Estimated reading time: 20 minutes

Average potato yields in the European Union (EU) remained stable at 35.1 t/ha, slightly below the five-year average. Denmark recorded the highest yield (44 t/ha), followed by Germany at 41.1 t/ha while Greece experienced a significant 19.7% drop due to extreme heat. Weather forecasts predict mixed conditions, with potential challenges for growers in southern Europe (Spain, Portugal, Romania, and Poland).

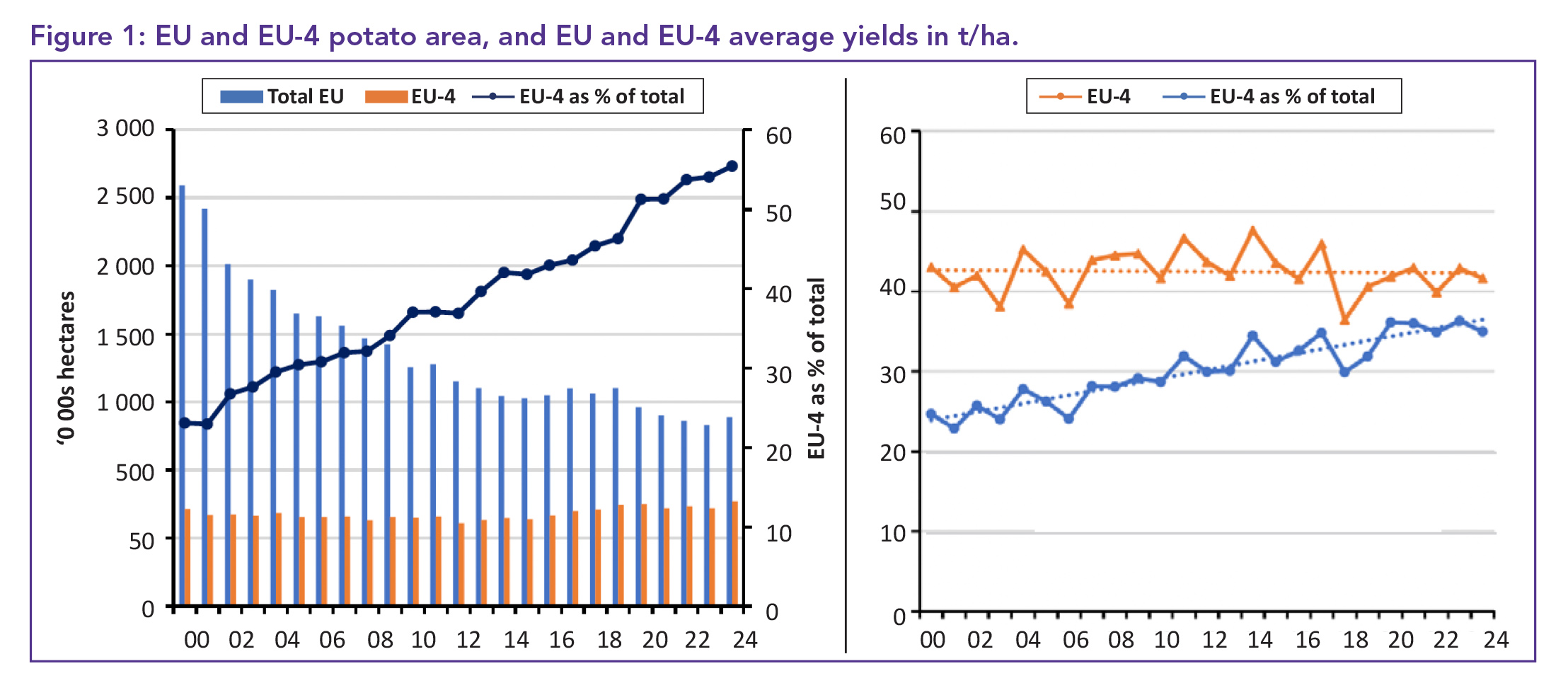

The EU potato growing area for this year is projected to rise by 7.9% to 1.396 million ha in 2024, primarily driven by major producers such as France, Germany, the Netherlands, and Belgium, which collectively account for 770 400 ha.

The total EU potato crop for 2024 is estimated at 48.902 million tonnes, with a more optimistic projection of 51.327 million tonnes, marking the largest harvest since 2020 (Figure 1).

Largest crop in 20 years

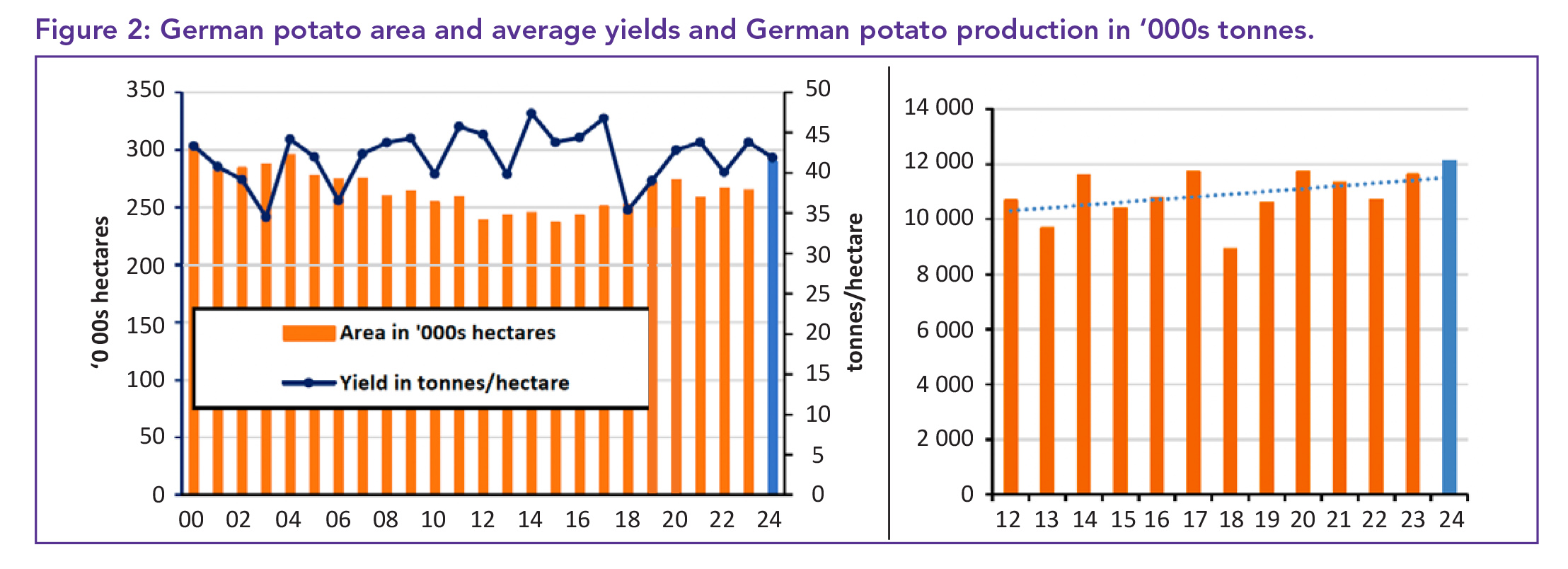

German potato growers are set to achieve their largest crop in 20 years, with a 9.3% increase in plantings to 289 200 ha, the highest since 2004. Niedersachsen, the largest potato-growing state, reported a 16% increase in acreage. However, Bayern saw a decrease of 7.3%.

If average yields were to match the last five years (41.9 t/ha), production could reach 12.117 million tonnes, a 4.4% increase from 2023 (Figure 2). In a best-case scenario, yields could result in a record harvest of 13.708 million tonnes. Current potato prices are declining due to the anticipated larger crop, with processing potato prices averaging €232.50/t, down €30 from last week.

More crops are said to be harvested due to the new crop market that stabilise. Recent rain in Germany is expected to delay or halt further lifting, and cooler temperatures are reducing growth potential. The market is primarily supplied by contracted potatoes, with growers holding back quality stock for later sale.

However, the influx of new potatoes has led to a slight price decrease. The average price reported by the Rhineland organisation, REKA, dropped by €2.50 to €160/t, though the price range between the lowest (€125) and highest (€195) prices is widening compared to the previous week. Currently, prices are €60/t higher than at the same time last year, reflecting rising values as the harvest becomes more challenging.

Retail demand for fresh potatoes has shown a slight decline in recent months, potentially due to elevated prices over the past year. Despite this, sales remain higher than pre-Covid levels, reflecting a robust baseline for consumer demand. According to market research firm GfK and the AMI newsletter, retailers sold a total of 101 000 tonnes of fresh potatoes in July. This figure represents an 8% drop compared to the same period in 2023, indicating that while demand has softened, it continues to perform well compared to historical trends.

Potato demand declines in France

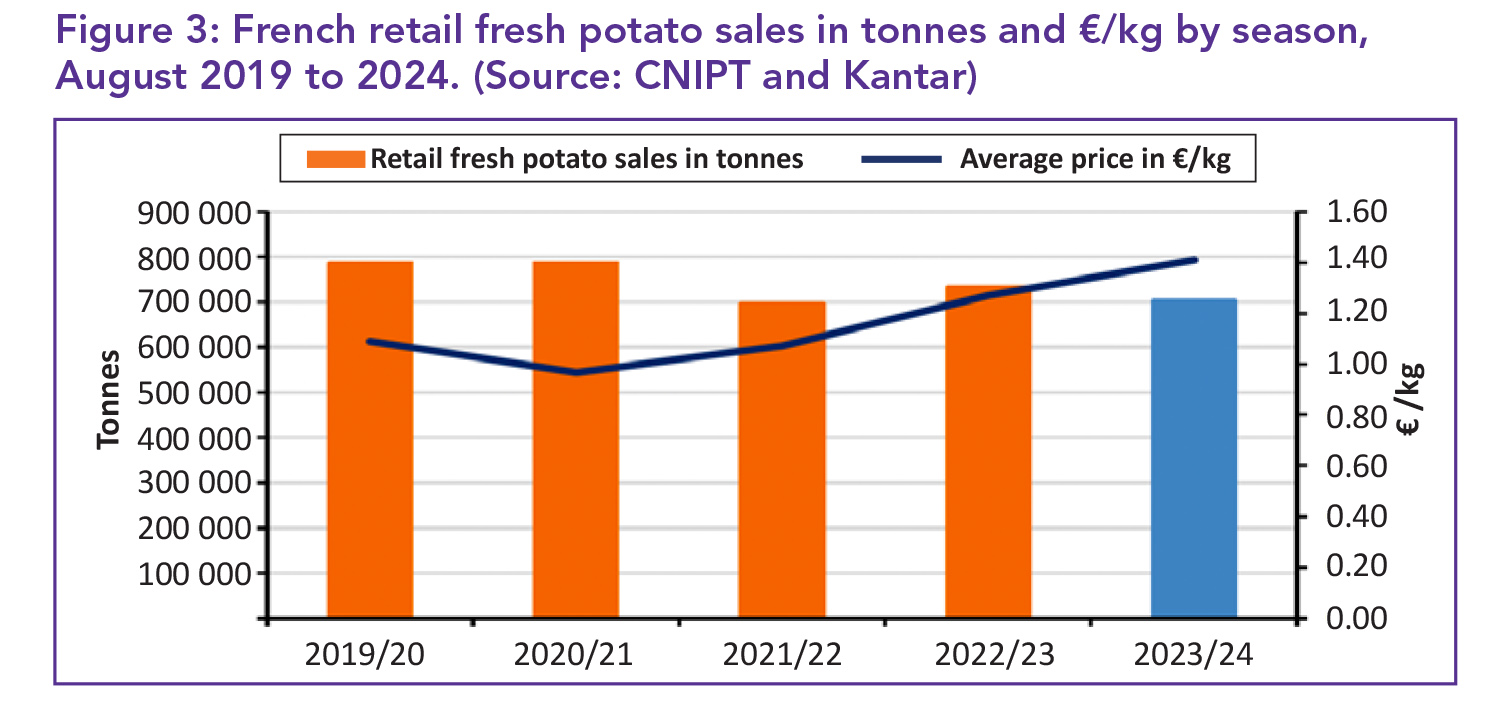

A sharp decline in fresh potato demand in July and early August is said to have led to lower seasonal sales. In the four weeks leading up to 4 August, French retailers sold 37 406 tonnes of potatoes, down 8.7% compared to the same period last year. While this was a 0.9% increase from 2022, it remained over 11% lower than sales during the Covid years of 2020 and 2021.

Potato prices were up 6.4% year-on-year, averaging €1.93/kg. Discounters saw a 15.6% rise in demand, contrasting with a 12.6% drop in hypermarket sales, while convenience and online sales fell by nearly 8% (Figure 3).

The processing potato industry in France reached record levels in the 2023/24 season, with usage increasing by 12.9% to 1.608 million tonnes. The opening of a new processing plant by Belgium’s Clarebout contributed to this surge, with contract sales representing 77.9% of processing usage. Despite significant growth, French processing still trails behind Belgium and the Netherlands.

However, the establishment of new processing facilities suggests ongoing increases in usage. Early potato prices are under pressure due to increased supply, with wholesale prices for Agata potatoes dropping to €1.15/kg.

Price decline in Belgium

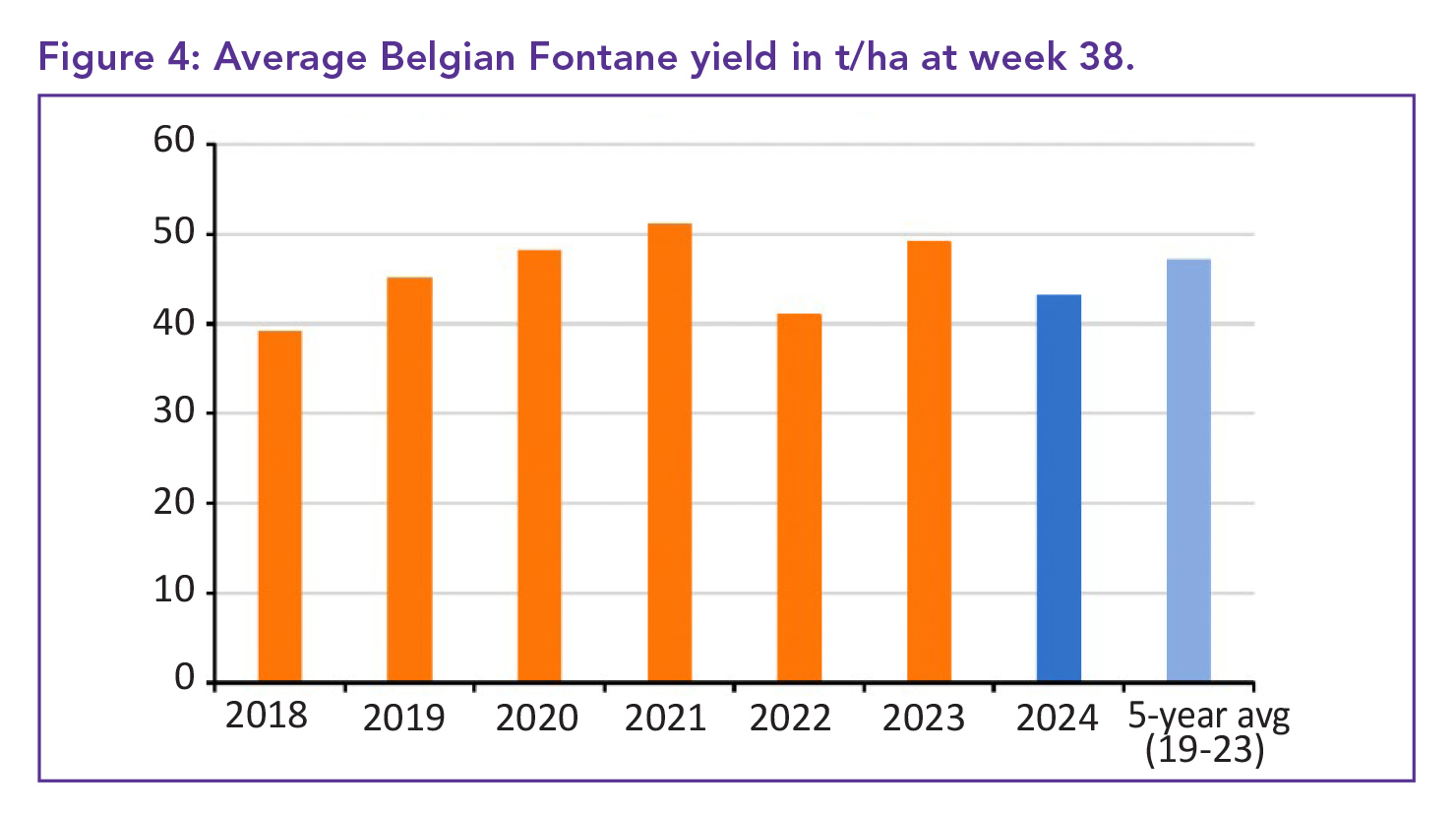

Belgium reported positive early yields, with average yields of 48 t/ha for early varieties such as Amora. Prices have, however, declined significantly due to increased supply. The average price of €175/t received compares to €450/t a year ago and is lower than 2022 and 2021 prices at a similar point in the season. Average yields are currently behind previous years, but this is due to the delayed planting of crops rather than a lack of growth.

The price of free-buy potatoes stabilised at €125/t, the lowest for this period since 2020. Belgium’s potato market faces quality concerns, particularly for the Bintje variety, leading to price maintenance amid low supplies (Figure 4).

Netherlands: New potato platform

A new platform called Service to Potato (S2P) was launched to enhance transparency in the free-buy processing potato market, allowing growers to list their potatoes and receive buyer offers (www.service2potato.com/en).

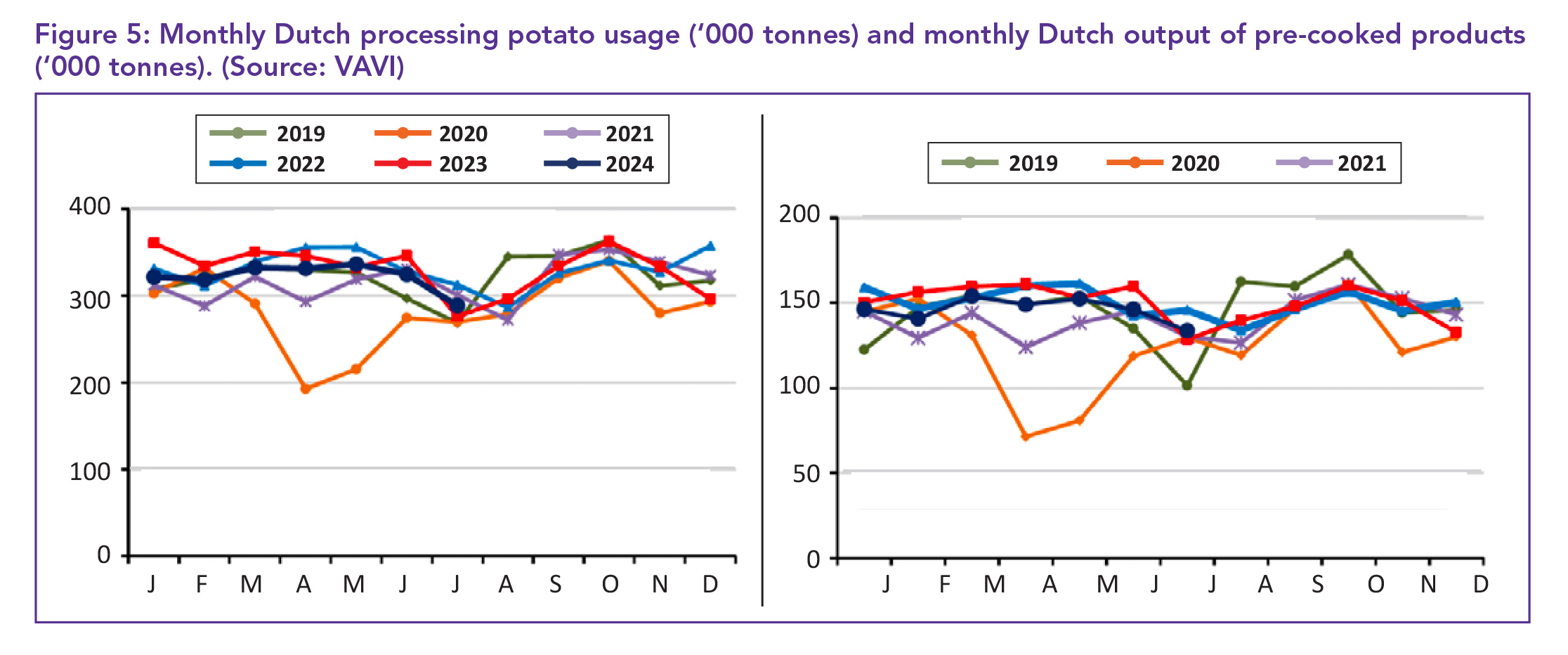

End-of-season potato availability increased by 4.5% in July, reaching 288 500 tonnes, though still below July 2022’s 312 700 tonnes, according to VAVI. Pre-cooked potato product output grew 3.9% in July, but seasonal production fell 2.6% (Figure 5).

Other product output, including dehydrated potatoes, dropped 8.4% in July. Dutch potato availability may rise in 2024, but yields remain below the five-year average. Prices vary widely, ranging from €125 to €300/t based on quality.

Spain fears reduced demand

Ex-farm potato prices remain high but dropped by 5.7%. Despite the decrease, this is still an unprecedented high price for this time of year, and it is not expected to decline in the short term. Concerns, however, are that the high prices might reduce consumer demand, particularly after a busy tourist season. Spain’s potato production is projected to remain below two million tonnes for the third consecutive year, impacting prices.

Improved prices in Portugal

Potato prices in Portugal were 90% higher compared to the triennium of 2021 to 2023. The average ex-farm price of new potatoes in Portugal was €570/t in the week to 25 August, unchanged from that of the previous week, but 48.7% up on that of the same week last year and 80% higher compared to the same week in the triennium 2021 to 2023. Ware potato prices varied by market, ranging from €500 to €700/t.

Weather challenges in Polland

In Poland, the area under potato cultivation likely increased by 6% compared to 2023, reaching 200 000 ha. Yields are expected to rise by 8% to 32 t/ha, leading to a forecasted production of 6.4 million tonnes, the largest crop since 2021. However, this is still historically low, at just over a quarter of the 2000 harvest.

Weather conditions in July and early August were favourable, though excess rainfall caused potato blight in some regions. Potato prices dropped significantly by 15% since early August, with current prices ranging from PLN0.60 to 1.00/kg in large wholesalers. White potatoes, grown mainly in Mazovia, held a premium price of PLN1.00 to 1.50/kg. Despite improved yields, crop conditions were impacted by weather challenges and disease.

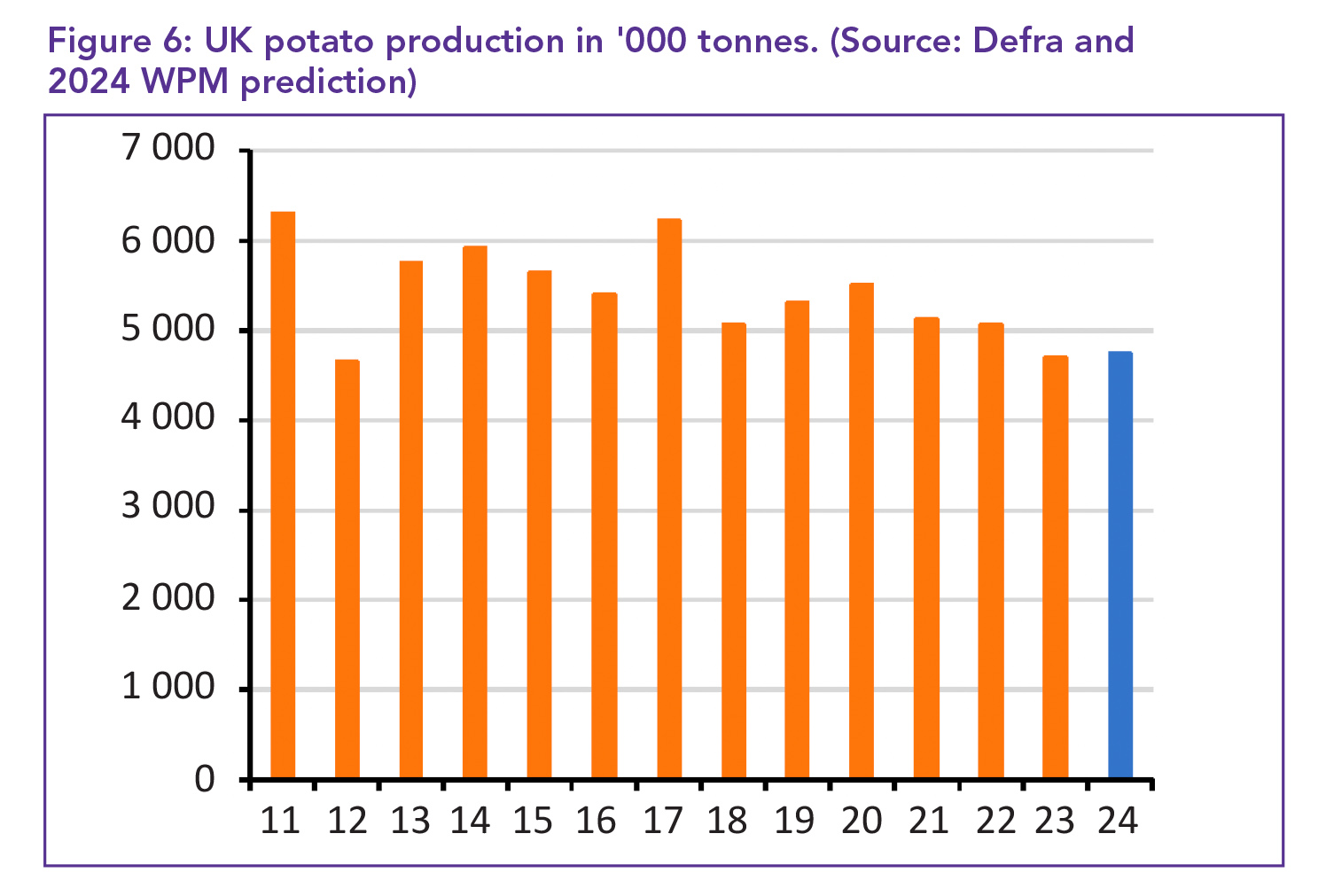

Small crop in UK

British growers planted around 100 000 ha, similar to 2023, the smallest area on record. The estimated 2024 United Kingdom (UK) potato production is around 4.751 million tonnes, but some predict it could be as low as 4.2 million tonnes, potentially the smallest crop on record. Although reduced planting has kept prices high, production costs have also increased, with growers needing confidence in sales to continue planting (Figure 6).

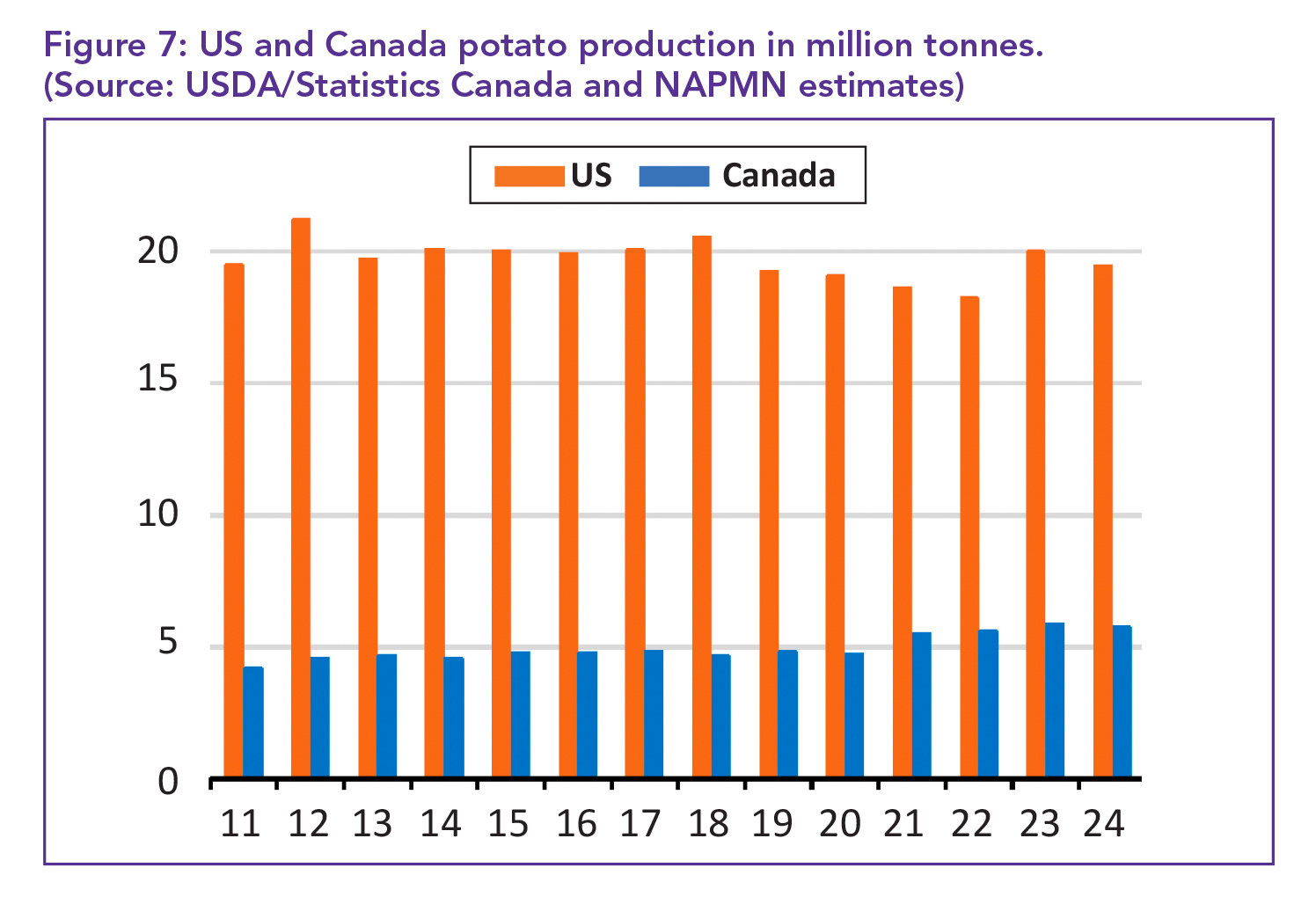

North American smaller crops

The North American potato crop is expected to be slightly smaller in 2024 compared to last year. The United States (US) crop is estimated at 19.45 million tonnes, 2.7% less than in 2023, with a similar yield in Idaho but a larger decline in Washington. Canada’s crop is forecasted to be 1.7% smaller at 5.742 million tonnes, still the second largest after last year’s record. The combined US and Canadian production are expected to be 25.192 million tonnes, down 2.5% from 2023, but still among the largest crops in recent years.

Potato price inflation has eased, helping boost US retail sales by 1.3% in the year ending June, with 6.308 million tonnes of potatoes sold. The total sales value rose by 4.6% to US$18.286 billion, with the average price up 3.3% to US$5.22/kg, a smaller increase compared to last year’s peak inflation. Chips remained the most popular potato product, and while fresh potato sales grew by 2.2% in volume, their value dipped slightly.

Frozen, dehydrated, and refrigerated potato products saw price increases that led to record-high sales values. Over the past five years, the value of US retail potato sales increased by 34.9%, despite a 4.5% drop in volume (Figure 7).

International imports

Some countries experienced increased imports and in others, demand drops led to a decline in imports.

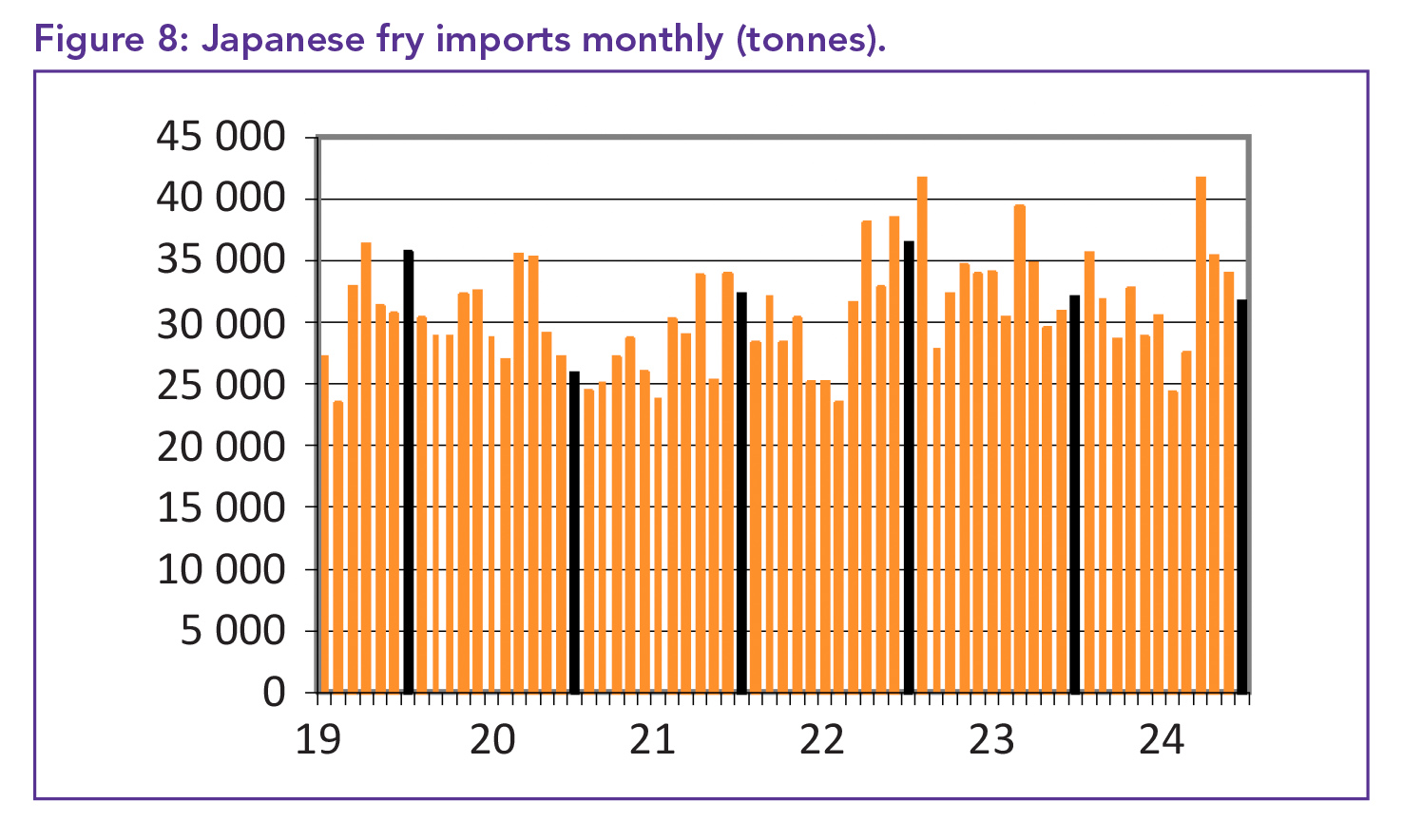

Robust demand in Japan

Japan experienced robust fry demand, increasing imports significantly. Japan’s average fry import price hit ¥282 569/t (US$1 926), increasing by ¥6 900 from previous months. Fry imports decreased for the fourth consecutive month to 31 702 tonnes, a 1.1% drop compared to the previous year. The Netherlands became Japan’s second-largest fry supplier with a 47% year-on-year increase in sales, while Belgian fry imports saw a significant decline (Figure 8).

Demand decline in Chile

In June, rising prices by Chile’s top three fry importers led to a sharp drop in demand, with total fry imports falling by 3 200 to 8 048 tonnes, a 37.1% decrease compared to the previous year. The cost of fry imports in June was US$11.563 million, 36.4% less than the previous year. However, the annual cost of imported fries rose by 23.3% to US$198.735 million over the past year.

Steady strong demand in Brazil

Despite rising fry prices, demand in Brazil remains strong, leading to a 10% increase in the import bill over two months. In July, Brazil spent BR225.824 million (US$41.15m; €37.53m) to import 29 982 tonnes of fries, 51.2% more than the previous year. Argentina remains Brazil’s largest supplier, with a price rise from BR8 004/t in May to BR8 881/t in July, and higher sales at 13 060 tonnes.

Other suppliers, such as the Netherlands and Belgium, also increased prices, resulting in mixed sales outcomes. Dutch fries saw a drop in sales by 1 092 tonnes, while Egypt’s lower-priced fries saw a surge in demand, with sales rising 578.6% to 19 904 tonnes annually. Brazil’s fry export business also grew, with sales up 41.8% year-on-year.

Australia: Record average price

In July, strong demand for imported fries led to a record average price of A$2 366/t (US$1 575/t; €1 427/t), an increase of A$164 from the previous month. After a slow June with imports of 8 487 tonnes, July saw a rebound with imports rising to 11 912 tonnes, though still 31.8% lower than last year.

Belgian and Dutch suppliers dominated, providing two-thirds of the imports, while the US also made significant contributions with its highest sales since May 2023. Belgian fries rose to A$2 407/tonne, and US fries increased to A$2 594/tonne. Dutch fries saw a more modest price rise to A$2 067/tonne but were still 17.1% more expensive than a year ago.

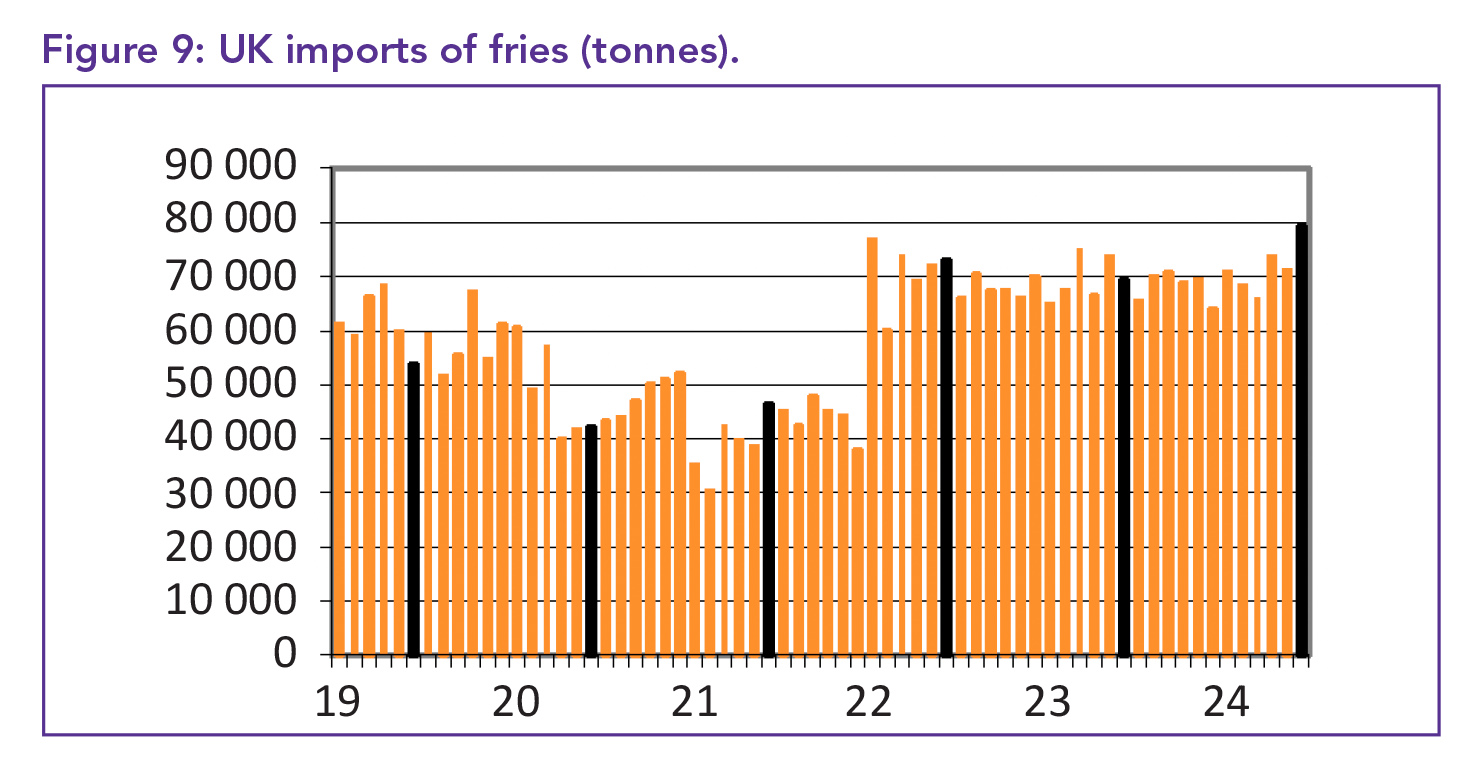

Import record for the UK

In June, the UK achieved a record import of 79 231 tonnes of fries, resulting in a monthly import bill exceeding £100 million for the first time. The total cost reached £103.675 million (US$134.4 million; €121.7 million), a 21.6% increase from the previous year, contributing to a 19.6% rise in annual fry import costs, totalling £1.076 billion (US$1.395 billion; €1.263 billion) (Figure 9).

Thailand and India boost trade

In July, India boosted its trading relations with Thailand by placing its largest-ever fry order of 5 238 tonnes, raising total imports to 9 845 tonnes, just short of the record set in March 2023. India’s fry exports to Thailand increased by 32.3% over the past year, now representing 48% of the Thai market, while China’s share fell to 22%.

India’s average price per tonne was Baht 47 247 (US$1 381/t; €1 248/t). New Zealand became Thailand’s third-largest supplier, with a 16.5% increase in annual sales, while Belgium, the Netherlands, and the US also saw varied sales. Despite July’s surge, Thailand’s annual fry import market value is 6.7% lower at Baht 3.977 billion (US$116.3m; €105m).

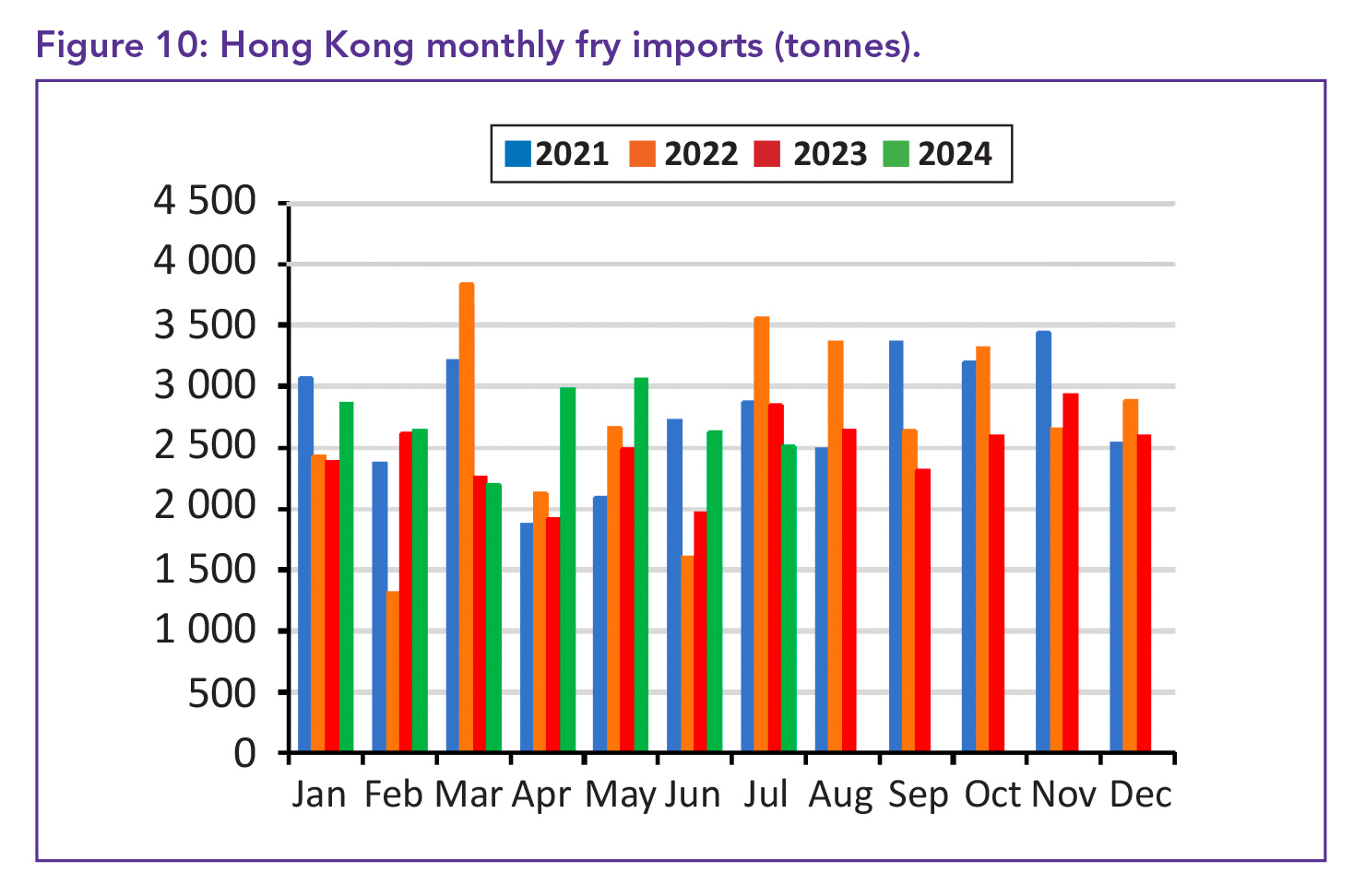

Record imports for Hong Kong

In July, Hong Kong’s fry imports were 11.8% lower than a year ago, though annual imports rose by 2.1% to 31 895 tonnes. US fries remained competitive, with sales rising 17.9% from last year to 1 782 tonnes, despite a price increase. In contrast, China’s July sales dropped by 47.1%, though its annual sales were 54.7% higher at 5 742 tonnes.

US fries maintained market preference, with annual earnings 3.7% higher at HK$310.6 million. Sellers from the Netherlands and Belgium struggled, with Belgium’s sales dropping by 41.3%. India’s presence in the market weakened, while Turkey saw initial interest. The total annual value of Hong Kong’s processed potato imports rose 11.1% to a record HK$476.5 million (Figure 10).

Phillipines

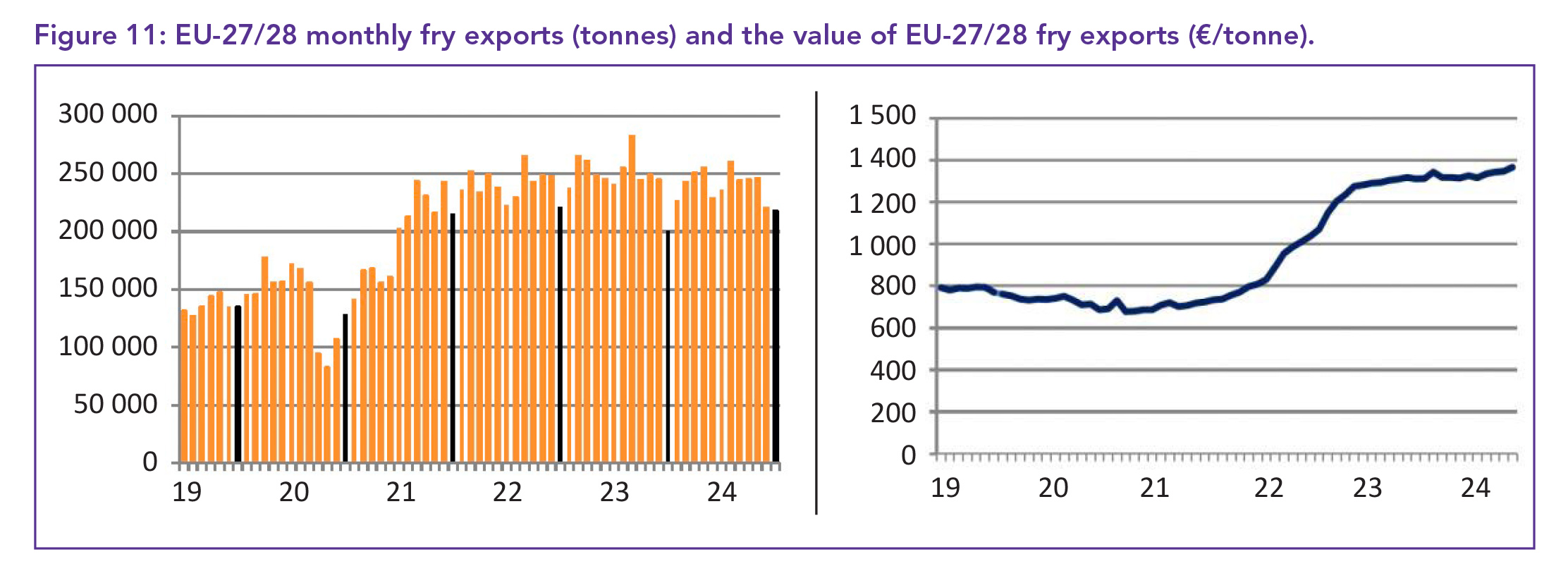

In June, India’s potato fry exports gained ground in the Philippines, taking 30% of the market and closing in on the US’s 34% share. Indian fries, priced at Pso63,825/t (US$1 139/t), were the lowest-cost option, selling at a 23% discount to US fries. In July, EU-27 fry exports for the 2023/24 year were only 3.4% lower than the previous year, despite a smaller harvest across the Union. Total exports reached 2.872 million tonnes, down from 2.974 million the prior year, with July sales increasing by 8.5% to 217 401 tonnes. A significant contributor was a 15.9% rise in sales to the UK, which totalled 72 941 tonnes, with prices up €22 from June to €1 514/t (US$1 683/t). The average EU export price rose 3.7% to €1 366/tonne (US$1 588/t). Excluding the UK, July exports increased by 4% to 144 499 tonnes, while total annual sales fell by 4.7% to 2.038 million tonnes.

The US remained the EU’s second-largest customer, purchasing 15 048 tonnes, 34.2% more than last year, despite a decrease of 3 200 tonnes from June. Annual sales to the US increased by 1.9% to 234 797 tonnes, generating €335.709 million (US$373.18 million). Saudi Arabia’s purchases rose nearly 2 000 tonnes in July, though still 14.1% lower than last year, with a 12.9% price increase to €1 420/t (US$1 579/t).

Sales to South America grew by 10.8% over the past year, totalling 418 936 tonnes, with July sales at 28 864 tonnes. Although Brazil’s purchases declined to 9 039 tonnes, Colombia’s sales approached record levels at 8 540 tonnes. Australia’s fry imports fell 19.5% to 102 312 tonnes, while Japan’s increased by 16.1% to 6 910 tonnes. Overall sales to Asia dropped 18.3% to 315 717 tonnes. Sales to Africa plummeted by 33.9%, while Eastern Europe saw a slight increase of 1.3% in annual sales, driven by growing demand from Ukraine (Figure 11).

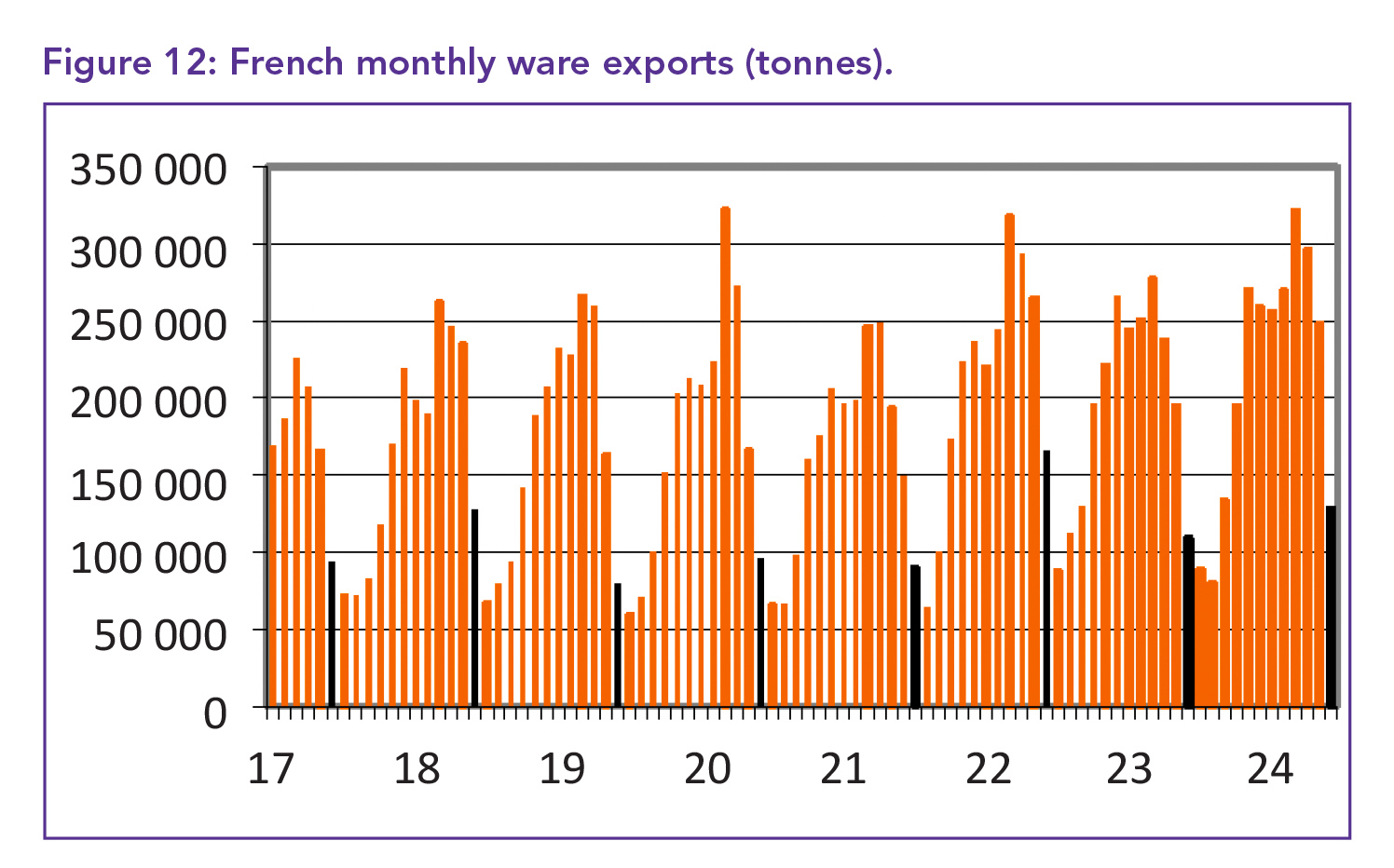

Record exports for France

French ware and seed potato exports reached record levels in the 2022/23 season, with 2.666 million tonnes of ware potatoes exported, an increase of 8.7% from the previous season. This solid performance solidifies France’s position as the world’s largest exporter of fresh potatoes, surpassing Germany by approximately 300 000 tonnes. The total value of the trade exceeded €1 billion for the first time, up 26.8% from last year, with an average export price of €378/t, a 16.7% increase year-on-year. In June, the average price rose to €410/t, a 28.4% increase from June 2023.

Belgium remained the largest market for French potatoes, importing 827 504 tonnes, down 1.5%, with June sales declining by 11.7% to 75 899 tonnes. Exports to Spain also fell by 1.1%, while there were increases in sales to Italy (up 16%), Portugal (up 6.3%), and the Netherlands (up 73.8%). The UK, facing a smaller crop, increased imports, taking in over 3 000 tonnes in June alone (Figure 12).

Germany: Shortage leads to surge

In July, German fresh and ware potato exports surged due to a shortage of potatoes in neighbouring European countries, reaching 163 970 tonnes – over 200% higher than the same month last year. The Netherlands and Belgium were the primary recipients, with demand from the Netherlands increasing by 273% and Belgium by 1 847%. This surge contributed to an annual export total of 2.323 million tonnes, a 16.3% increase from the previous season, and a trade value of €665.7 million, up 46%.

The average price for the year rose by 25.6% to €287/t, with July prices peaking at €398/t, the highest on record. France recorded the highest average price in July at €543/t, while Austria had the lowest at €318/t.

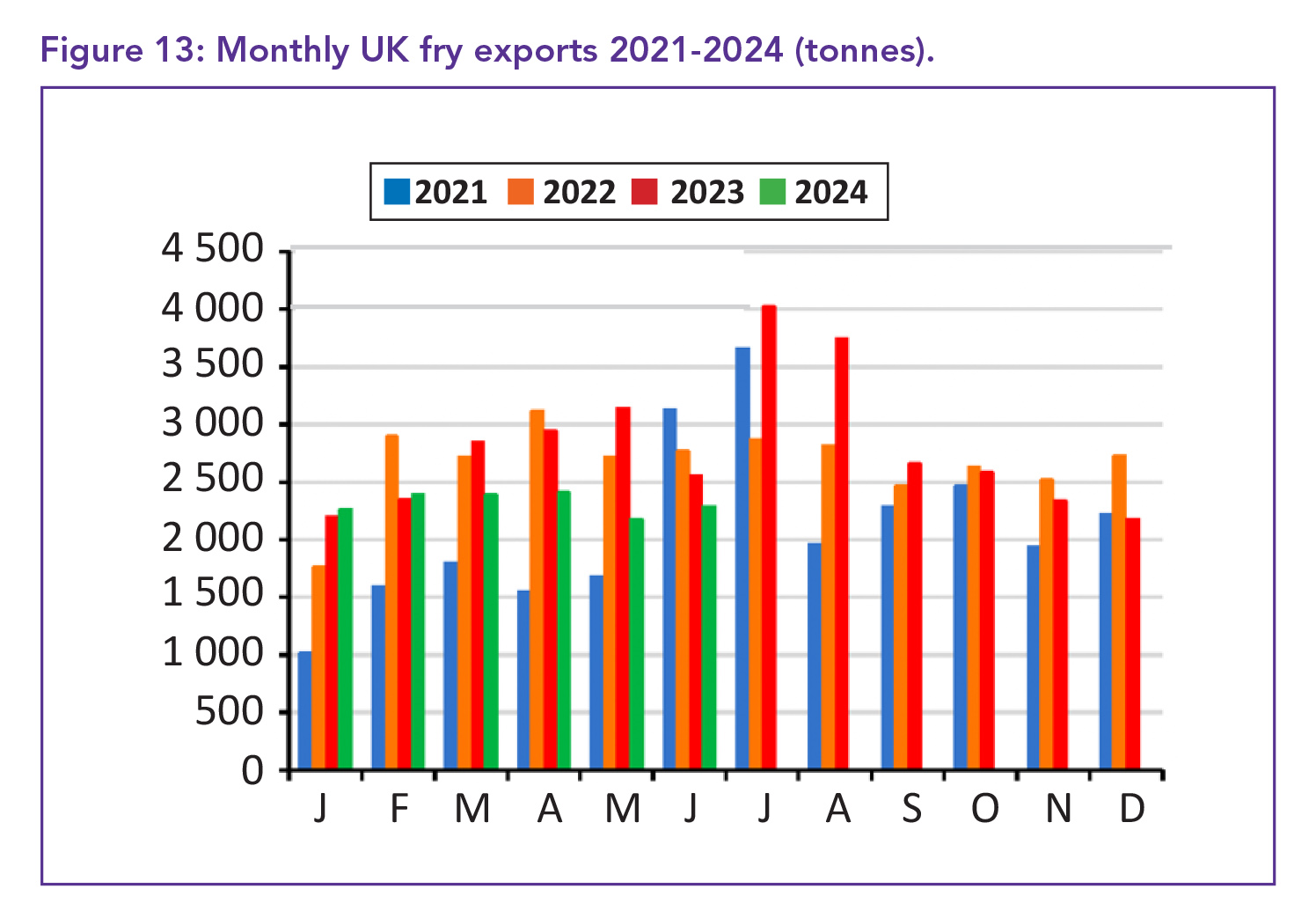

Irish increase UK imports

In June, UK fry exports increased by 110 tonnes from May, reaching a total of 2 281 tonnes. The majority of this demand came from the Irish Republic, which remained steady at 1 859 tonnes. The price for Irish fries rose by £30 to £1 180/t (US$1 530; €1 385), an 8.7% increase compared to last year. Australia, the UK’s second-largest customer, imported only 84 tonnes at a price of £3 202/t (US$4 151; €3 759), which is 32.6% higher than the previous year.

Other countries such as France, the Netherlands, and Belgium imported around 50 tonnes each, while smaller quantities were exported to Hong Kong, the UAE, Iceland, Turkey, and Brunei. Overall, UK fry exports for the year remained unchanged at 31 480 tonnes, but earnings decreased by 3.4% to £43 million (US$55.75 million; €50.5 million) (Figure 13).

The UK ware potato exports for June were subdued at 8 634 tonnes, down 25% from June 2023. For the season, exports totalled 125 582 tonnes, a 34.5% decrease, primarily due to a shortage of British potatoes. The average export price in June rose to £775/t, a 29.9% increase from the previous year, while the overall season average price increased by 43.1% to £618/t. However, this led to a 6.3% drop in trade value to £77.628 million.

Ireland also faced a shortage of potatoes from the 2023 harvest, increasing its imports by 26% in June to 6 448 tonnes, resulting in seasonal sales of 70 159 tonnes – 3.8% more than the previous year. While sales to Spain and France declined significantly, Germany and Norway increased their purchases, although their totals remained relatively small.

UK seed exports were minimal in June, but seasonal trade remained steady at 93 606 tonnes, with an average price of £724/t, reflecting a 4.7% increase compared to the 2022/23 season. The total trade value for the season reached £67.764 million, up 5.1% and the highest recorded from July to June. Egypt was the largest market, accounting for 55% of trade, though demand slightly decreased to 51 878 tonnes. Notably, Saudi Arabia nearly doubled its seed orders, while Morocco, Turkey, Israel, and Serbia also increased their purchases.

Brexit continues to impact UK seed trade due to misaligned phytosanitary rules, limiting free trade. Exports to the Canary Islands fell by 11.2%, and sales from Northern Ireland to the Republic of Ireland decreased by 26.3%. Additionally, UK seed imports dropped by 26.7% to 8 514 tonnes, with the Netherlands supplying 71% of imports, followed by France (17%) and Germany (7%).

Varied trends for US and Canada

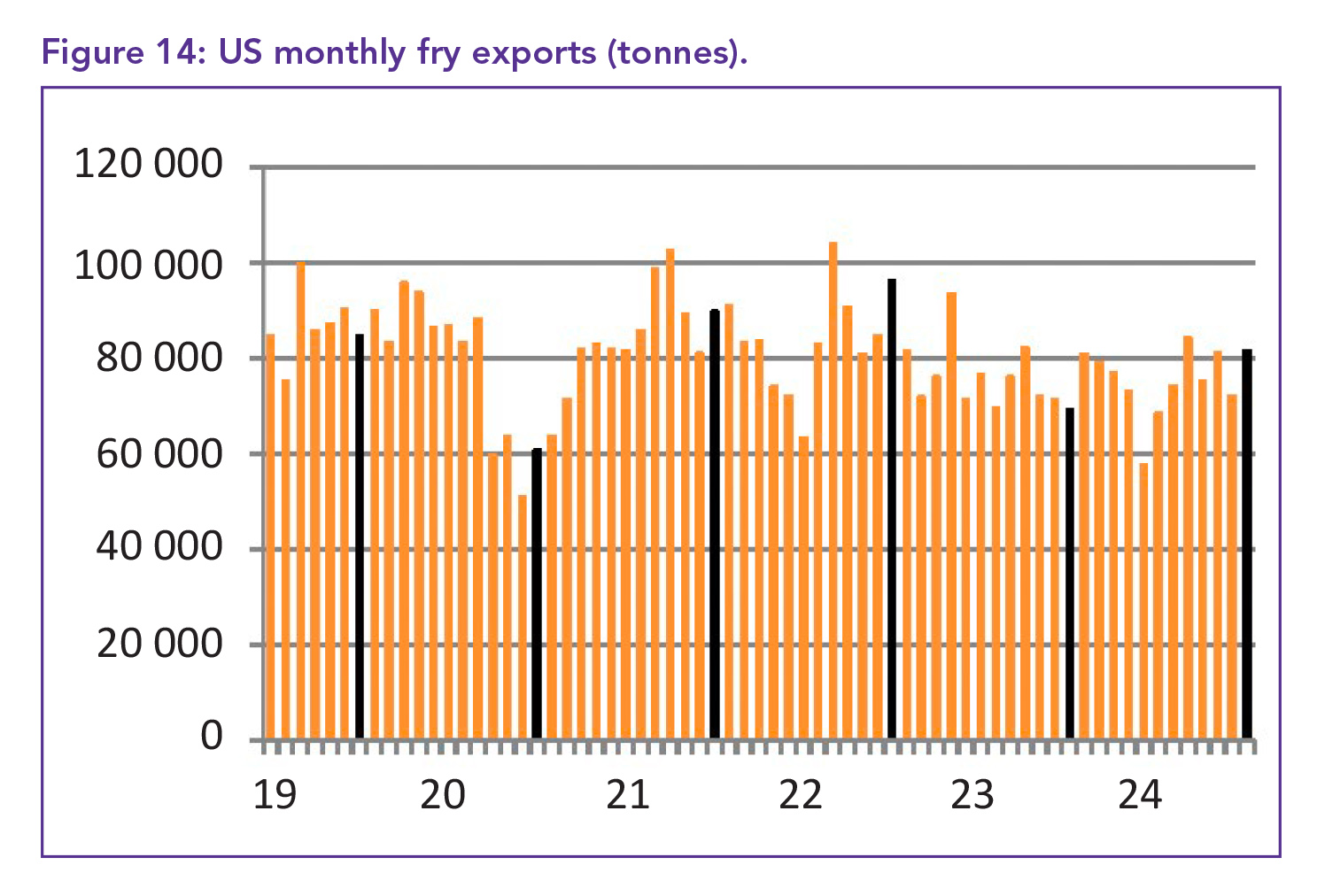

Despite a 10% increase in crop size in 2023, US fry exports fell by 1.2% to 905 988 tonnes. Export earnings rose by 6.9% to $1.53 billion due to higher prices. Canada saw a 4.5% increase in fry exports, benefitting from lower prices compared to the US. US fry imports rose by 2.3%, indicating reliance on foreign sources despite increased domestic production.

Canadian fry exports reached a record 1.408 million tonnes, generating CA$2.682 billion, a 4.5% increase. The US remains the largest market. Imports and exports show varied trends, with some markets improving while sales to the US declined. The US became the EU’s second-largest market for processed products, with a significant 14.5% annual growth (Figure 14).

Price drop in Turkey

A significant drop in the average export price of Turkish fries, almost €100 over four months, helped maintain sales, with July recording 5 144 tonnes sold. This is 900 tonnes more than June but 10.3% lower than the previous year. The average price fell to €1 211/t (US$1 341/t), an 8.1% decrease from last year.

Demand was strongest from Russia, which purchased 2 885 tonnes at €1 196/t (US$1 324/t), down from June. Russia remains Turkey’s largest fry customer, though its share has decreased to 55%, with Iraq and China increasing their orders.

Iraq doubled its purchases to 1 008 tonnes, while China’s purchases tripled to 662 tonnes. Sales to Cyprus remained steady at 144 tonnes, while Greece’s orders rose to 83 tonnes. Despite a 14.5% decline in Turkey’s annual fry sales to 76 258 tonnes, this figure is still 73% higher than in 2019. Export earnings fell 23.4% to €97.080 million (US$107.5m), but the loss in Lira terms is minimal due to currency depreciation.

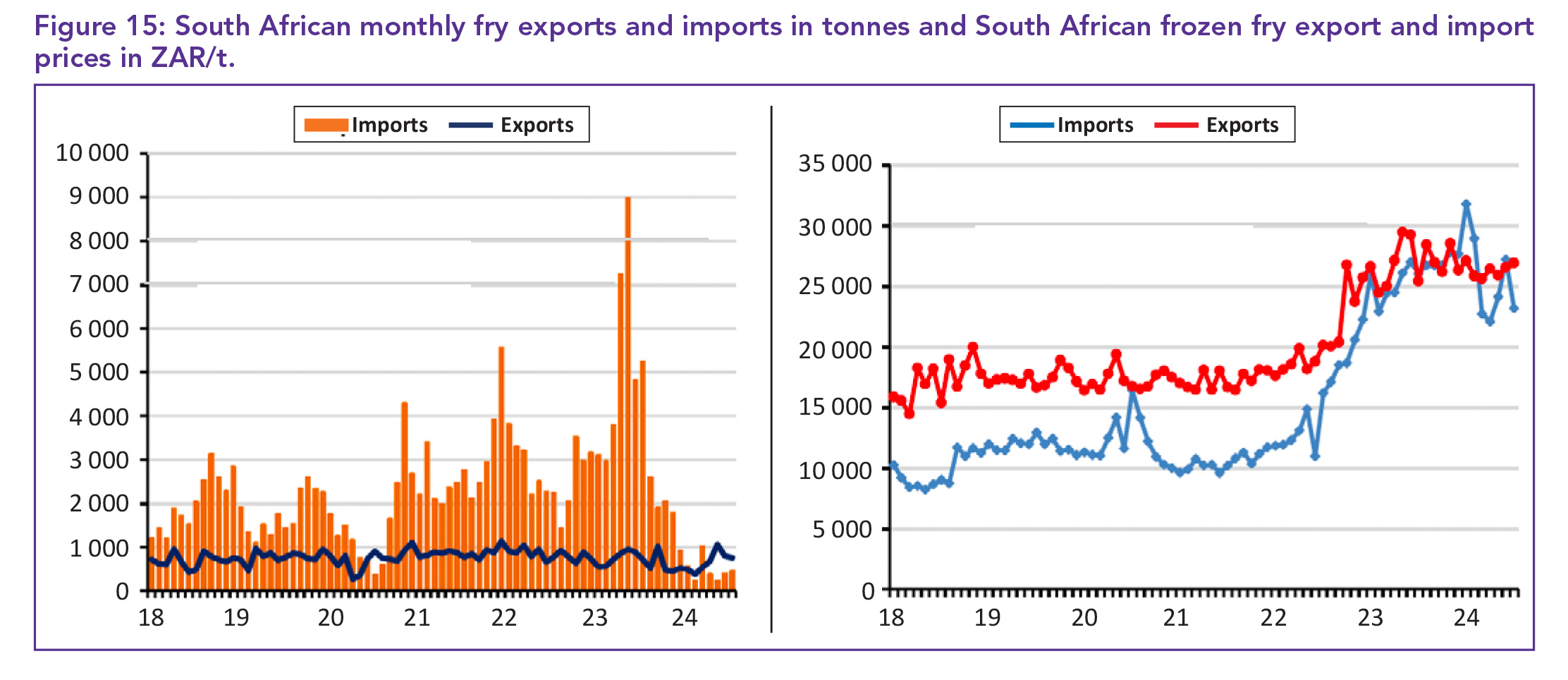

South Africa: Exports increase

In July, South Africa’s frozen fry exports exceeded imports for the fourth consecutive month due to import restrictions. Only 457 tonnes were imported, 91.3% less than July 2023, while 757 tonnes were exported, a 6.6% increase from last July. Over the past year, exports totalled 12 497 tonnes, down 74.6% but almost 5 000 tonnes higher than the previous year.

Imports have dropped significantly, and exports may soon surpass it annually. The US was the only country to increase its supply, with 20 tonnes, while European suppliers saw over 80% decline. The UK experienced a market growth of 205.6%, and India’s trade rose by 6.7% (Figure 15).

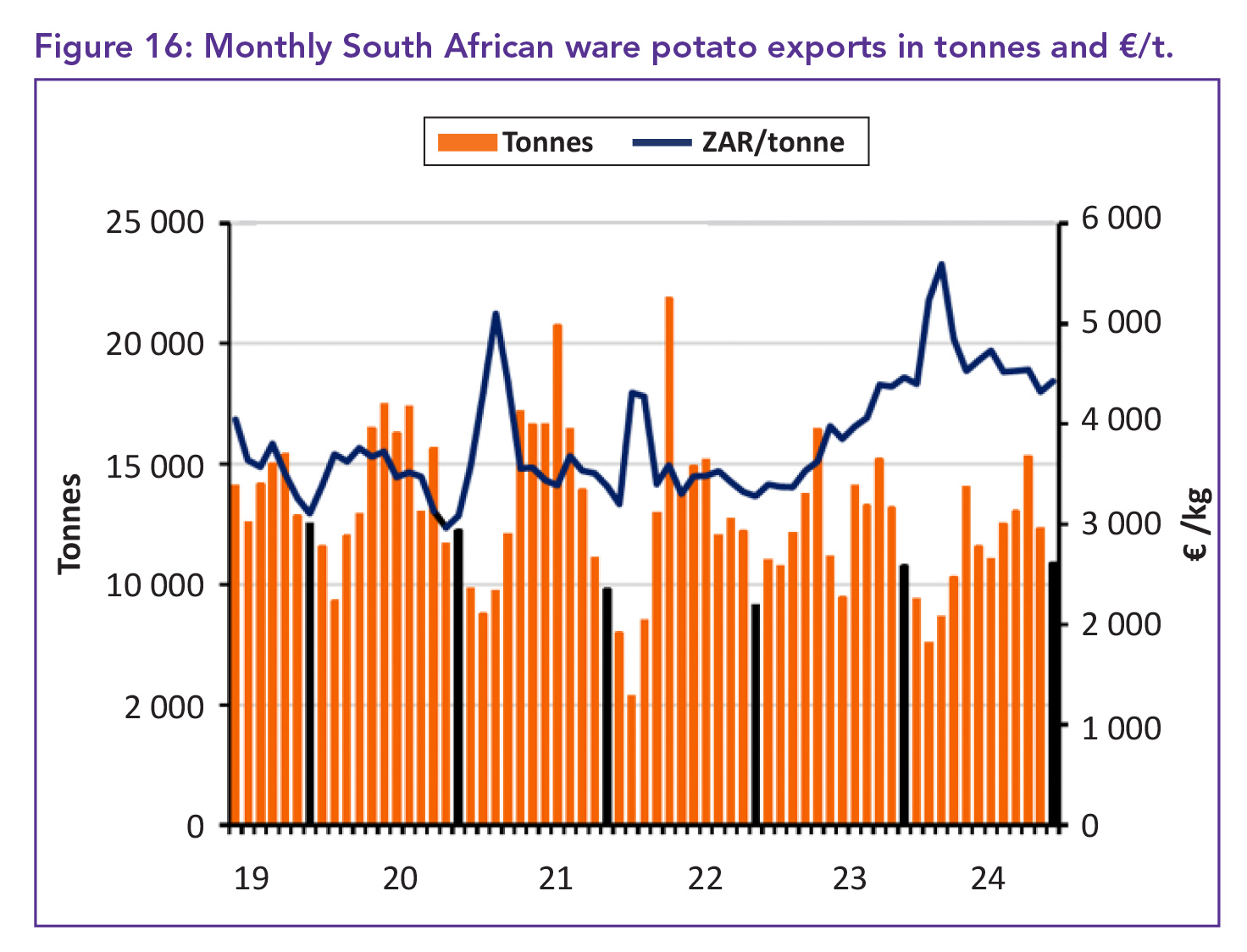

South Africa exported 136 396 tonnes of ware potatoes in the last year, 9.6% less than the previous year. Mozambique was the largest buyer (65%), followed by Namibia (17%) and Eswatini (7%) (Figure 16). –Anje Venter, Potatoes SA

For more information, email the author at anje@potatoes.co.za