Estimated reading time: 12 minutes

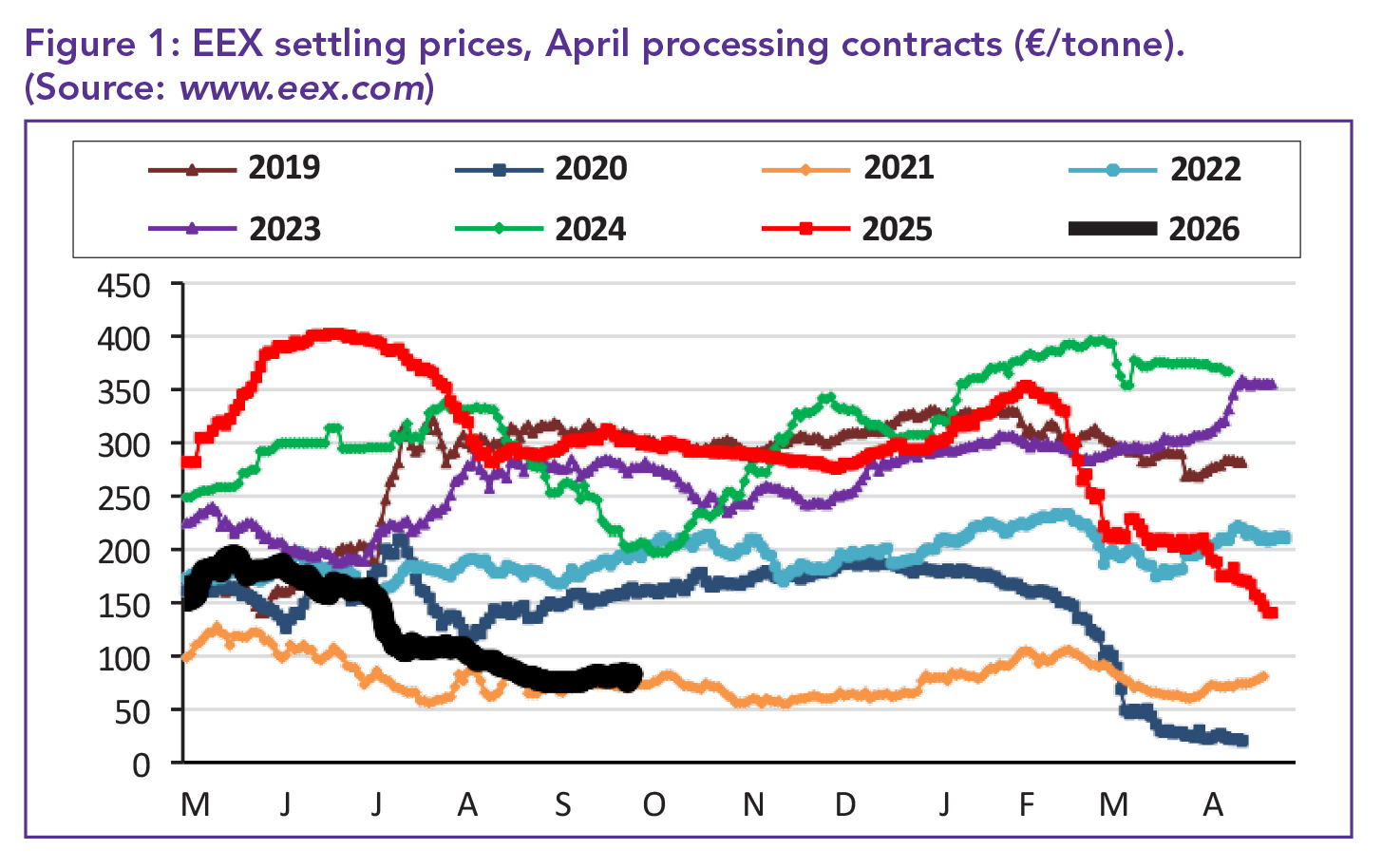

The European potato market has experienced a notable shift. Early in the season, high prices were anticipated for the third consecutive year. However, weakened demand and abundant stock caused prices to fall. Contract buying played a dominant role in the market, driving prices down to as low as €10/tonne. Free-buy prices started higher, with Dutch PotatoNL averaging €80/tonne before declining to €75.

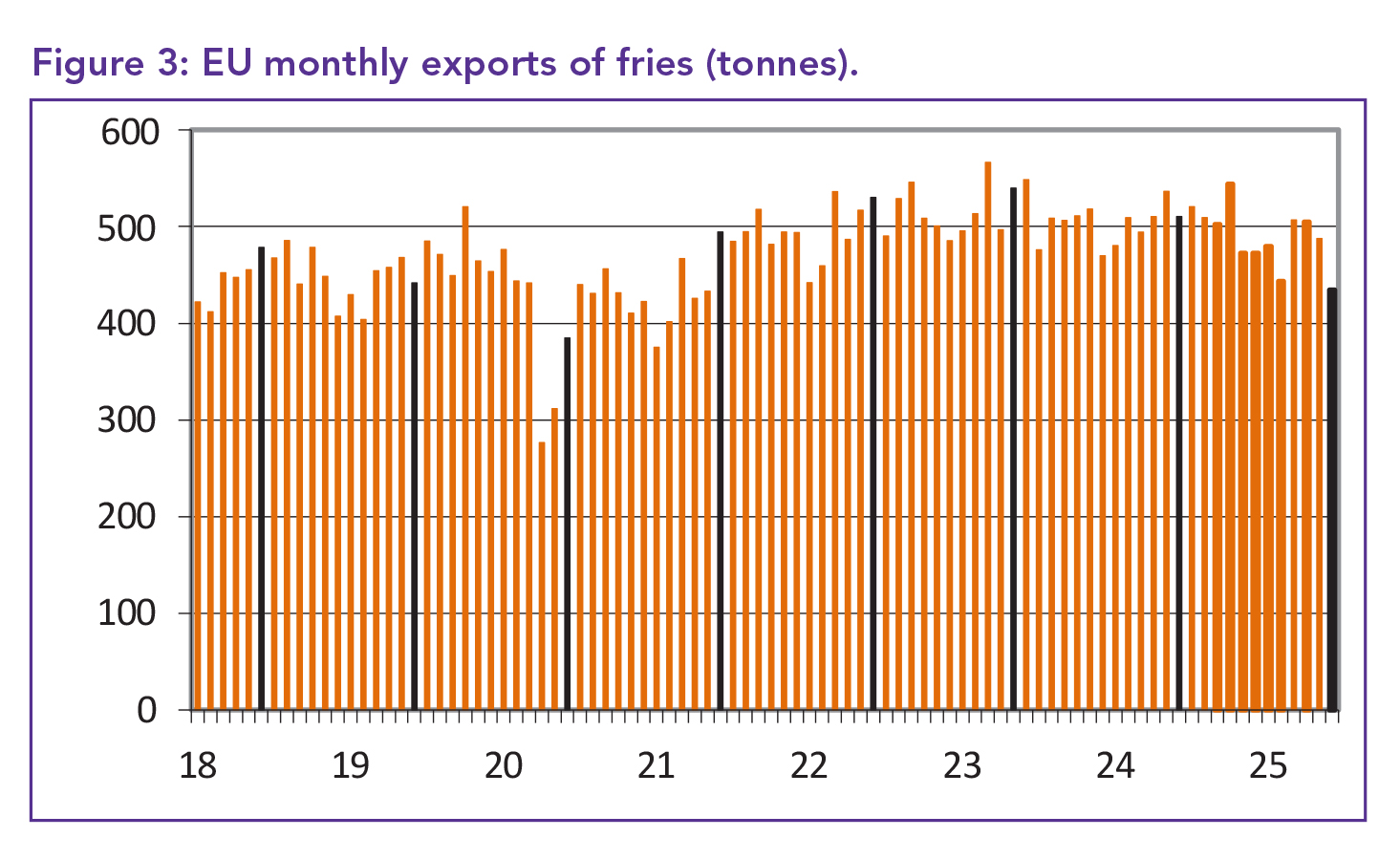

In July, European Union (EU) frozen fry exports saw a slight increase compared to June, but remained 1% lower than in July 2024, and 6.3% lower for the year. Demand within the EU declined, with Belgium and the Netherlands being particularly affected, whereas France experienced growth. Globally, reduced demand for European fries affected sales, though 12-month totals remain above last year’s levels and are 10% higher than in 2019. Meanwhile, China continues to expand its fry exports, setting another 12-month record in August.

Mixed start for EU fry exports

The EU frozen fry export market began the new season in July on a cautiously optimistic note, with global sales (excluding the United Kingdom [UK]) rising by 3 500 tonnes compared to June, reaching 153 288 tonnes – an increase of 7.8% year-on-year (YOY).

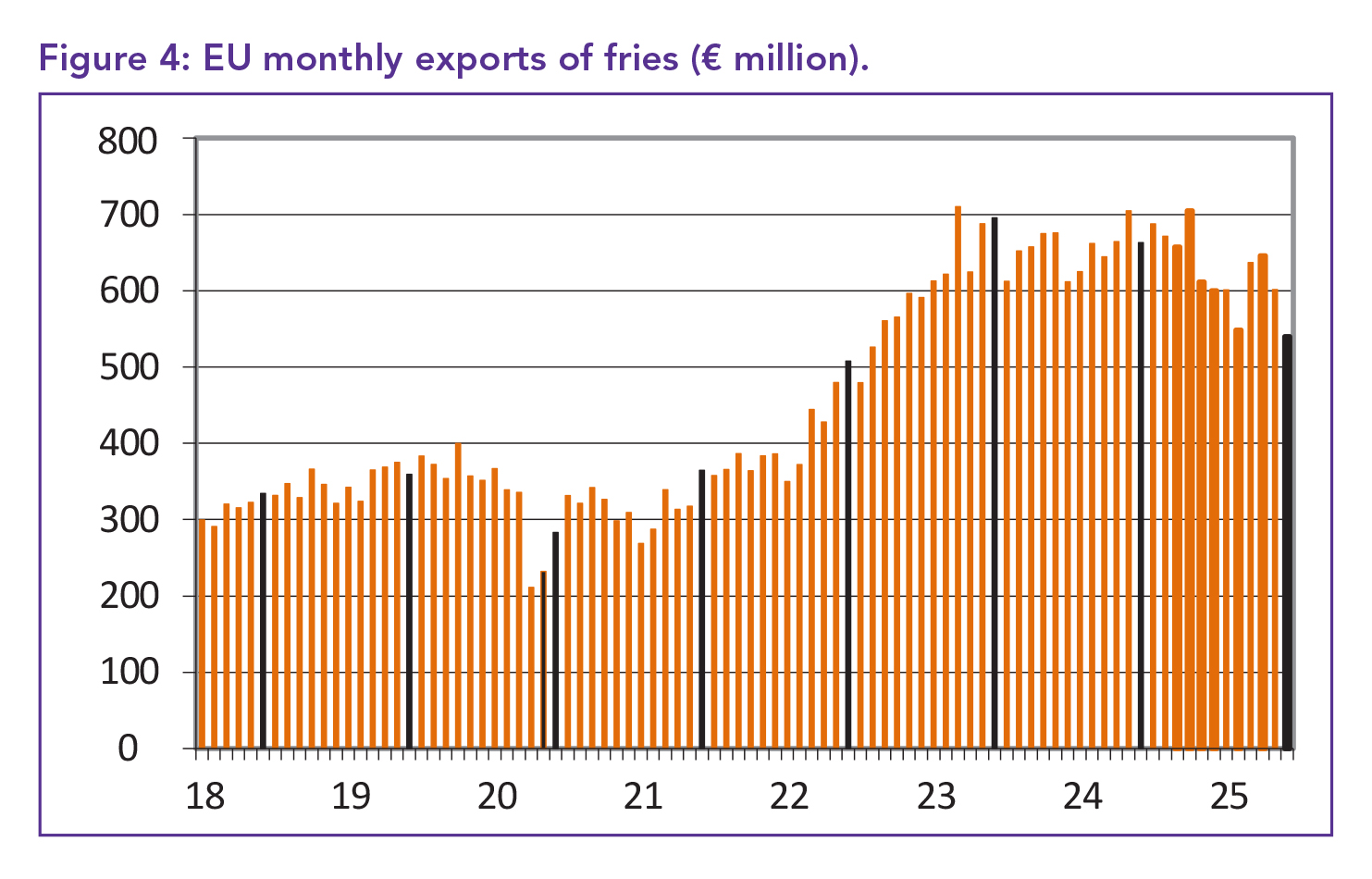

However, global competition and currency pressures pushed average export prices down by 9.3% from last year, to €1 240/tonne. As a result, total EU export earnings dropped by 10.2% YOY to €268.3 million, with an 18% decline in UK sales contributing significantly to the downturn.

The United States (US) market defied expectations, with July sales jumping 35.5% YOY to 20 378 tonnes, despite the ongoing 15% tariff. Surprisingly, prices also rose by €32 to €1 337/tonne, suggesting either strong demand from US consumers or increased cost pressures within the American food service sector.

Asia showed mixed results. While overall regional sales declined by 13.4%, exports to Japan – Europe’s largest Asian buyer – reached 7 586 tonnes, the highest level since September 2024. Prices in Japan remained stable, and the average regional price dipped by just 1%.

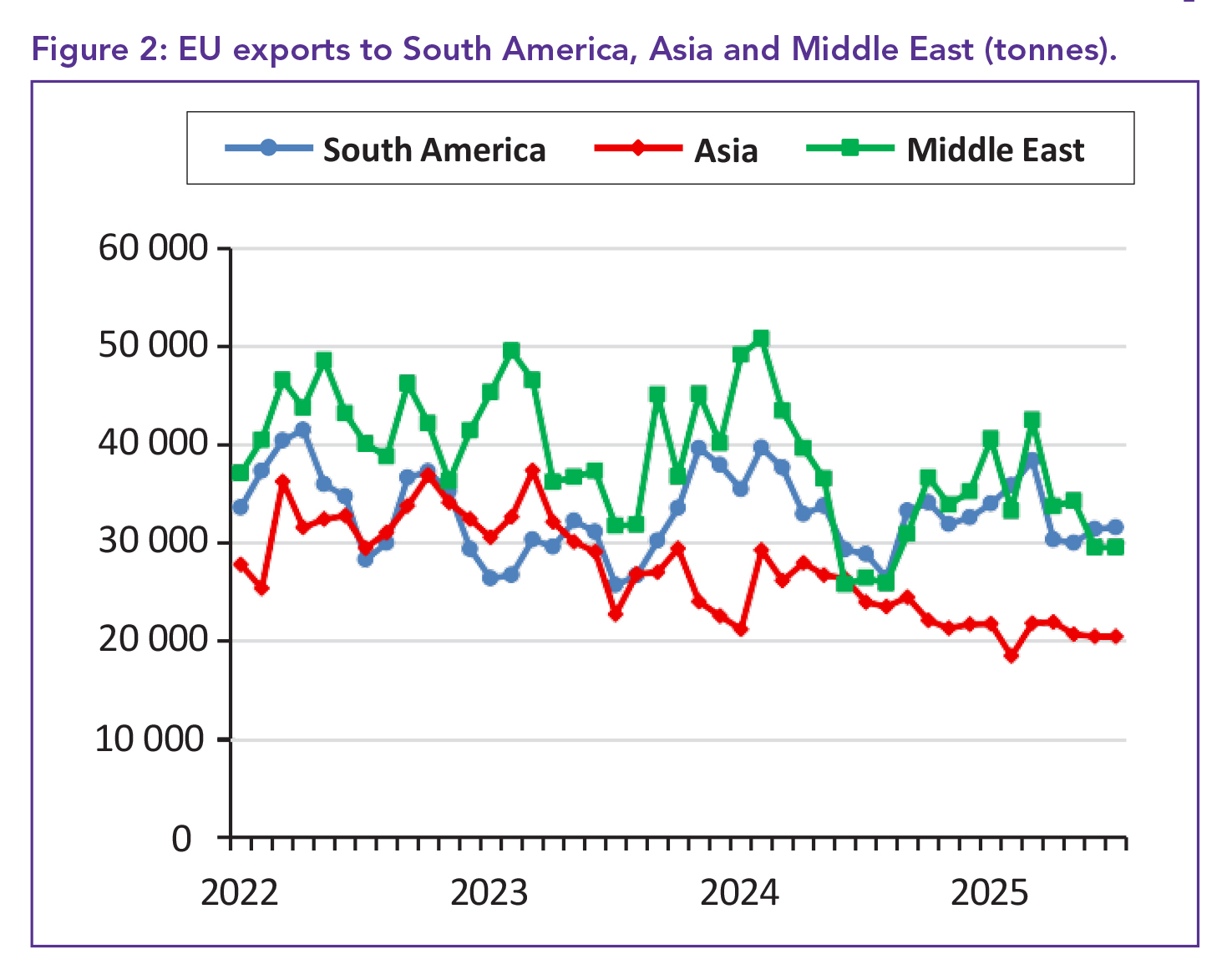

In price-sensitive regions such as South America and the Middle East, significant price reductions were observed. Brazil, for example, paid only €960/tonne, although its volume increase was modest. Chile and Colombia increased their orders, boosting South America’s share to over 13% of total EU sales. In the Middle East, demand continued to grow – driven primarily by Israel and Jordan – despite varied price trends. Five key Middle Eastern countries now collectively account for 12% of EU fry exports.

Closer to home, Eastern Europe recorded an 8.3% YOY increase in sales, though Ukraine and Serbia bought slightly less compared to June. African markets continued to grow steadily, with a 49% increase from July 2024, driven primarily by South Africa. Meanwhile, Australia placed its largest order since November 2024 by purchasing 8 175 tonnes, an 8.6% YOY increase.

Despite regional variations, July’s figures reveal that while demand in major markets remains solid, EU exporters continue to face strong headwinds from global competition – particularly from China and India – and persistent downward pressure on prices.

EU potato yields show slight dip

Potato yields across the EU saw a slight decline in September, according to the EU’s Monitoring Agricultural ResourceS (MARS) agency. The average yield across the 27 member states was reported at 36.5 t/ha, marking a 0.8% decrease from August and a 0.5% drop compared to September 2024. Despite this decline, yields remain 0.3% above the five-year average.

Several major potato-producing countries reported notable declines. Germany’s yields fell by 1% from August to 41.3 t/ha, now standing 4.2% below its five-year average.

France experienced a 2.4% decline to 40 t/ha, while Poland’s yields dropped 1.6% to 31.5 t/ha, though remaining slightly above both last year’s figures and the five-year average. Denmark recorded the steepest monthly decline, with yields plummeting 8.4%, placing it 6.1% below the five-year norm.

In contrast, the Netherlands stood out as the only country to report a monthly increase, with yields rising 0.5% YOY to 43.4 t/ha – 2.8% above the five-year average. Belgium’s yields held steady at 42.3 t/ha, 3.9% above its long-term average. In southern Europe, yields in Spain, Italy, Greece, Portugal, and Romania remained below their five-year averages, contributing to a broadly mixed outlook for EU potato production as the season progresses.

Top EU fry exports hit new lows

Frozen fry exports from the EU’s top five suppliers – Belgium, the Netherlands, France, Germany, and Poland – fell sharply in June 2025 amid weakening demand across Europe. Combined shipments dropped to 434 345 tonnes, marking the lowest monthly total since May 2021 and a 14.9% decline compared to June 2024.

Over the past 12 months, total exports from these five countries decreased by 2.5% to 5.88 million tonnes, while average prices in June fell 4.4% YOY to €1 242/tonne. Belgium, despite remaining the largest exporter, saw a 24.5% drop in June shipments, contributing to an 8.1% annual decline to 2.89 million tonnes. The Netherlands also recorded weaker results, with June exports down by 12.1%, and its annual total slipping 7.4% to 1.73 million tonnes.

In contrast, France delivered a strong performance. Its June exports surged 23.5% YOY to 65 129 tonnes, while annual exports reached a record 721 352 tonnes, up 44.2%. Poland posted a 14.7% increase in annual exports despite a dip in June figures. Germany followed a similar pattern, with softer performance in June dampening overall momentum. As intra-EU sales weaken, shifting demand patterns and price pressures continue to reshape the outlook for Europe’s leading frozen fry exporters.

Export prices under pressure

The global average export price for frozen fries in June was US$1 426/tonne, down 1% YOY, though still 46.7% higher than in 2019.

- Among the top 20 exporters, China recorded the lowest price at US$1 055/tonne, down 17.9% from a year earlier and 36.1% lower than in 2019.

- India’s price dropped to US$1 085/tonne, remaining nearly unchanged from 2019.

- Belgian fries were priced at US$1 348/tonne, a 65% increase compared to 2019.

- The Netherlands saw prices rise 1.3% YOY to US$1 506/tonne – 50% higher than in 2019.

- US prices fell 3.3% YOY to US$1 647/tonne, though remaining 42.5% above 2019 levels.

- Canadian prices fell 6.8% to US$1 357/tonne.

- Brazil was the only major exporter to reduce prices below 2019 levels.

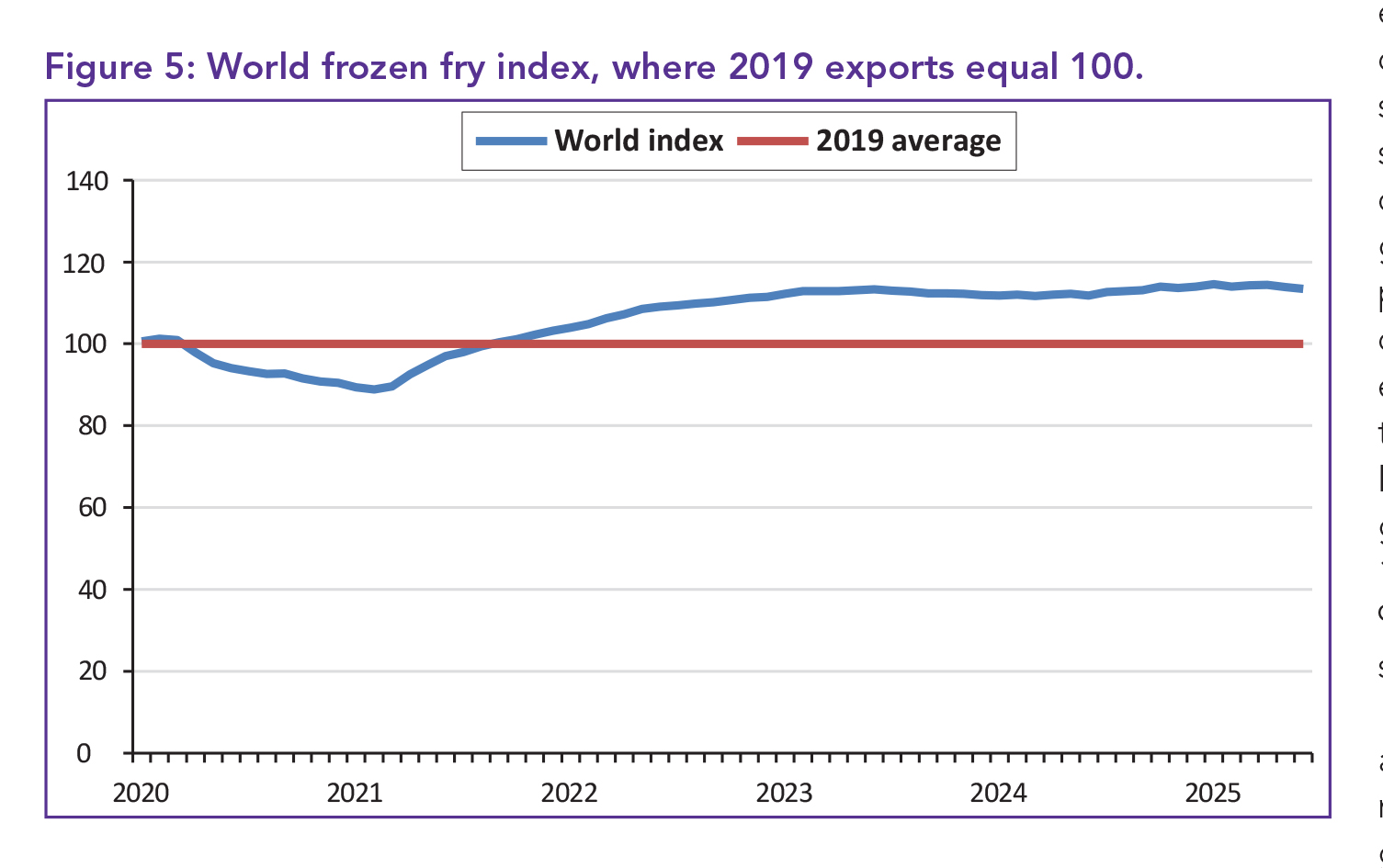

EU sales slow global momentum

The global frozen fry market continued to face pressure in June this year, largely due to weakened demand in Europe. According to World Potato Markets’ frozen fry trade index, global exports fell 4.1% YOY to 740 912 tonnes – the lowest level since May 2021. Nevertheless, volumes remained 10.8% higher than in June 2019, indicating sustained long-term growth.

The index itself edged down to 113.4, a slight decrease from May (113.8) and 1.3 points below the January 2025 peak, as the global market shows signs of slowing. EU exporters were at the core of this downturn. Belgium’s exports dropped sharply by 24.1%, and the Netherlands saw a 12.1% decline. Since these two countries account for roughly 45% of global frozen fry exports, their weak performance significantly dragged down overall trade. In fact, when excluding these countries, global fry trade increased by 13.6% in June.

Despite these short-term setbacks, global frozen fry exports over the past 12 months rose by 1.4%, reaching 9.208 million tonnes – representing a strong 13.4% increase since 2019.

France stood out with a 42% annual increase in exports and has now risen 92.5% since 2019. Its rapid growth, supported by expanded capacity, appears to have come partly at the expense of Belgium and the Netherlands, which together lost 391 000 tonnes in exports over the past year. In contrast, France added 213 000 tonnes.

Meanwhile, China and India continued their remarkable export growth. China’s exports rose by 92.6% over the past year to 290 000 tonnes, representing a 2 475% increase since 2019. India also saw robust growth, with exports up 35.9% YOY and 653% over the past six years. Türkiye has also experienced strong export growth since 2019, although its momentum has recently slowed.

Germany

Germany’s potato market is under significant pressure as oversupply and sluggish demand continue to weigh heavily on prices. The first processing price of the 2025/26 season, reported by the German organisation REKA, has plunged to just €45/tonne, with offers ranging between €40 and €50.

This marks the lowest start-of-season price in five years, matching levels last seen during the Covid-disrupted 2020/21 season.

In sharp contrast, prices at the same point last year opened at €160/tonne and surged to as high as €450 before collapsing below €100 by the end of the season. Weather conditions have added further complications. Recent temperatures exceeding 25°C in northwest Europe have raised concerns regarding tubers being too warm for safe storage.

However, earlier rainfall has softened the soil, easing harvest conditions. With cooler temperatures now returning below 20°C, and forecasts calling for sunshine and intermittent showers, growers should benefit from improved lifting conditions.

Still, with more potatoes entering the market and limited free-buy activity, downward price pressure is expected to persist in the coming weeks.

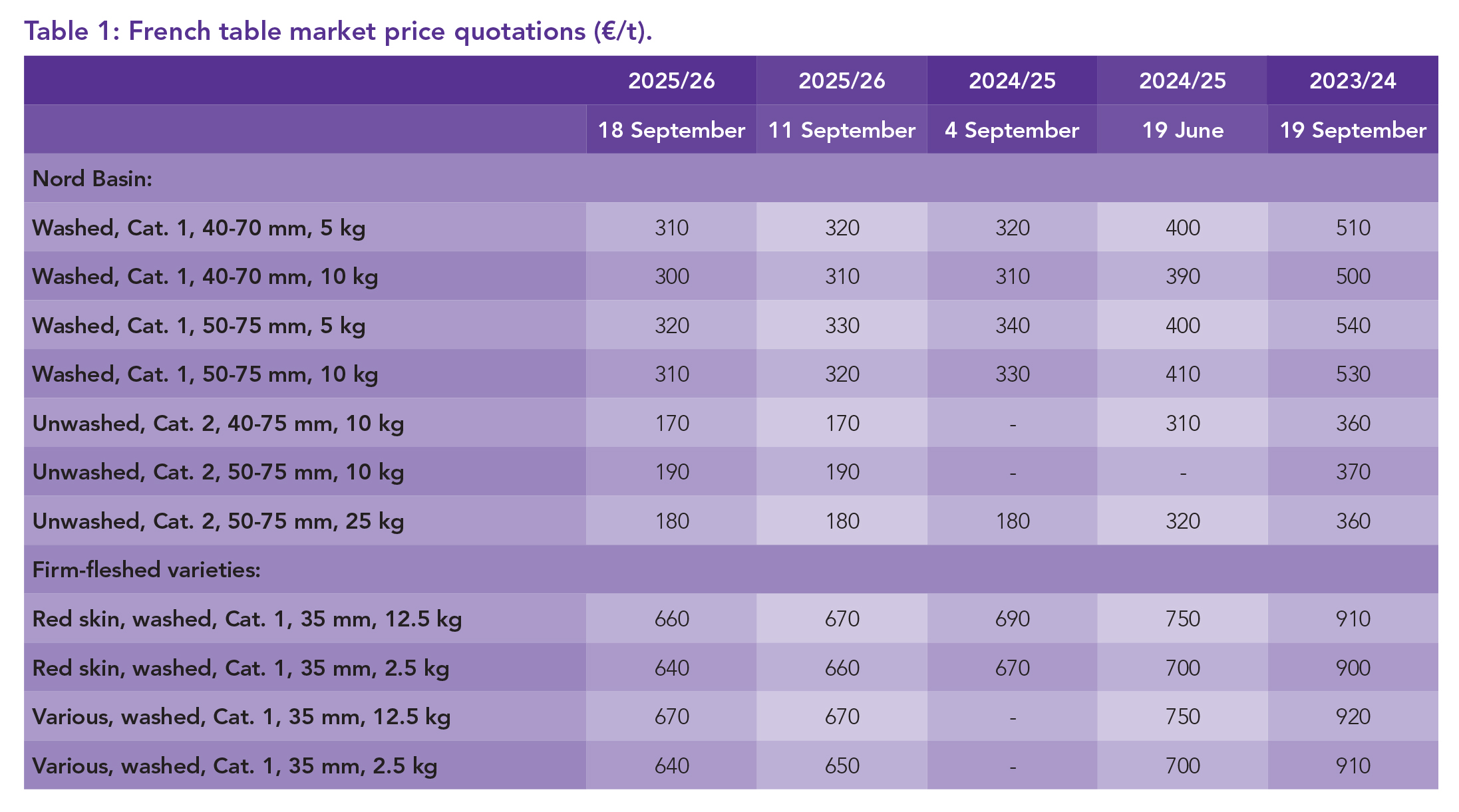

France

Table potato prices in France dropped in September as increased market supply continued to exert downward pressure. The benchmark Nord Basin price for Category 1 (10 kg pack) potatoes dropped €10 to €300/tonne, now €200 lower than at the same time last year. Prices haven’t been this low since the 2020/21 season, when they remained below €300 despite a surge in fresh potato consumption during the pandemic. Other varieties also recorded similar declines, with firm-fleshed potatoes now trading between €640 and €670/tonne, well below the €1 000-plus levels seen two years ago.

While export prices held steady week-on-week, the bulk Agata benchmark slipped to €140 per tonne, dipping below 2020/21 levels. This reflects ongoing weakness in both domestic and export markets.

Poland

Potato prices in Poland have collapsed to their lowest levels in years, with wholesale and free-buy prices down over 50% YOY, and more than 60% below 2023 levels. The situation by late September was as follows:

- Wholesale prices averaged PLN 0.47/kg (€0.11), compared to PLN 1.07 to 1.50/kg (€0.25 to €0.35) at the same time last year.

- Free-buy prices at buying stations had dropped to PLN 0.35 to 0.50/kg (€0.08 to €0.12) – well below production costs.

- Retail shelf prices remained relatively stable, averaging PLN 1.50 to 2.50/kg (€0.35 to €0.59), with supermarket promotions offering temporary discounts.

The sharpest pressure was felt by producers and wholesalers, while consumers benefitted from lower prices at checkout. The market continues to struggle with a significant oversupply amid persistently weak demand.

The Netherlands

The first PotatoNL quote of the 2025/26 season saw Category 2 prices average €80/tonne, ranging from €50 to €110. While this is slightly above the €65 per tonne recorded in July, it remains well below the highs typically seen in previous season openers. No quote was issued for Category 1 potatoes. For comparison, in September 2022, Category 2 potatoes averaged €255/tonne, highlighting the current market’s softer tone amid ongoing supply pressure.

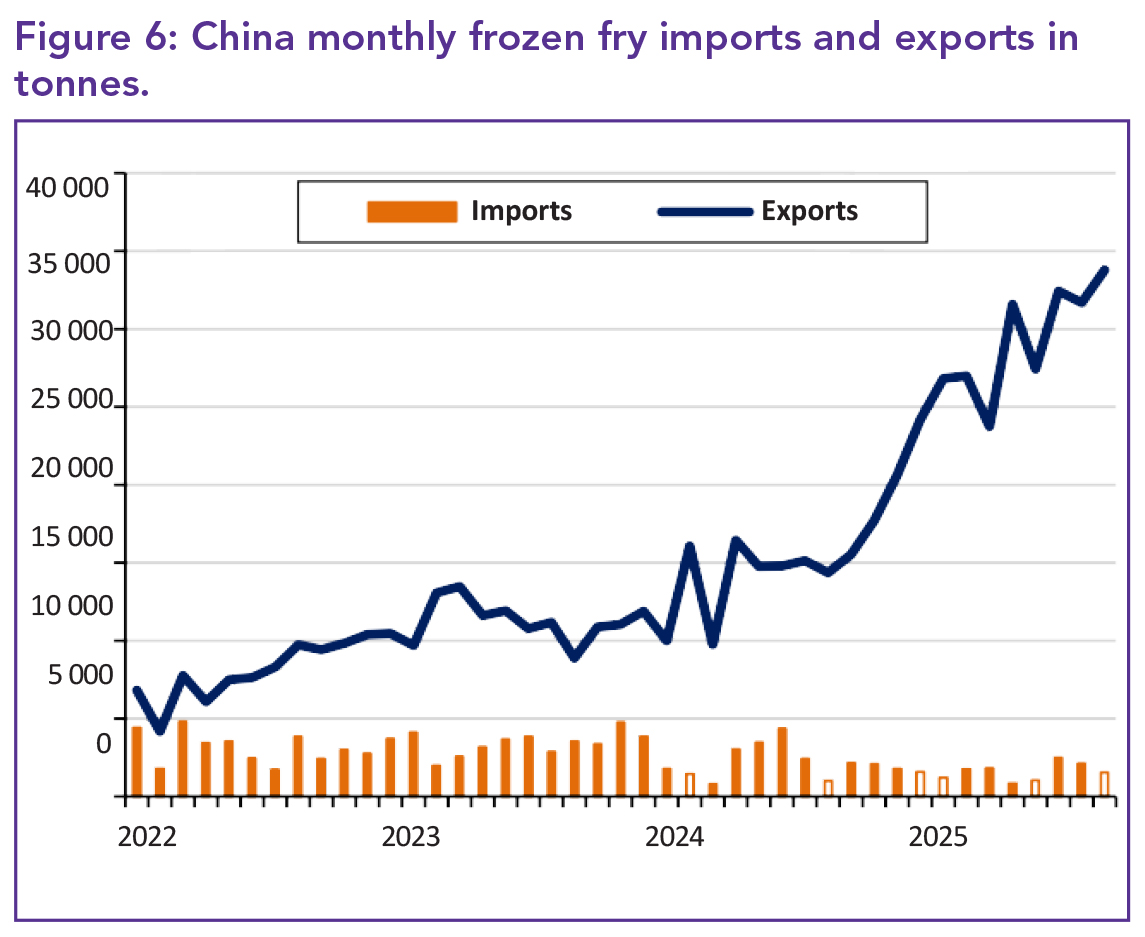

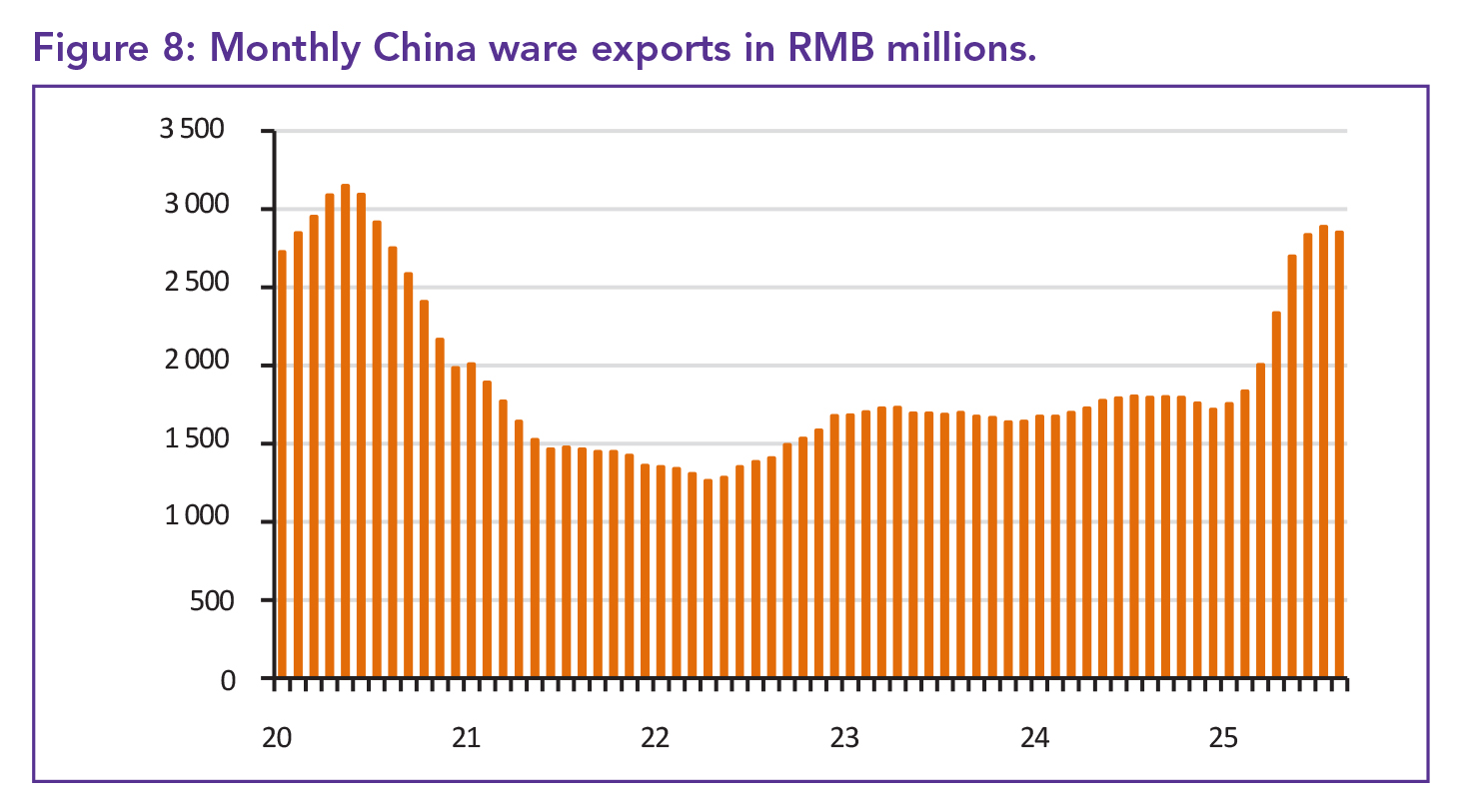

China

China’s frozen fry exports reached a record 33 778 tonnes in August, driven by a major order from Indonesia, which doubled its monthly intake to 5 340 tonnes – a 109% YOY increase – supported by a 6.1% price drop.

The Philippines remained China’s top buyer by importing 5 620 tonnes, while Japan and Thailand reduced their volumes despite lower prices. Saudi Arabia and Hong Kong increased their purchases, with Hong Kong placing its largest order in a year.

Despite the rising export volumes, China’s average export price held steady at RMB 7 513/tonne (€899). Monthly fry export earnings nearly doubled to RMB 254 million (US$35.7 million) compared to August 2024.

On the import side, China bought 1 552 tonnes of fries, down 28% YOY. Belgium was the top supplier, with rising prices, while sales from the US and Netherlands fell sharply. Total fry imports over the past year remain 37.5% lower than the previous 12 months.

China’s bull market in fresh potato exports has cooled, with August shipments dropping by 17 283 tonnes to 67 232 tonnes, as local harvests in Russia and Kyrgyzstan reduced demand.

- Russia’s orders fell sharply to just 5 752 tonnes, down from 35 600 tonnes three months ago.

- Kyrgyzstan cut its purchases to 2 475 tonnes, though it remains China’s top fresh potato buyer this year by value, spending over RMB 923 million (€110 million).

Meanwhile, demand in Southeast Asia remains strong:

- Malaysia bought 17 796 tonnes, a slight decrease from July.

- Vietnam increased its orders to 16 088 tonnes, supported by a price cut.

- Sri Lanka’s demand has more than doubled YOY, reaching 49 717 tonnes annually.

- Thailand also raised its orders to 6 669 tonnes.

Despite the slowdown in August, China’s total fresh potato exports for the year are up 79%, reaching 946 015 tonnes. – Ané du Plessis, Potatoes SA

For more information, email the author at ane@potatoes.co.za or visit www.potatoes.co.za