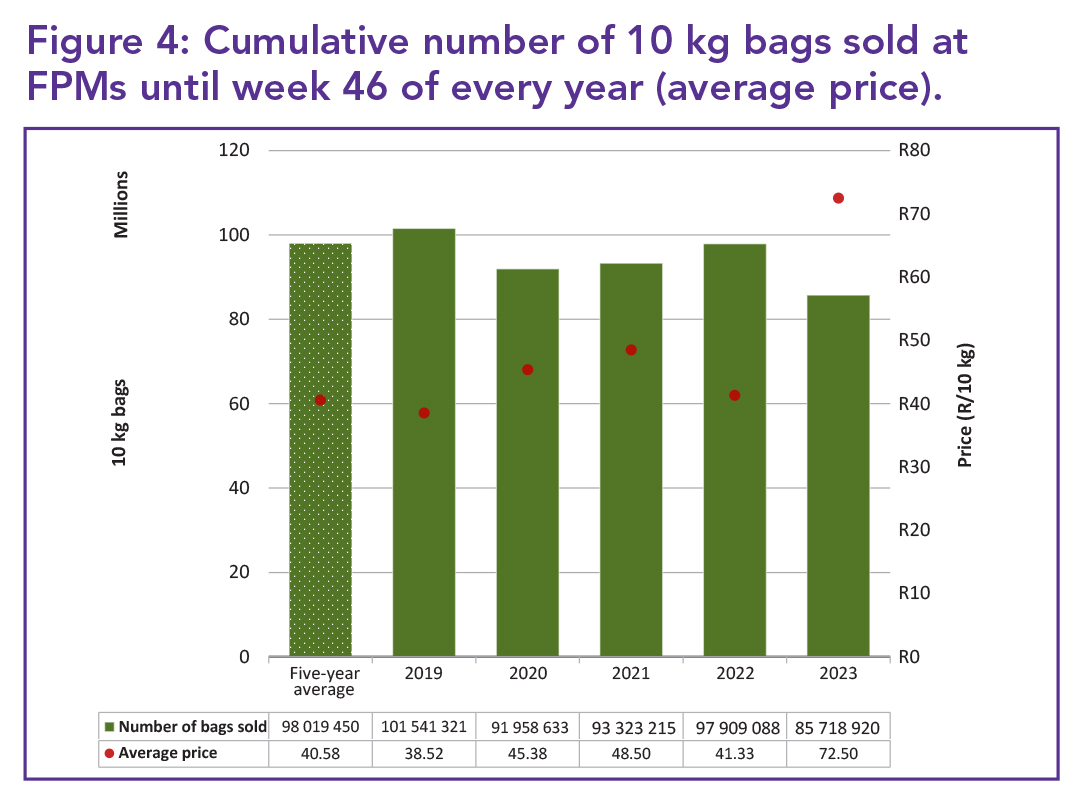

Figure 4 outlines sales performance on the FPMs throughout 2023, showing a 12% decrease compared to the corresponding figure in 2022. In addition, Figure 4 provides insight into the average prices over the same 46 weeks, revealing that the average price in 2023 had reached its highest point in the past five years. Moreover, sales on the FPMs after the first 46 weeks of 2023 were 12 million 10 kg bags less than the five-year average. At the time of writing it was anticipated that the lagging effect due to the various challenges faced throughout the year would persist until year-end.

Potato sales

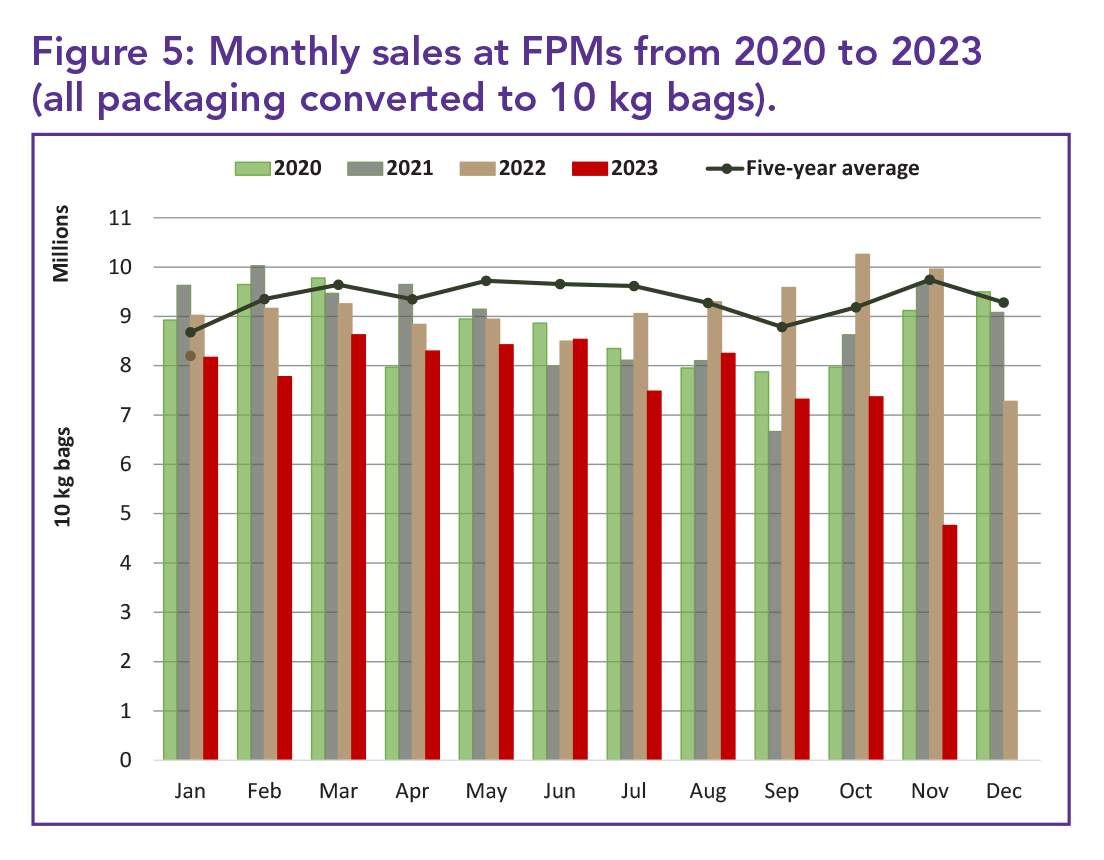

Figure 5 provides an overview of the monthly sales at the FPMs starting 2020 to date. In November, sales dropped below the eight million 10 kg bags threshold to 4.7 million 10 kg bags, compared to October’s sales of 7.3 million 10 kg bags and September’s sales of 7.3 million 10 kg bags. When comparing November 2023 with those of November 2022, a significant decrease of 52% is observed. However, it was anticipated to increase slightly by the end of November 2023.

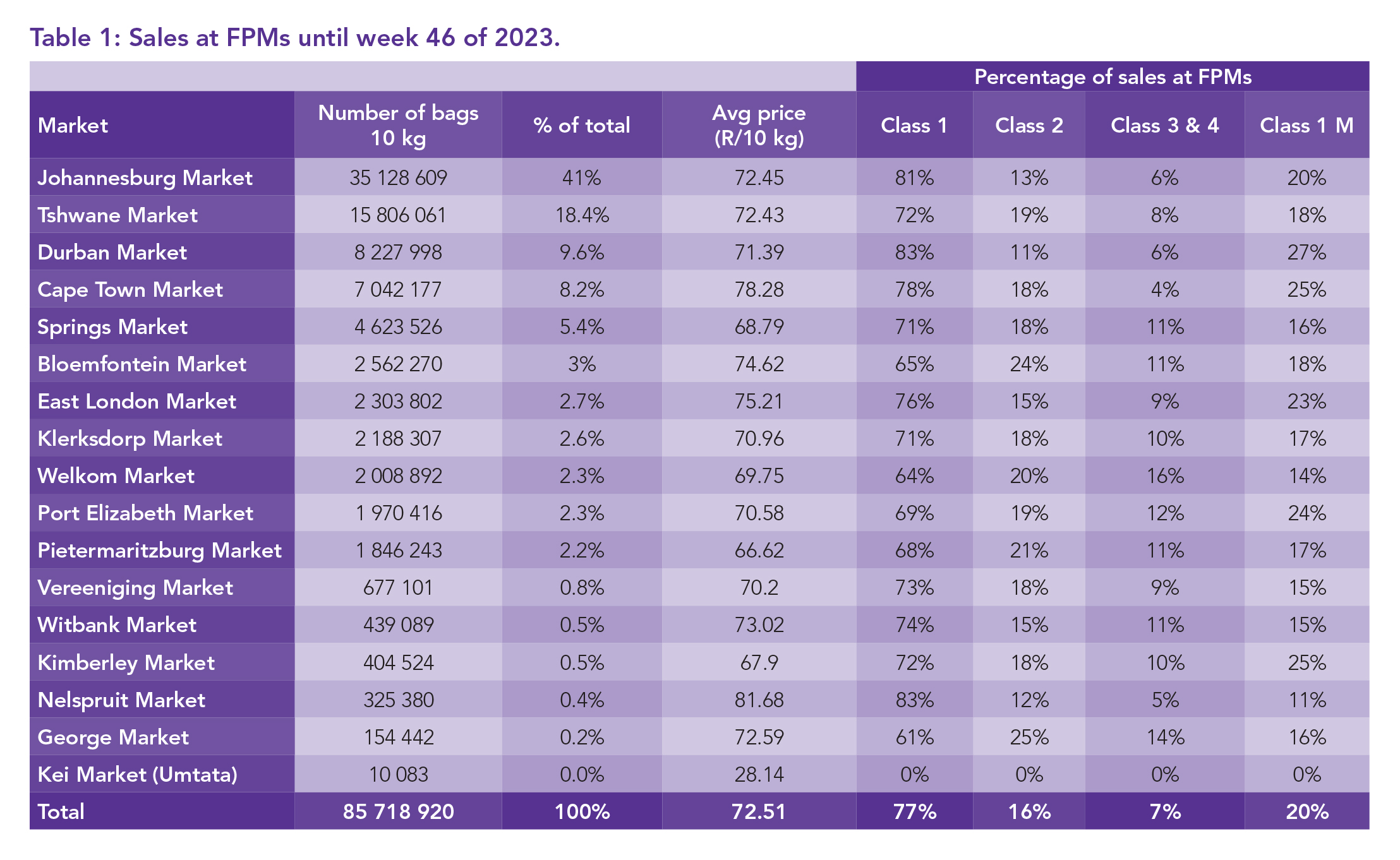

Table 1 contains the number of bags sold by the various FPMs during the initial 46 weeks of 2023. A detailed examination of sales performance across regions in 2023 reveals a mixed picture.

The five leading FPMs during this period collectively accounted for 83% of total FPM sales. The average price for each market, encompassing all classes and sizes, is also outlined in Table 1.

Among the top five FPMs, Durban and Springs markets exhibited average prices that were R1.19 and R3.72 lower respectively than the countrywide average yearly price of R72.51. In terms of market composition, Durban and Johannesburg markets showed the highest proportion of Class 1 bags in their total sales, accounting for 83 and 81% respectively, representing the highest percentages among the top five markets.

Price fluctuations and sales

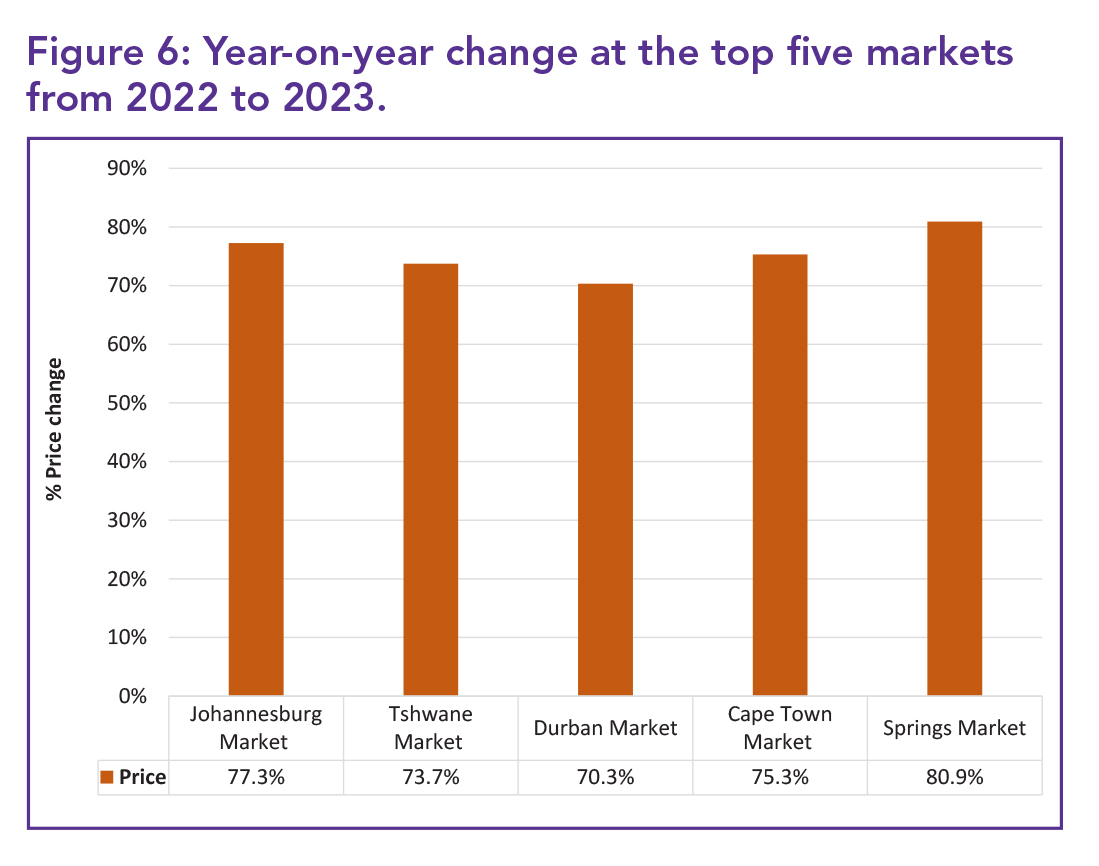

Figure 6 provides insights into the year-on-year price fluctuations of the leading five markets. In all these markets, prices escalated by more than 50% compared to the same period the previous year. Notably, the Springs market witnessed the most pronounced percentage surge, registering a price increase of 80.9%.

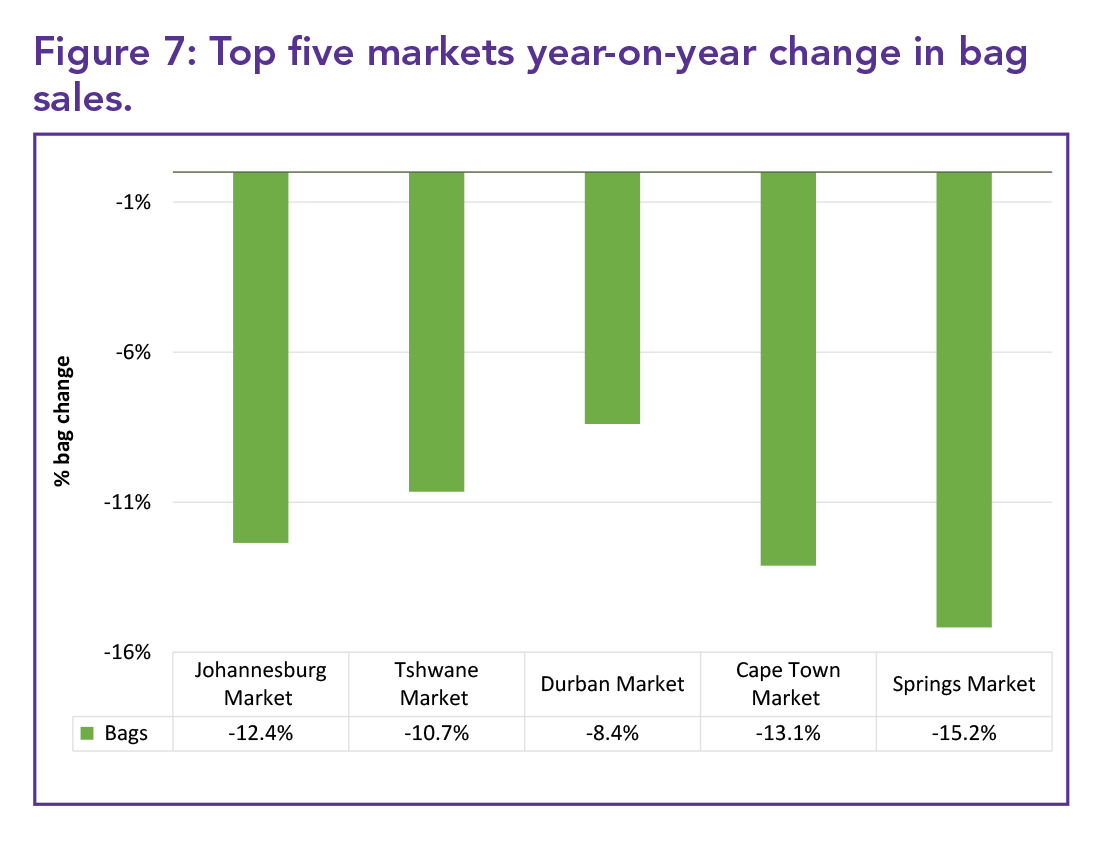

Conversely, Figure 7 depicts the year-on-year fluctuations in sales volumes across the top five markets. The Durban market stands out as the sole market that demonstrated the least decline in sales during the same period compared to the previous year. The Springs market, on the other hand, displayed the biggest decrease year-on-year among the top five markets.

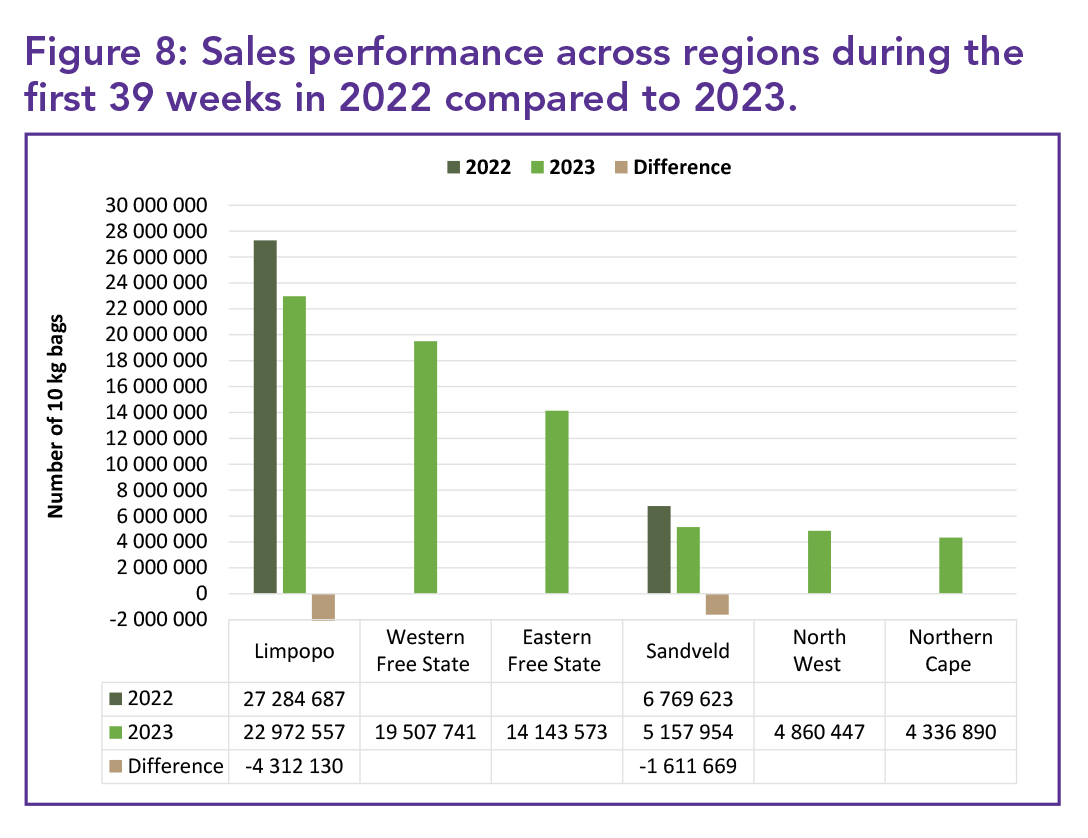

In Figure 8, a comprehensive view of sales performance across various regions in 2023 compared to 2022 unveils an intriguing pattern. Five regions experienced a decline in sales of 10 kg bags on the FPMs, while the Northern Cape was the only region that witnessed an upswing in sales during the first 46 weeks of 2023. This divergence highlights the diverse trends that played out across regions within this period.

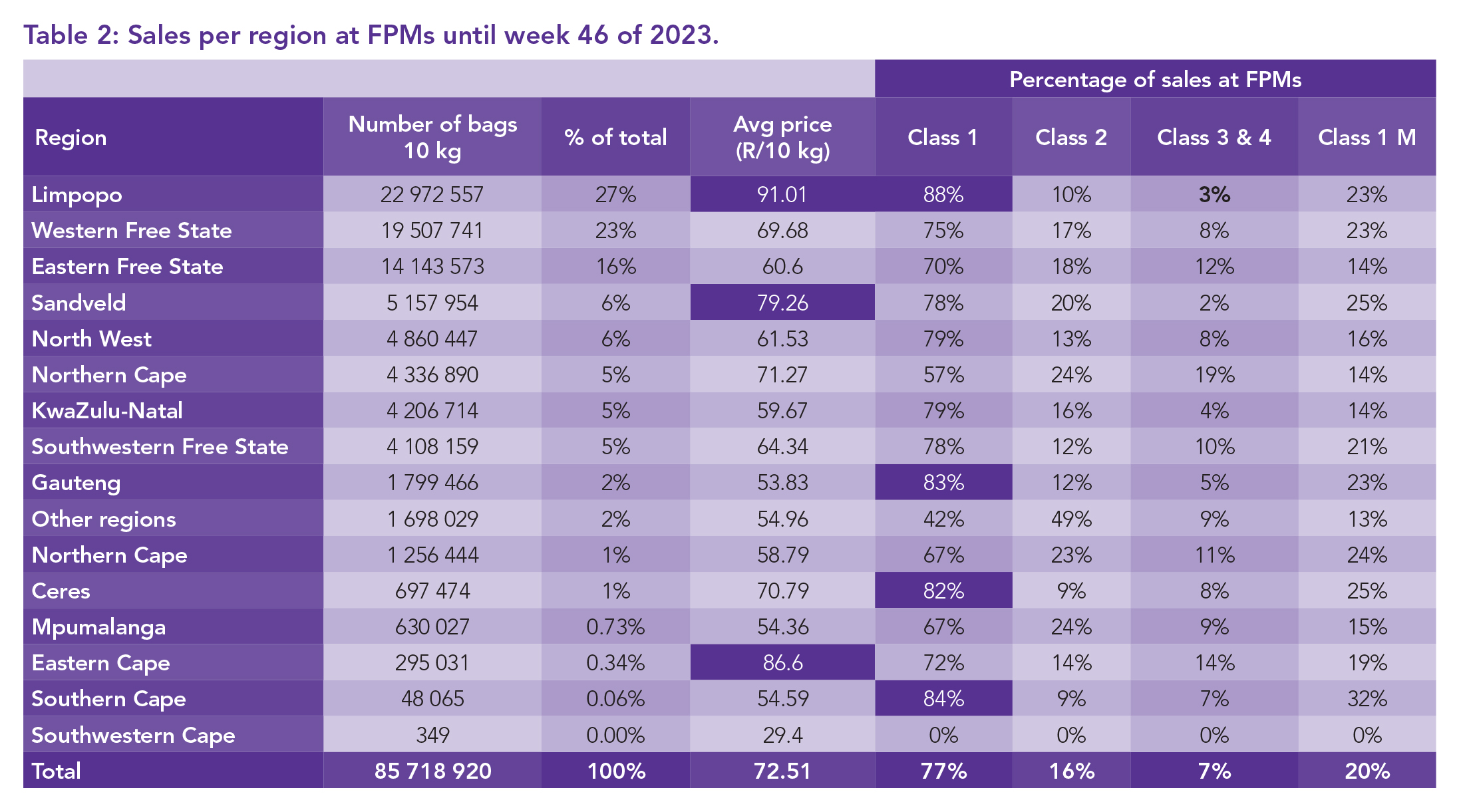

In terms of market presence on the FPMs, Limpopo, the Western Free State, and Eastern Free State – the three largest regions in terms of share during the initial 46 weeks – accounted for 66% of overall potato sales, as detailed in Table 2.

Additionally, Table 2 depicts the percentage composition of Class 1, 2, 3, and 4 potato supplies for each region during this period.

Noteworthy is the observation that in November, Class 1 sales constituted 77% of total sales. This signifies a positive trend in marketing superior quality potatoes. Among the production regions, 12 recorded Class 1 sales percentages exceeding the 70% threshold. Limpopo led the way with the highest percentage of Class 1 sales at 88%, followed by the Southern Cape (84%) and Gauteng (83%). – Lynné Roos, Sibabaliwe Rulumeni and Dikgetho Mokoena, Potatoes SA

For more information, send an email to Lynné Roos at lynne@potatoes.co.za or visit www.potatoes.co.za.