Estimated reading time: 6 minutes

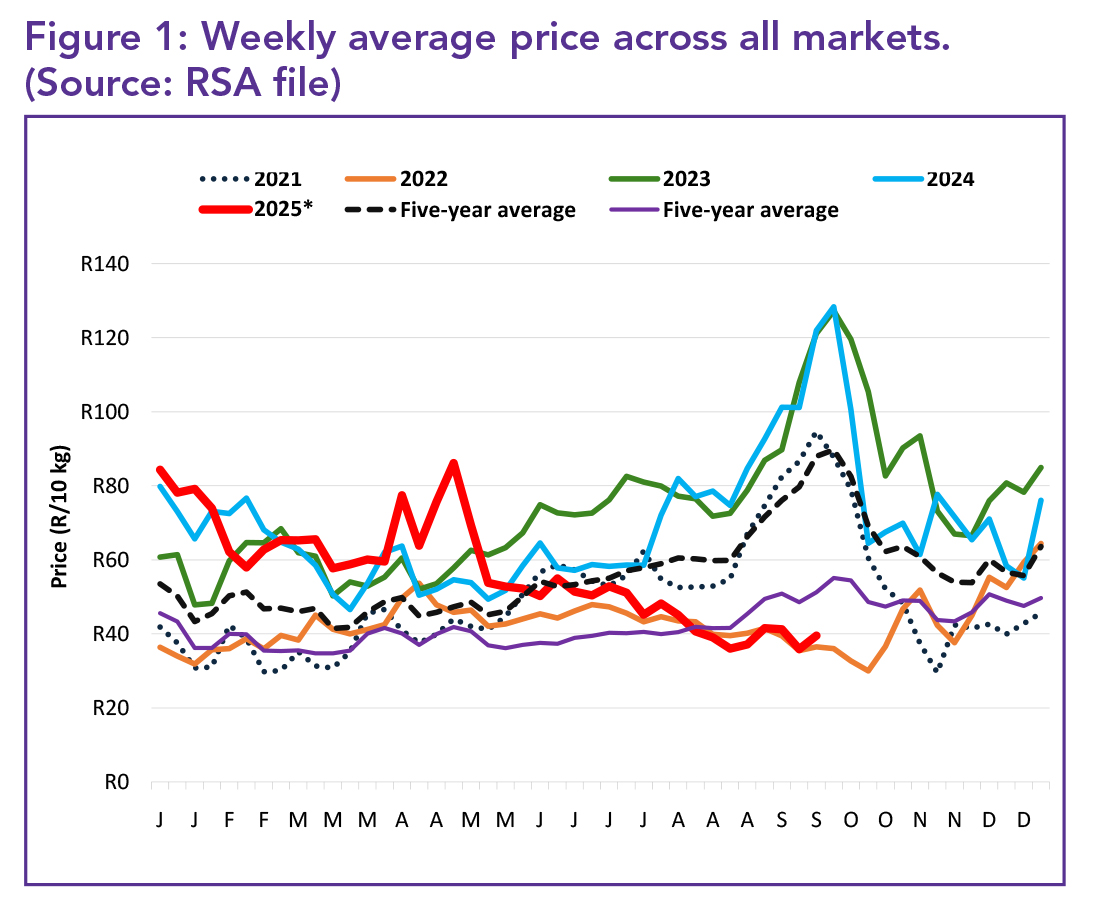

The average weekly price of potatoes during the first 39 weeks of 2025 at South Africa’s fresh produce markets (FPMs) showed a week-on-week increase of 10%. As illustrated in Figure 1, which tracks the weekly average price across all markets and potato classes and sizes, the average price in week 39 stood at R39.53 per 10 kg bag. This represents not only a week-on-week increase but also a year-on-year decrease of R82.46 compared to the corresponding week in 2024, underscoring heightened price volatility and market fluctuations.

Stock levels and price trends

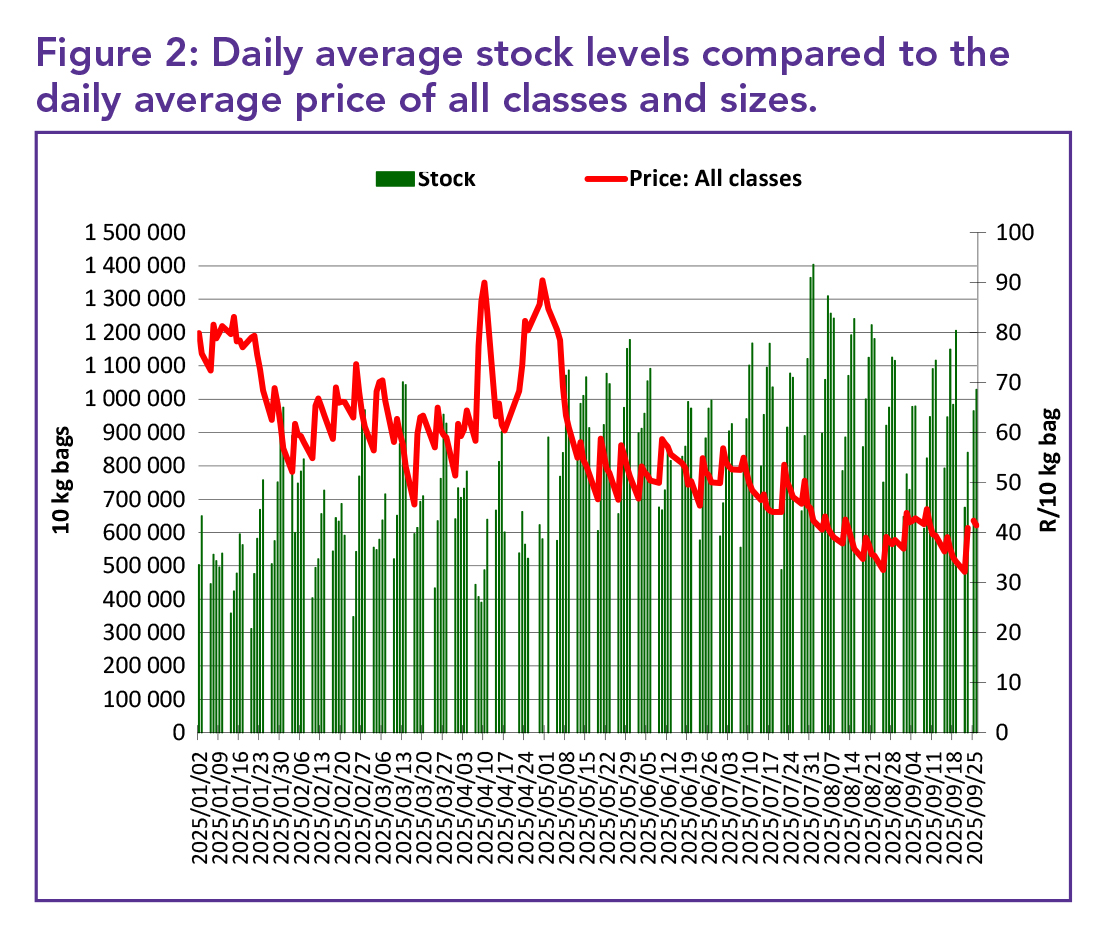

Figure 2 illustrates the relationship between supply and demand by analysing daily average stock levels alongside price trends. Elevated stock levels typically place downward pressure on prices. The average daily stock across South African FPMs was 807 596 bags (10 kg) during the first 39 weeks of 2025. In September, this figure rose to 909 842 bags – 48% higher than the September 2024 average of 614 854 bags.

Sales volumes and trends

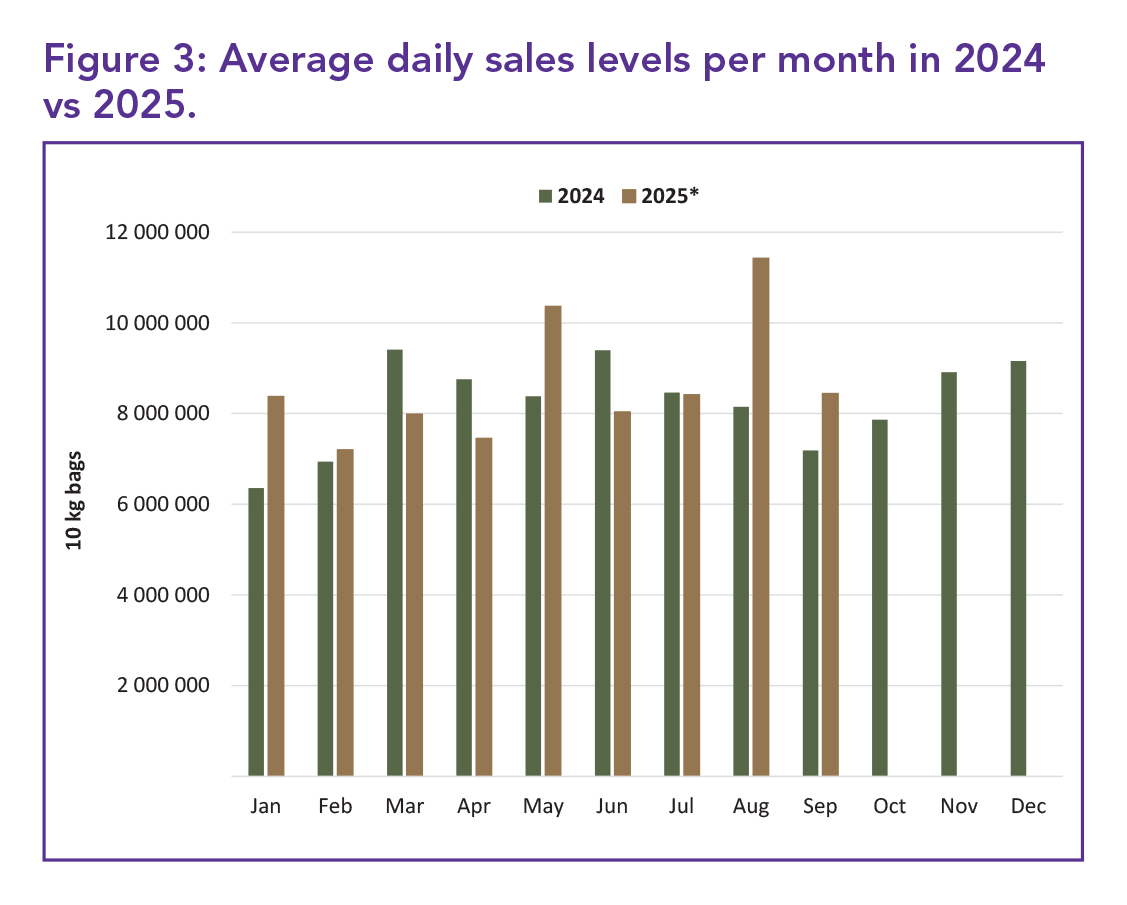

Figure 3 presents a year-on-year comparison of monthly sales volumes, showing an 18% increase in September 2025 relative to September 2024.

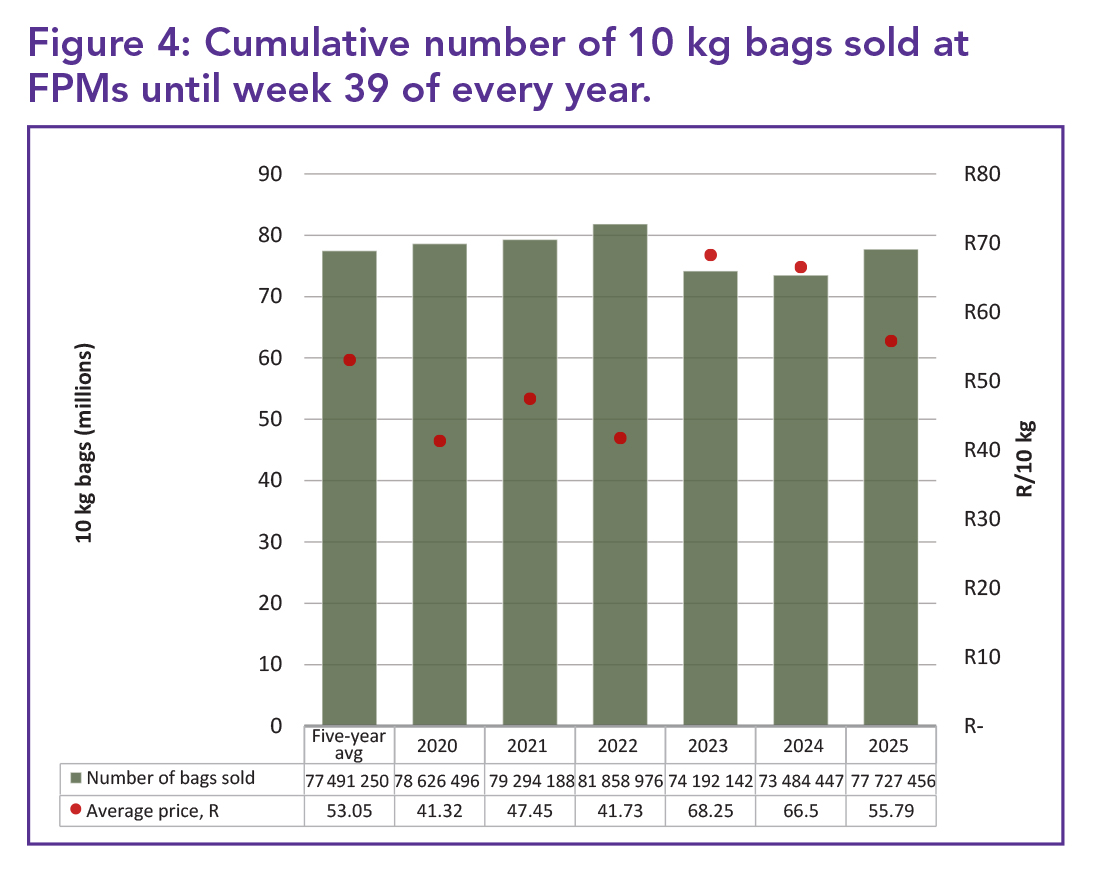

Despite this growth, cumulative sales for the first 39 weeks of 2025 totalled 77.7 million 10 kg bags, which is 236 206 bags above the five-year average for the same period, as shown in Figure 4. Notably, the average price in 2025 is R2.74 higher than the five-year average.

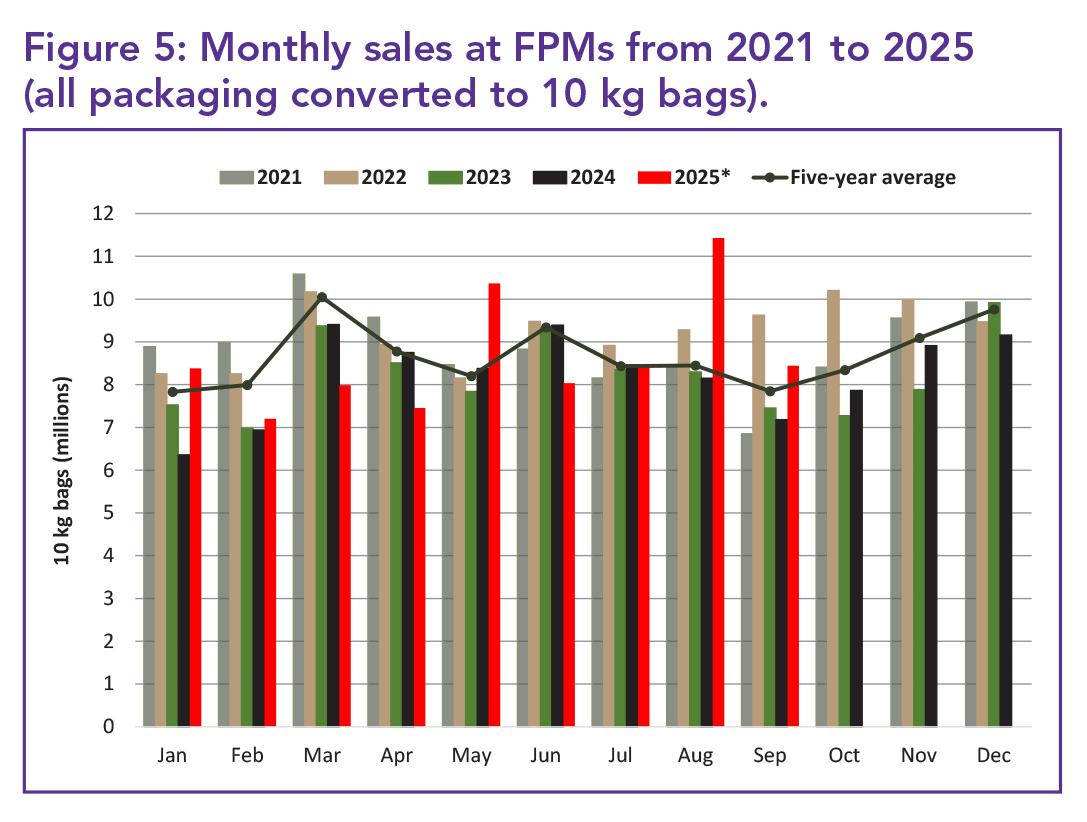

Monthly sales trends at FPMs, depicted in Figure 5, indicate a moderate month-on-month decline, with September 2025 recording 8.4 million 10 kg bags sold, compared to 11.4 million bags in August 2025. This represents a volume decline of 2 985 695 bags (10 kg).

Bag sales and averages

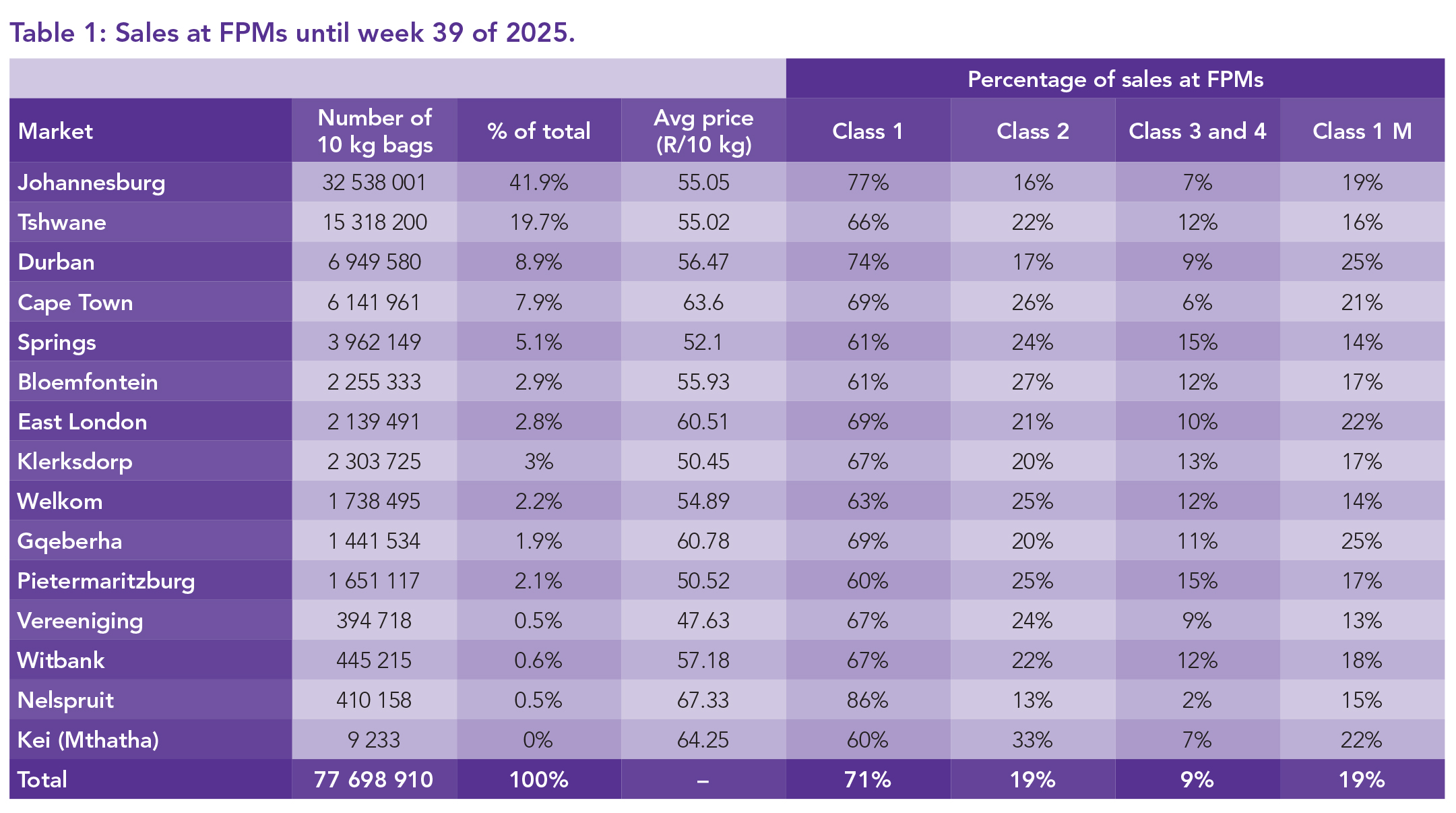

Table 1 outlines the number of bags sold at the various FPMs during the first 39 weeks of 2025. The five biggest markets during this period were collectively responsible for 83.5% of the country’s sales, showcasing their pivotal role in the potato supply chain. The average price per 10 kg bag across all classes and sizes is also reflected in Table 1.

In terms of the top average price per 10 kg bag received at the markets during the first 39 weeks, Nelspruit Market led with R67.33 per 10 kg bag, followed by Kei Market with R64.25 per 10 kg bag and Cape Town Market with R63.60 per 10 kg bag. In terms of Class 1 (all sizes) sales, Nelspruit, Johannesburg, Durban, and Cape Town Markets’ total sales consisted of 86, 77, 74 and 69% bags, respectively, with Johannesburg being the highest of the top five markets.

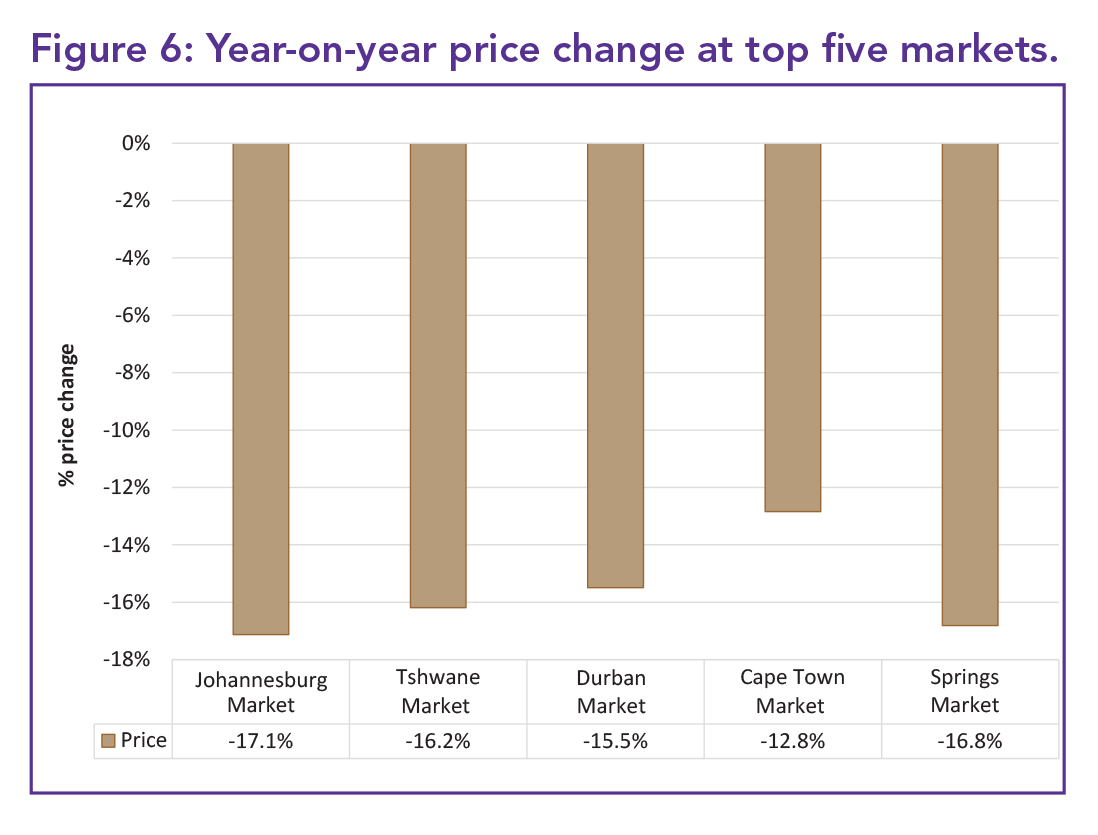

Figure 6 shows the year-on-year price change at the top five markets for the first 39 weeks of 2025, with all markets experiencing price declines. Johannesburg Market’s price showed the greatest percentage decline, decreasing by 17.1%.

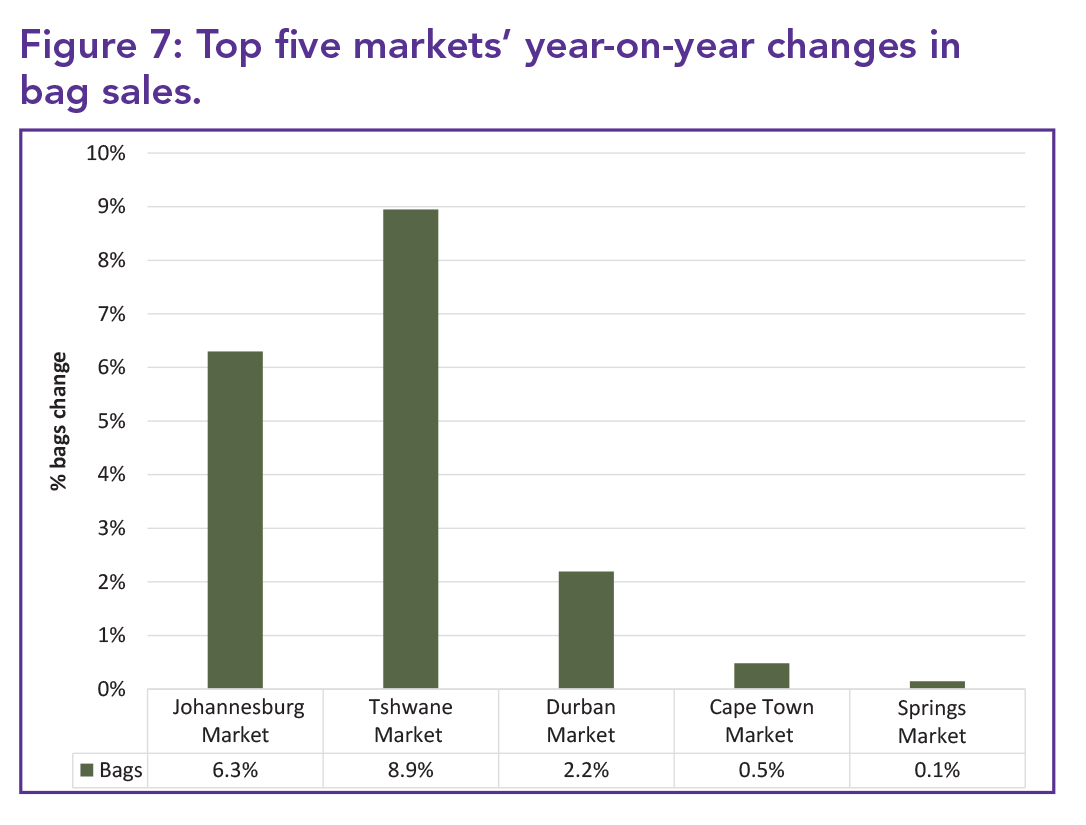

However, Figure 7 highlights a corresponding 6.3% year-on-year increase in sales volume at this market. The volumes sold at Tshwane Market increased by a notable 8.9% year-on-year.

Regional performance

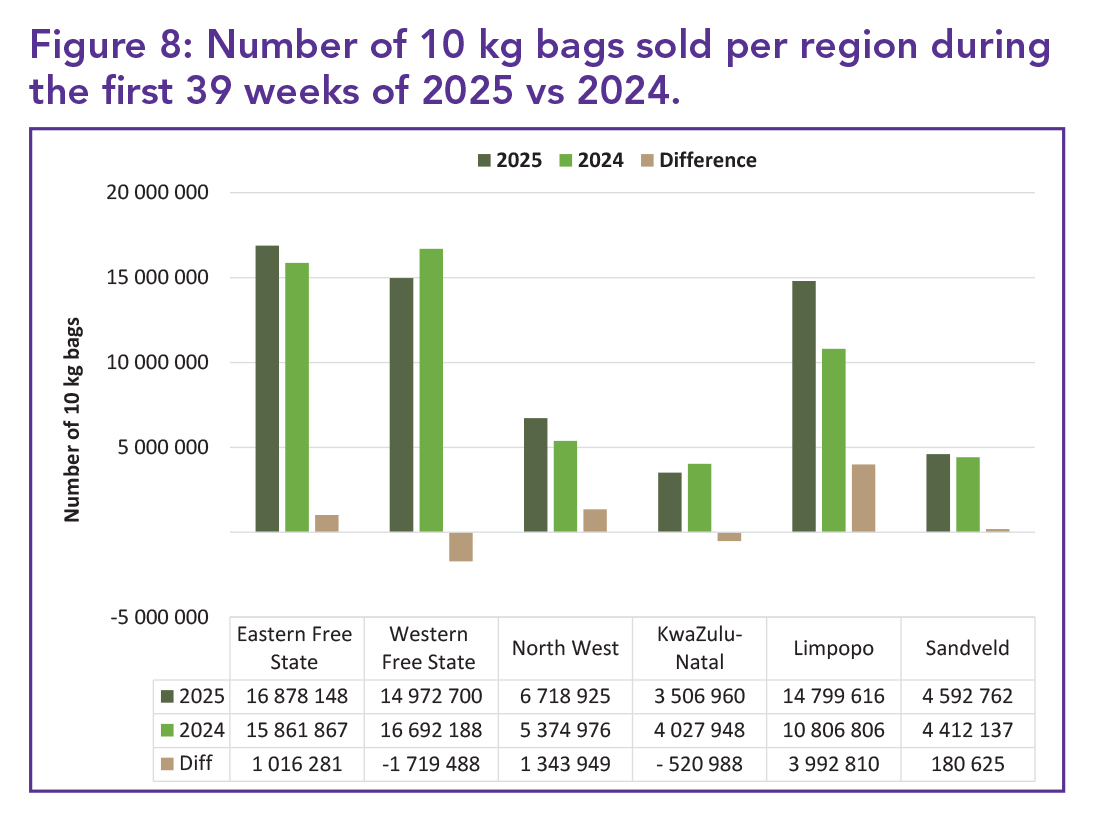

Figure 8 indicates sales performance at regional level. KwaZulu-Natal and the Western Free State regions showed a decline in the first 39 weeks of the year. The Eastern Free State, North West, Limpopo and the Sandveld recorded volume growth.

The Eastern Free State, KwaZulu-Natal, Western Free State, North West, Limpopo and the Sandveld collectively accounted for 79% of total national potato sales in the first 39 weeks of 2025, as summarised in Table 2.

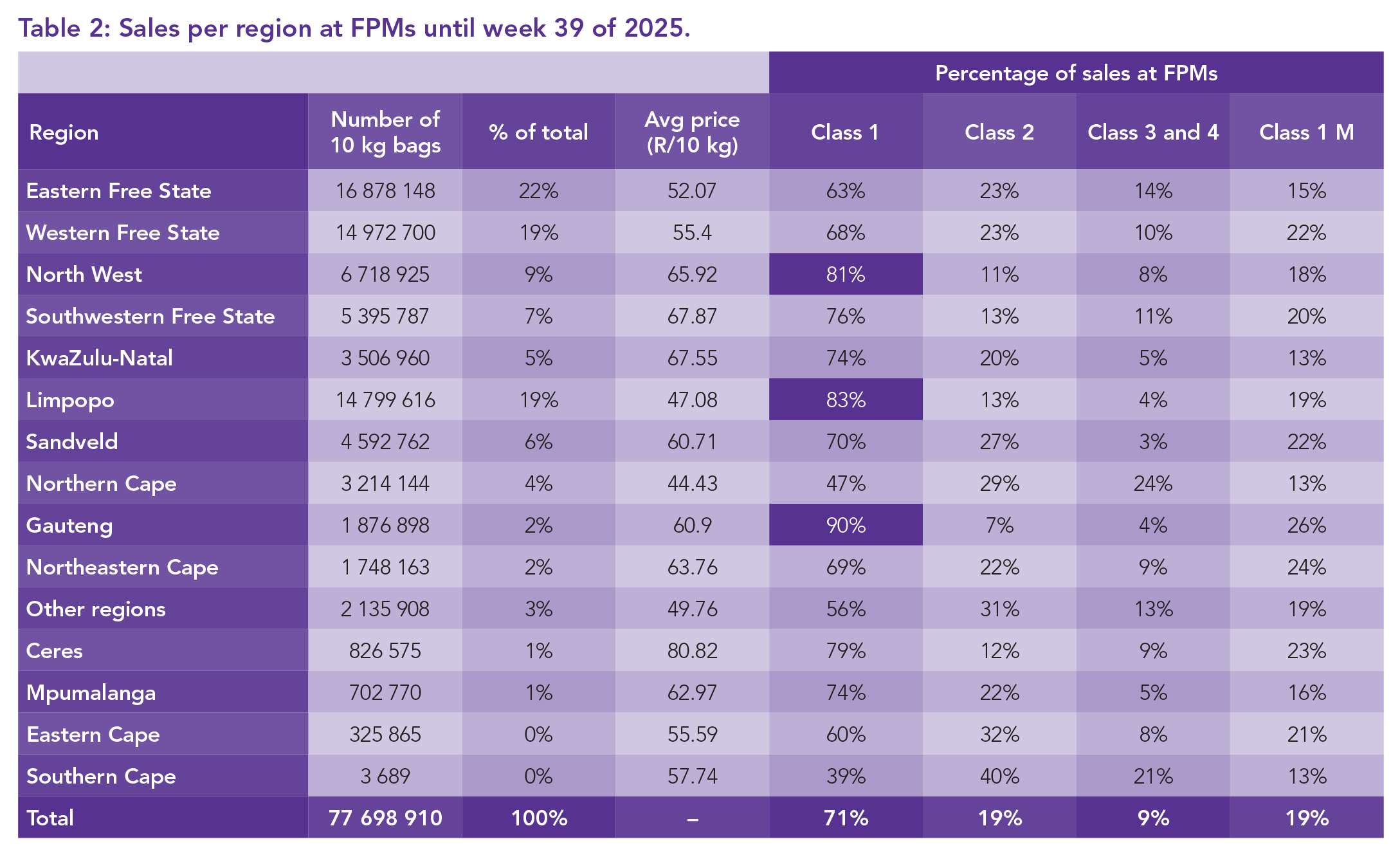

The classification of potatoes also varies significantly by region, as shown in Table 2. Regions such as Limpopo, North West and Gauteng led in Class 1 sales, with 83, 81 and 90% of their sales falling into this premium category, respectively. Overall, 12 of the 16 regions maintained a Class 1 sales ratio above 60%, reflecting consistent quality standards across much of the country. – Dikgetho Mokoena and Jodie Hattingh, Potatoes SA

For more information, email Dikgetho Mokoena at dikgetho@potatoes.co.za or Jodie Hattingh at jodie@potatoes.co.za.