Estimated reading time: 16 minutes

While it is the world’s largest importer of potatoes, the United States (US) is neither the world’s largest producer nor its largest exporter of the commodity. Yet, developments in the country have a disproportionate impact on the global market due to its political and economic dominance.

The unpredictable policies of President Donald Trump are affecting the potato market. For one, it has contributed to a weakening of the US dollar, making American exports cheaper. While this has not increased demand for US potato products, sales have at least held steady in the face of greater competition from countries such as China and India. This competition is particularly evident in Japan, where general demand is up and the US, China, and India are all benefitting.

US tariffs are a headache for European shippers, whereas Canada enjoyed a good November with its continued tariff-free access to the US boosting its sales. The volume of the European potato surplus is becoming increasingly clear, with large volumes failing to stimulate additional usage in the Netherlands, and both France and Germany having surpluses of around one million tonnes each.

United States

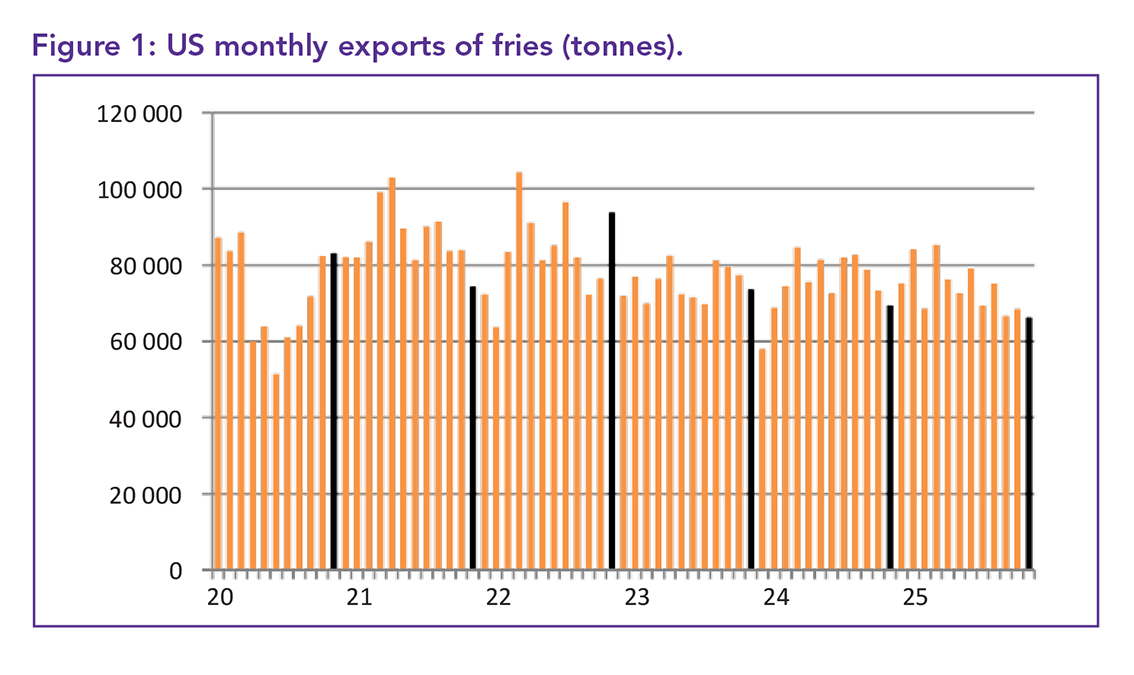

November fry exports from the US fell, but not dramatically. At 66 076 tonnes, they were the lowest since December 2023, the lowest November since 2014, and 2 172 tonnes below the previous month.

Despite this, the average export price of US$1 640/t (€1 384) was only US$13 lower than at the start of the year, continuing to hold a line against a price-sliding international market.

Sales to three of the US’s main markets – Mexico, Canada and South Korea – showed little change, while sales to Japan rose by 760 to 20 728 tonnes, about 8.6% higher than a year ago. November’s Japanese price of US$1 608/t (€1 357) was 2.8% lower than the year before, and US$7 higher than in October. Despite competition from China, US sales to Japan for the year reached 261 664 tonnes, 5.6% higher than in 2025.

Annual sales to Mexico and South Korea were down. Mexico’s fell 14.2% to 188 580 tonnes. November’s business was 30% lower at 12 183 tonnes, though unchanged from the previous month. At US$1 606/t (€1 355), the price was US$23 higher than in October. South Korea’s price was US$1 656/t (€1 397), US$2 higher than October.

The Philippines enjoyed a US$34 price cut and was able to buy at US$1 669/t (€1 408), while increasing its order by 834 tonnes to 2 571, which is 8.2% higher than the previous year. Sales to Taiwan, however, fell by 678 tonnes to 2 952, despite its price being US$37 lower at US$1 687/t (€1 423).

Canadian sales dipped by 368 tonnes to 5 312, accompanied by a US$43 discount, bringing the price to US$1 287/t (€1 086). Saudi Arabia saw its price lower by US$15 to US$1 649/t (€1 391), which is still 1% higher than the year before, with its sales holding at 1 837 tonnes. Kuwaiti sales slipped by 173 tonnes to 537, while exports to the United Arab Emirates (UAE) rose by 55 tonnes to 178.

Sales to El Salvador were 483 tonnes lower at 917, Costa Rica fell by 3 240 tonnes to 639, and Guatemalan sales were 176 tonnes lower at 3 396. Prices in these countries fell between 2.6 and 6.2% over the past year.

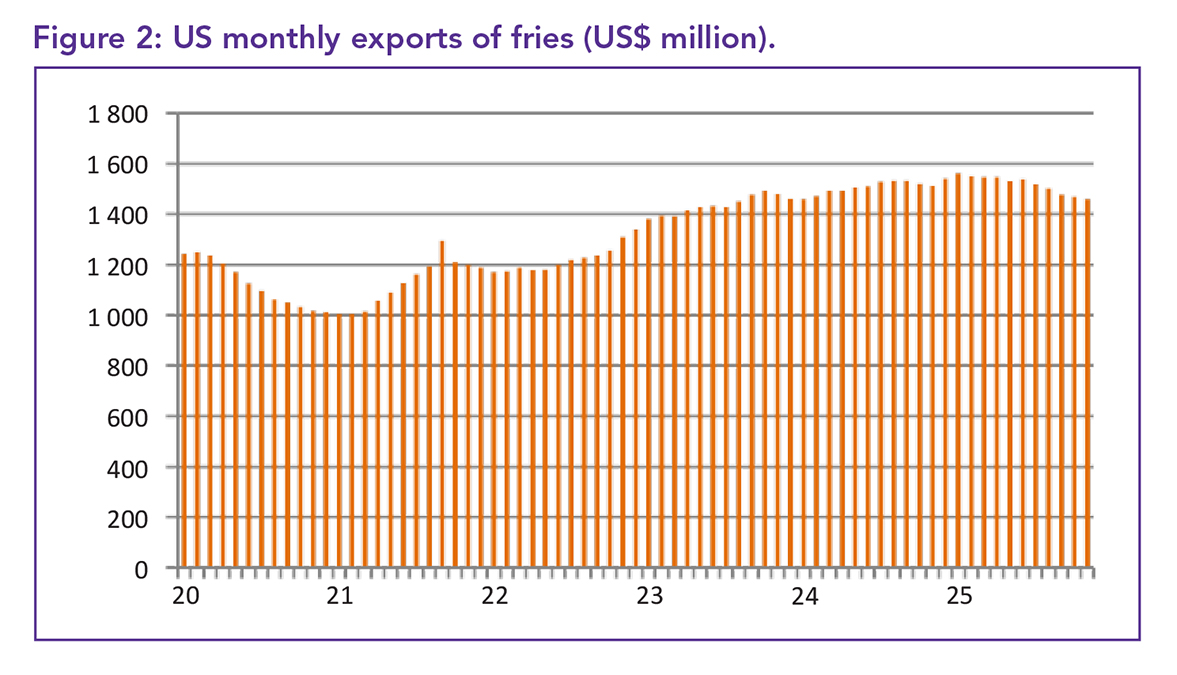

While November’s total US exports of processed potatoes were 3.8% lower than the year before, its earnings fell 7.6% to US$108.378 million (€91.43 million).

Mixed trends in potato trade

Fry import volumes bounced back in November, climbing 5 730 tonnes up to 123 139, just 3% less than the year before. All the main European importers recorded increased sales compared with Canada, despite contending with 15% trade tariffs.

November saw President Trump, fearful of the impact of his tariffs on domestic food inflation, removing tariffs on certain food categories; however, processed potato products were not included.

Tariff-free imports of Canadian fries rose by 2 551 tonnes. Belgian imports, subject to a 15% tariff, increased by 2 790 to 15 274 tonnes; Dutch imports, also with a 15% tariff, rose by 359 to 2 381 tonnes; and German fries, with the same tariff rate, climbed 481 to 1 435 tonnes.

Imports from India have been making good headway in the US market, however, with typical Trumpian unpredictability, most Indian products were hit with a 50% tariff. November saw Indian imports fall from 769 tonnes in September to just 210 tonnes. Canada’s fry price was US$17 lower at US$1 370/t (€1 156), while both Belgian and Dutch fries reduced their import prices by larger amounts; these prices are quoted before any import tariffs. The month’s Belgian price was US$38 lower at US$1 498/t (€1 264), while the Netherlands’ price was US$81 lower at US$1 289/t (€1 087). The German fry price was US$35 higher at US$995/t (€839), but 20.4% lower than the year before.

Comparing the month’s import earnings to the year before, Canada’s US dollar earnings were 6.7% lower, Belgium’s were 21.3% down, and the Netherlands 23.2% lower. Higher-end French processed products, which saw a price reduction of US$40 to US$3 618/t (€3 052), saw earnings increase by 26.2% compared with November 2024. Six months into the tariff programme, it appears that EU importers are beginning to feel the financial pinch, although demand for products remains unaffected.

Much of the current slide in EU prices is being seen around the world due to the Union’s current strong supply situation.

Egypt faces just a 10% tariff. Its November sales were down 407 at 1 489 tonnes, which is 6.8% lower than the year before, with the average price down by US$16 to US$1 153/t (€973). Indian fries became more expensive in the US market, with November prices rising US$185 to US$1 696/t (€1 431), prior to being penalised through tariffs. Although total import volumes were only 3% lower than a year earlier, the cost of those imports before tariffs fell 10.9% to US$171.648 million (€144.8 million).

While fresh and processing potato imports from Canada rose in November by 11 159 to 43 665 tonnes, this was 8.3% below November 2024. The price US$787/t (€664) was 1.4% higher.

It was a good month for potato exports to Japan, rising by 4 000 to 6 766 tonnes, which was a 95% improvement on the year before, despite the price being 87.6% higher at US$947/t (€799). Mexican fresh potato exports fell by 3 488 to 18 765 tonnes, down 21.2% on November 2024, with the price 16.2% lower at US$468/t (€395). South Korean exports were 5.9% lower at 5 021 tonnes, with the price down 3% to US$546/t (€461).

Canada

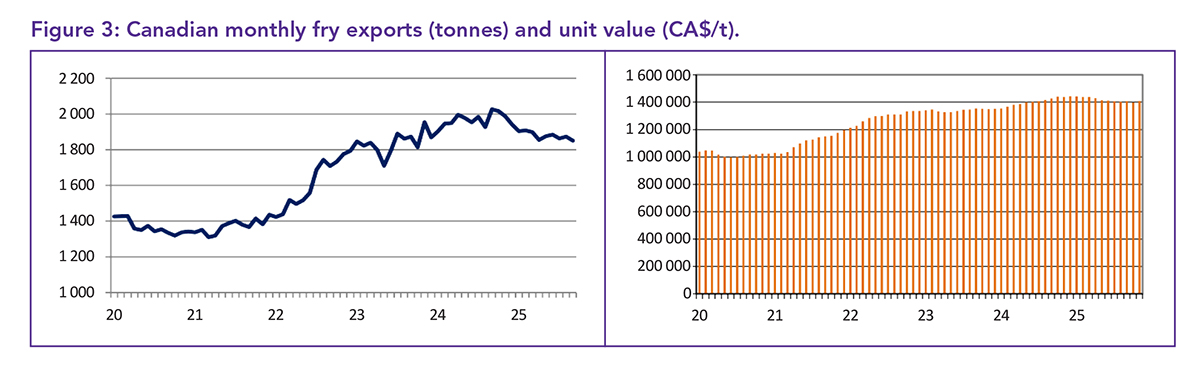

A CA$22 drop in the average export price helped secure international sales of 124 093 tonnes in November 2025, the highest volume since March and 11.3% higher than a year ago. Over the past eight months, the average Canadian export price has fallen 8.8% and, at CA$1 850/t (US$1 356; €1 143), is slightly lower than it was two years earlier. Fry sales to the US were 2 515 tonnes higher at 101 185, encouraged by a CA$15 price drop, selling at CA$1 953/t (US$1 431; €1 207), 7.1% lower than a year ago. In contrast, the US export price to Canada was 5.9% higher.

A large increase in sales to Japan also contributed to the month’s figures. Japanese sales were 1 701 tonnes higher at 5 069, more than double the level seen a year earlier. Over the previous 12 months, sales to Japan increased by 50.8% to 43 860 tonnes. The improvement was achieved without a price cut; the November price was CA$54 higher at CA$1 444/t (US$1 058; €893), though still 9.6% lower than 12 months before.

Although annual sales to Mexico were 37.2% higher at 66 572 tonnes, November sales slipped 743 to 7 191 tonnes, despite a CA$34 price cut, selling at CA$1 531/t (US$1 122; €946).

Taiwan increased purchases by 708 to 1 307 tonnes, while South Korea added 159 tonnes, taking in 417. The Taiwanese price was CA$45 higher at CA$1 231/t (US$902; €761), while South Korea paid CA$150 more, at CA$1 371/t (US$1 005; €847).

In Central America there were increases of 700 to 800 tonnes in business with Panama and Costa Rica. With no change in price, Panama took 2 202 tonnes at CA$1 249/t (US$915; €772), while a CA$83 price cut saw Costa Rica increase its purchases to 1 811 tonnes, taking its purchases for the year up to 12 573 tonnes. Canada’s sales to the Gulf States also continued to improve.

Saudi Arabia imported 445 tonnes more, paying CA$1 227/t (US$899; €758) for 1 091 tonnes, while the UAE bought 146 tonnes more, paying the same price for 721 tonnes. Both countries have seen little change in their price for the past three months, with Kuwait purchasing at the same rate in November.

Lower prices meant that, although November’s sales were 11.3% higher than a year ago, takings were only 1.4% better at CA$229.539 million (US$168.2 million; €141.9 million).

US fries dominate Canadian market

While EU processors may be finding the US market challenging, there appears to be no enthusiasm for the product further north in Canada either. In November, Canada purchased 4 576 tonnes of imported fries, with sales declining for all major suppliers.

Compared to a year ago, Canadian imports were still 12.4% higher, but the annual gain was entirely in favour of US imports, which were 17.5% higher at 4 138 tonnes. Compared with a year earlier, Belgian imports were 5.9% lower at 335 tonnes, Dutch imports declined by 36.1% to 23 tonnes, and French imports were 84.6% lower at just ten tonnes.

Dutch fries offered the largest discount in the month. At CA$2 876/t (US$2 107; €1 778), they were CA$1 739/t cheaper than in October. France’s fries were CA$1 347/t cheaper at CA$3 326/t (US$2 437; €2 056), while Belgian fries were CA$214/t less at CA$2 189/t (US$1 604; €1 353).

Although enjoying an annual increase, sales of US fries were still 322 tonnes lower than in October, as its sales price came down by CA$86 to CA$2 256/t (US$1 653; €1 394). India reduced its price by CA$740, selling at CA$2 379/t (US$1 743; €1 470) and its sales improved by 21 to 50 tonnes.

China exported three tonnes of processed product at CA$3 390/t (US$2 484; €2 095).

With no shortage in stock from the 2025 harvest, Indonesia was a welcome market for exports of 3 528 tonnes of ware potatoes, 85.3% higher than a year ago, from Canada.

Sales to Indonesia for the year have increased by 487% to 11 172 tonnes, while annual sales to Trinidad and Tobago fell by 24.4% to 11 600 tonnes.

Trinidad and Tobago paid CA$648/t (US$475; €401) for their imports and Indonesia paid CA$912/t (US$668; €564). The month’s fresh potato exports to the US were 8.3% lower than the year before at 43 636 tonnes, at a price of CA$1 153/t (US$845; €713).

Germany

Germany harvested its largest crop of the century in 2025, totalling 13.871 million tonnes, according to the latest government estimates. This was 9.2% higher than in 2024, with the consumption potato harvest at almost ten million tonnes. The increase in production was driven by a 6.9% expansion in area to 301 800 ha and a 2.1% increase in average yields to 46 t/ha. It was the first time since 2000 that the area exceeded 300 000 ha.

The lowest area of recent years was recorded in 2015, at 237 000 ha.

Niedersachsen retained its position as the largest potato-growing region, producing 47.6% of the national crop. Nordrhein-Westfalen accounted for 17.9% of the total, while Bayern contributed 13.6%. The highest yielding region was Nordrhein-Westfalen at 52.1 t/ha, although this was slightly lower than in 2024. The largest production increase was in Bayern, up 24.5%, reflecting both the second-largest increase in planted area and the strongest improvement in yields. No region reduced its potato area in 2025 compared with 2024.

However, Brandenburg harvested a smaller crop due to a 9.3% decline in average yields.

The national and European surplus of potatoes means that growers are likely to reduce planted area in 2026, but the decline would need to be much greater than 5% to bring the market back into balance.

Lower prices are prompting sale increases, especially in multiple retailers such as supermarkets and hypermarkets. Retail sales in December reached 146 000 tonnes, up 10% on the same month in 2024, according to YouGov data for AMI. Compared to November 2025, December demand in supermarkets rose by 17%, with a 27% increase in hypermarkets and 25% increase in discount store sales, which was 13% up on the same month in 2024.

Over the year, retail demand rose 2.7% to 1.496 million tonnes and six-month sales to the end of December were 3.4% higher at 756 000 tonnes. However, demand in weekly markets and greengrocers declined. The average retail price of potatoes fell by 16.3% between December 2024 and December 2025.

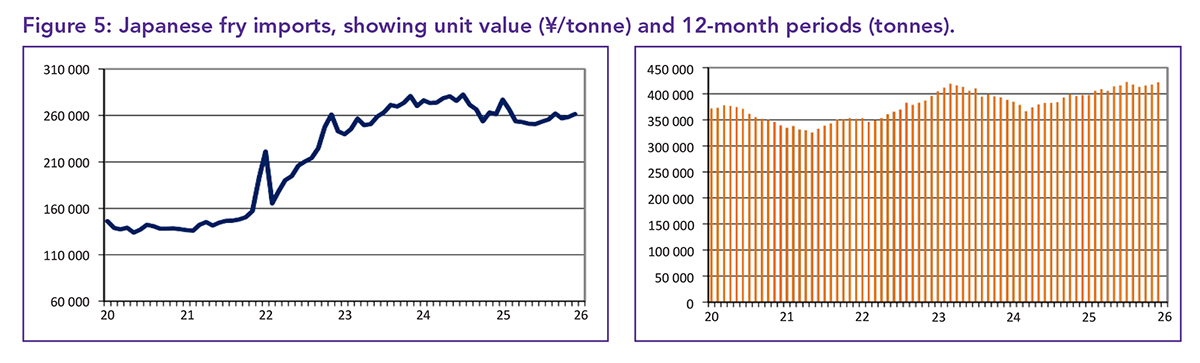

Japan

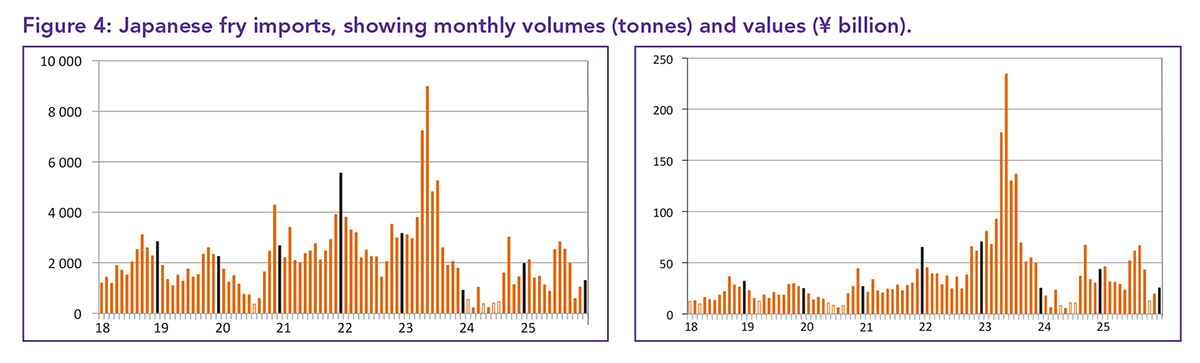

Strong sales in December – up 15% on the year before to 35 099 tonnes – pushed Japan’s annual imports of processed potatoes up to a new all-time high of 422 526 tonnes.

Annual import volumes have now surpassed the 419 689-tonne mark seen in March 2023. However, this rise in consumption is not driven by population growth. Japan has one of the fastest-shrinking populations in the world, falling from 126.3 million in 2020 to an estimated 122.4 million this year.

The rise in consumption appears to be driven by the arrival of lower-priced fries on the market, thanks to the expansion of Chinese potato processing. Chinese imports have grown from 3 497 tonnes in 2021 to 50 455 tonnes in 2025. Although they still account for a 12% market share, they have consistently provided a lower cost alternative to American or European imports. In 2025, the overall average import price was ¥237 914/t (US$1 536; €1 295). China’s average price was ¥196 770/t (US$1 271; €1 071), just 72% of the average US import price and 78% of the average Belgian import price.

While all the major importers have reduced their prices over the past year, none have done so with the rigor of China. The US average import price across 2025 was 2.1% lower than in 2024 at ¥273 250/t (US$1 765; €1 488), while Belgium’s fell 3.4% to ¥252 027/t (US$1 628; €1 372). China, by contrast, cut its average price by 14.4%.

December’s demand rose as Japanese consumers enjoyed dining out on chicken and chips over the Christmas break. Month-on-month imports increased by 3 206 tonnes with the largest increases seen from the US and Canada. US sales rose 3 275 to 19 981 tonnes despite a ¥7 000 price increase, selling at ¥282 500/t (US$1 824; €1 538). Canada dropped its price by ¥15 000 to ¥264 493/t (US$1 708; €1 440), and its sales more than doubled to 3 644 tonnes; their highest monthly volume in recent years.

China’s price rose by ¥20 500 to ¥210 780/t (US$1 361; €1 147), while its sales only increased by 660 to 5 810 tonnes. Yet it was still December’s second largest importer. The month’s losers were Belgium and the Netherlands. Belgian sales fell 1 502 to 1 887 tonnes, despite an ¥8 300 price cut, selling at ¥261 458/t (US$1 688; €1 423). Dutch sales were halved to 1 369 tonnes, following a ¥5 700 price reduction to ¥250 934/t (US$1 620; €1 366).

Luckily for Japanese consumers, Indian exporters are following China’s tactics. India imports were selling at ¥189 689/t (US$1 225; €1 033), ¥22 800 less than in November. Sales increased by nearly 300 to 2 021 tonnes, overtaking Belgium and the Netherlands. Indian fry imports for the year are up 74.9% to 13 681 tonnes.

Argentina sold 108 tonnes of fries at a much higher price of ¥361 991/t (US$2 338; €1 971). Annual imports were 6.1% higher at 422 526 tonnes, although the cost of those imports had hardly changed at ¥108.975 billion (US$704 million; €593 million).

However, a fondness for American fries meant that December’s volumes and expenditure were both up 15%. US potato imports also remained popular, rising 4 830 to 6 545 tonnes, approximately 169.5% higher than the year before, despite this year’s price being 12.1% higher at ¥122 551/t (US$791; €667). Over the year, fresh US potato imports were 35.5% higher at 48 319 tonnes.

New Zealand and Australia

Frozen fry exports were at their highest for three calendar years in 2025, as exporters boosted sales thanks to competitive pricing.

During the year, 55 020 tonnes of product was shipped – 17.5% more than in 2024, although still some way short of the record of almost 78 000 tonnes in 2018. Sales in December were 13.5% higher than the same month the year before, reaching 4 080 tonnes. The average price of fry exports over the year was NZ$1 855/t (US$1 123; €951), 1.3% lower than in 2024, despite a spike in December values. This pricing keeps New Zealand competitive, even against newcomers such as India and China, and well below European or North American prices.

New Zealand had a particularly good year in Australia, with exports to its neighbour up 34.4% to 20 774 tonnes, though still 7 000 tonnes less than in 2023. December demand from Australia for New Zealand fries was 115.1% higher, at 2 237 tonnes.

New Zealand struggled in its second largest market, the Philippines, in December, but over the year exports to the country were up 27.1% to 8 788 tonnes. Demand from Thailand and Malaysia fell over the year, though there were steady, albeit small, sales to Indonesia, Taiwan, and South Korea.

Imports of frozen fries into New Zealand fell by 11.7% in 2025 to 22 854 tonnes but were up 9.1% to 2 197 tonnes. The average import price in December was NZ$2 662/t (US$1 611; €1 364). Over the year, Australia accounted for 57% of total imports, the Netherlands 23% and Belgium 13%.

New Zealand’s fresh potato exports rose by 11.1% in 2025 to 28 418 tonnes. Fiji accounted for 82% of that trade, followed by French Polynesia at 6% and Samoa at 5%. The average export price for the year was NZ$936/t (US$567; €480), 7.5% lower than in 2024.

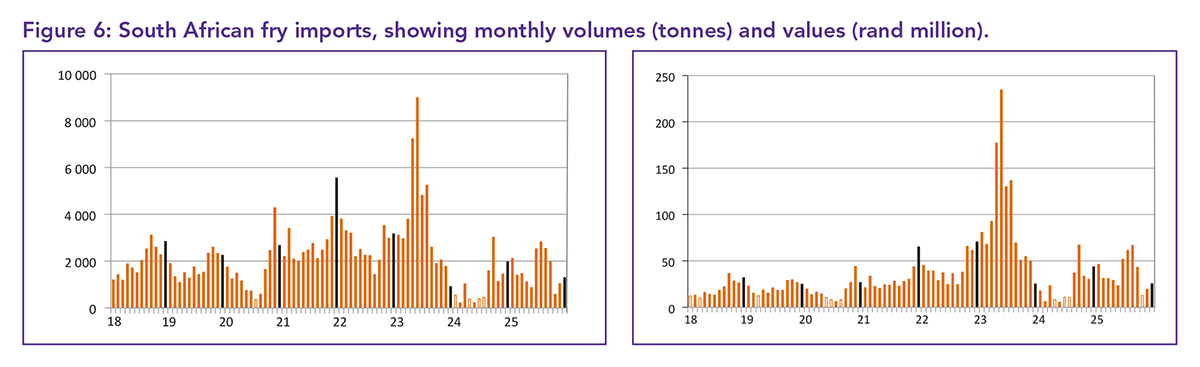

South Africa

Following a year of growth, 2025 ended with a plunge in frozen fry imports.

In December, 1 298 tonnes of product were imported, 34.1% less than the same month the year before and only 184 tonnes more than exports. Over the year, exports were up 59.4% to 19 795 tonnes.

The average price for the year was R22 334/t (US$1 399; €1 185). Belgium saw its imports rise by 16.5% to 11 280 tonnes, although December imports fell 40.7%. Imports from the Netherlands, the US, and China also grew over the year.

China was the lowest-priced supplier throughout 2025, at R14 017/t (US$878; €744), which was 37.2% less than the average import price and 51.9% lower than the highest-priced US imports. While exports fell in December, annual trade grew 12.4% to 10 129 tonnes.

All markets grew or held steady over the year, with the average export price rising 8.1% to R29 372/t (US$1 840; €1 558). Namibia accounted for a third of the market, with Botswana contributing 30%.

Exports of fresh potatoes increased 22.5% in 2025, reaching 166 148 tonnes. Mozambique was the largest market, accounting for 64% of sales, followed by Namibia at 17%, and Eswatini and Lesotho at 7%. Exports in December hit their highest monthly total since December 2021 at 21 405 tonnes, some 45.6% more than the same month in 2024. The average price of ware exports in 2025 was R4 592/t (US$288; €244), 2% less than in 2024. – Francois Strauss, Potatoes SA

For more information, email the author at francois@potatoes.co.za or visit www.potatoes.co.za.