Estimated reading time: 13 minutes

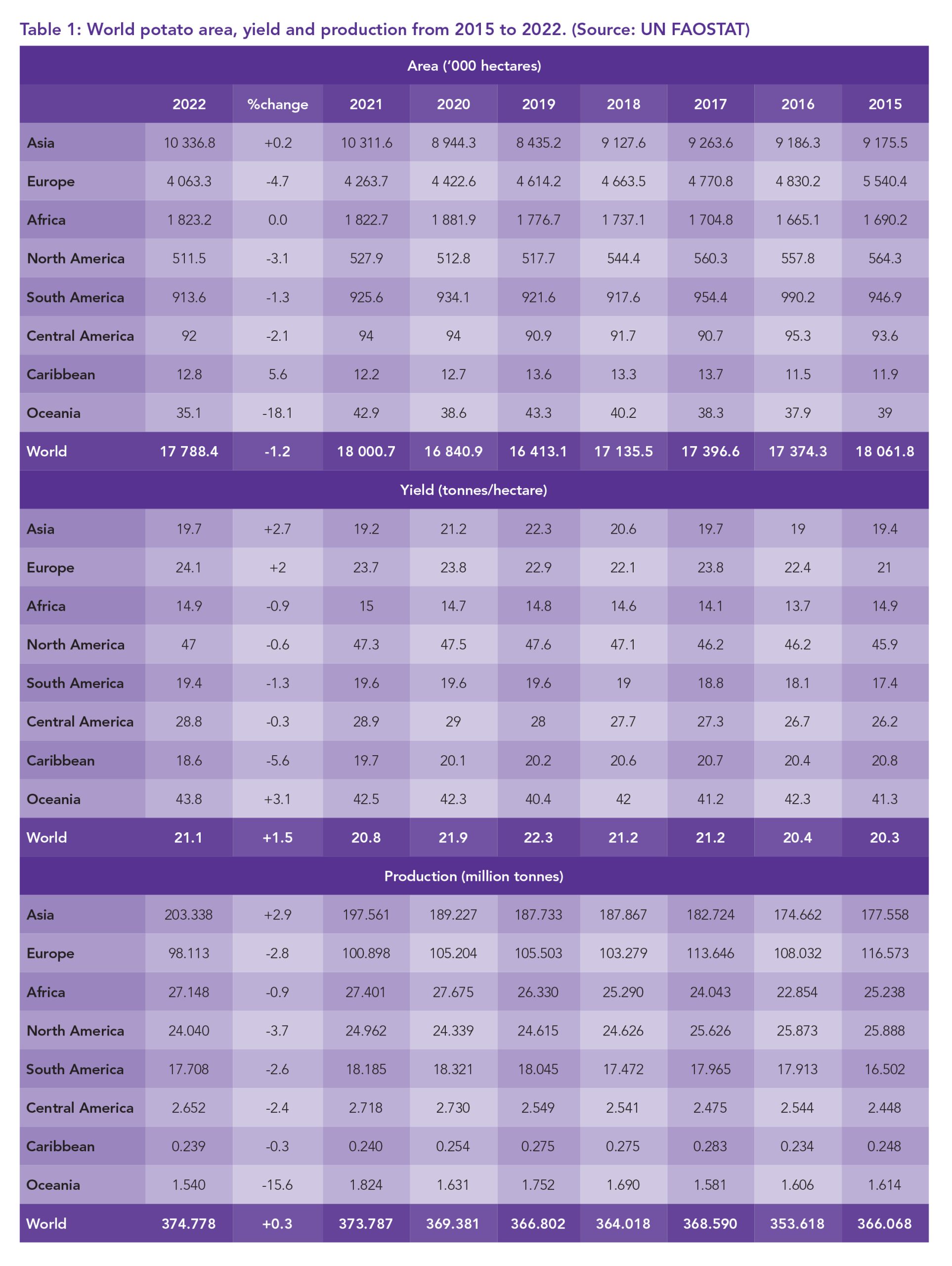

The potato industry has reached new heights in global production, with 2022 witnessing a record 374.8 million tonnes which represents a 0.3% increase from the previous year. This remarkable achievement, fuelled by higher yields compensating for reduced planting areas, sets the stage for continued growth and challenges in the potato market.

Preliminary data for 2023 indicates continued growth in Asia and Africa, with North America boasting a notable 10% increase in its harvest which should make up for a disappointing European harvest affected by excessive rain. However, potatoes diverge from other major crops (maize, wheat, rice, potatoes and soya), experiencing a decade-long decrease in planting, prompting concerns. The looming challenges for 2024 include uncertainties pertaining to weather and seed availability.

Recent trade figures reveal a shift favouring local suppliers in Asia rather than other countries exporting to it, as initially expected with the rise of Asia as the most important potato region. China, a major role-player, has increased shipments to destinations such as Japan, underscoring changing dynamics in the global potato market.

Achievements in 2022

At the end of every year, the United Nations’ Food and Agriculture Organization’s statistical division, Food and Agriculture Organization Statistics (UN FAOSTAT), publishes production figures for the previous year, which means Supply Intelligence (the publishers of World Potato Markets) obtained the 2022 figures.

Global potato production reached a new peak in 2022 at 374.8 million tonnes, 0.3% up on the 2021 figure, driven by a 3.5% overall growth in the decade between 2012 and 2022.

Asia contributed significantly, surpassing the 200 million tonne mark (up 2.9%), while every other region, including Europe, North America and Oceania, faced challenges with a dampened yield (2.8, 3.7 and 15.6%, respectively).

Planting and yield trends

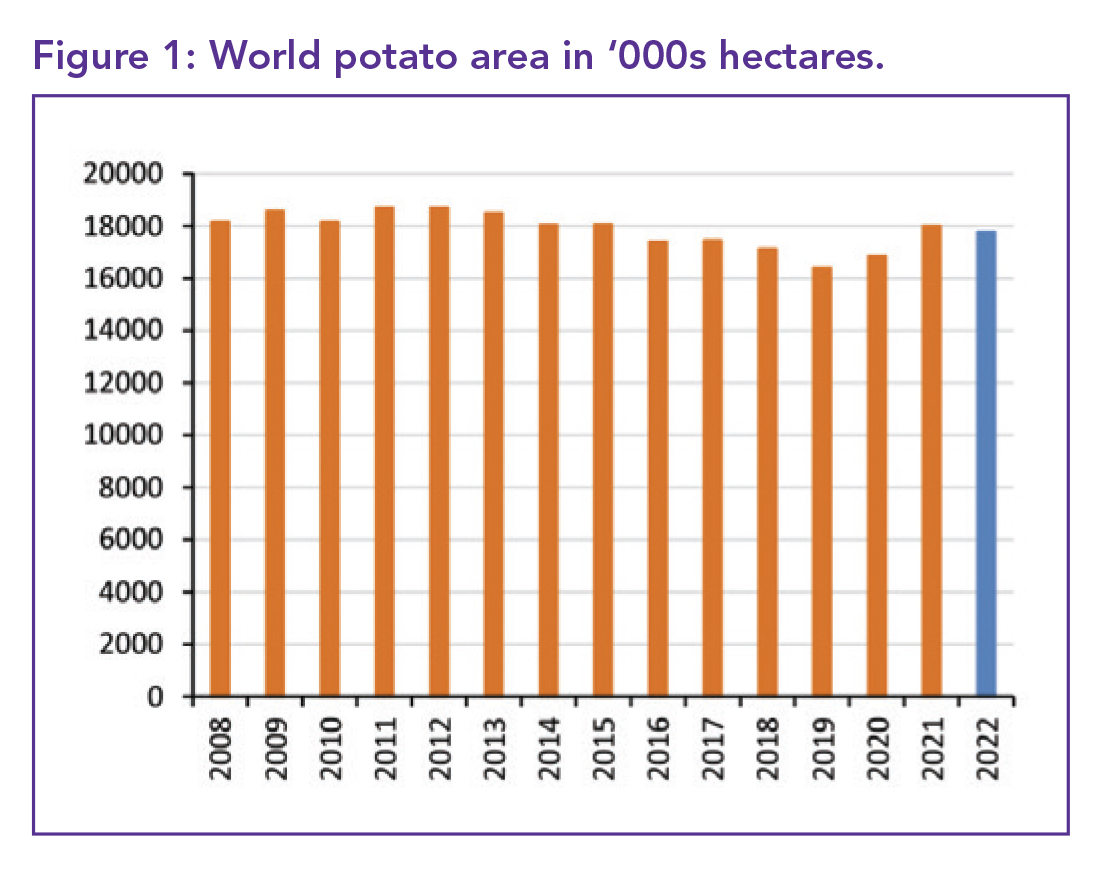

The global potato-growing area decreased slightly by 1.2% to 17.788 million ha but remained 3.5% higher than in 2012. Asia, Africa and the Caribbean saw an increase in their potato areas (although the African increase was tiny). Europe and Oceania saw significant declines in their areas.

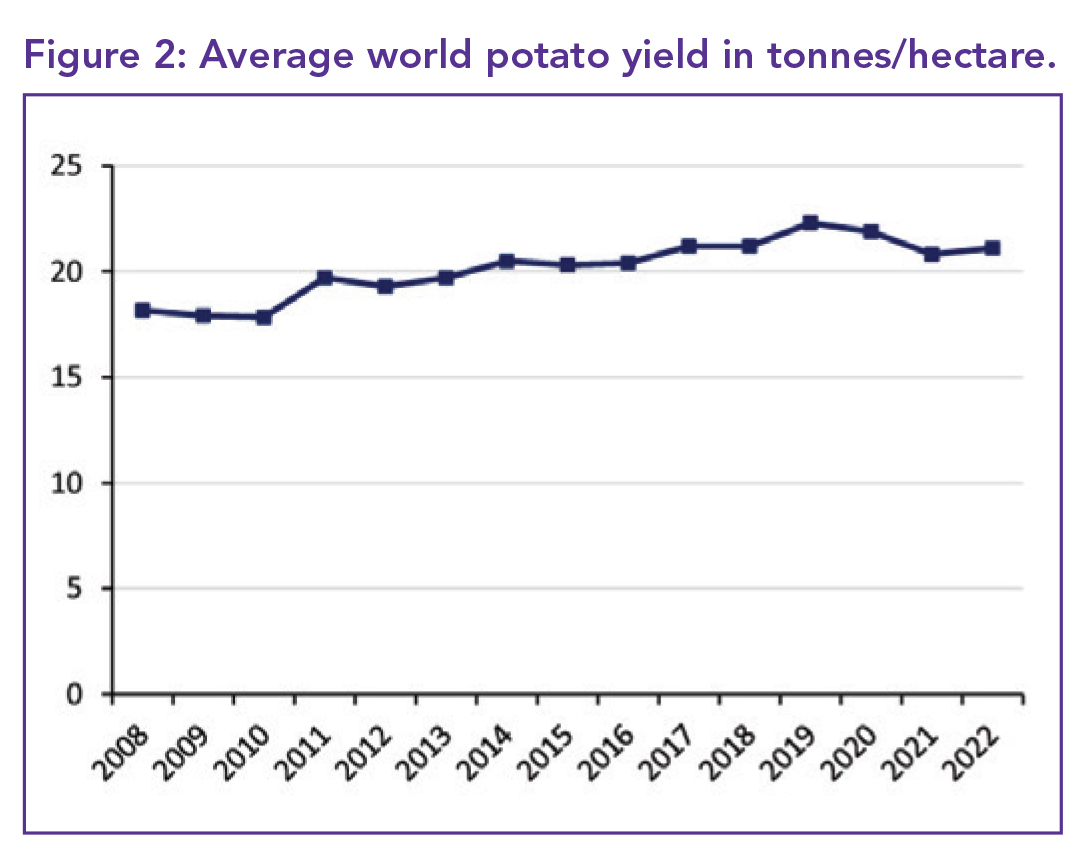

The world average yield rose by 1.5%, reaching 21.1 t/ha, an increase of 9.3% on the decade, but 5.4% below the all-time high of 22.3 t/ha in 2019, with Asia and Europe experiencing increases (2.7 and 2%, respectively).

In 2023, however, Asia experienced further increases in both yield and cultivated area, while the United States (US) crop saw a significant 8.9% boost and the Canadian crop increased by 3.7%. These gains are expected to offset the stagnant production in Europe. However, overall global production is forecast to reach between only 377 to 380 million tonnes, indicating a modest increase.

Potato growth lag

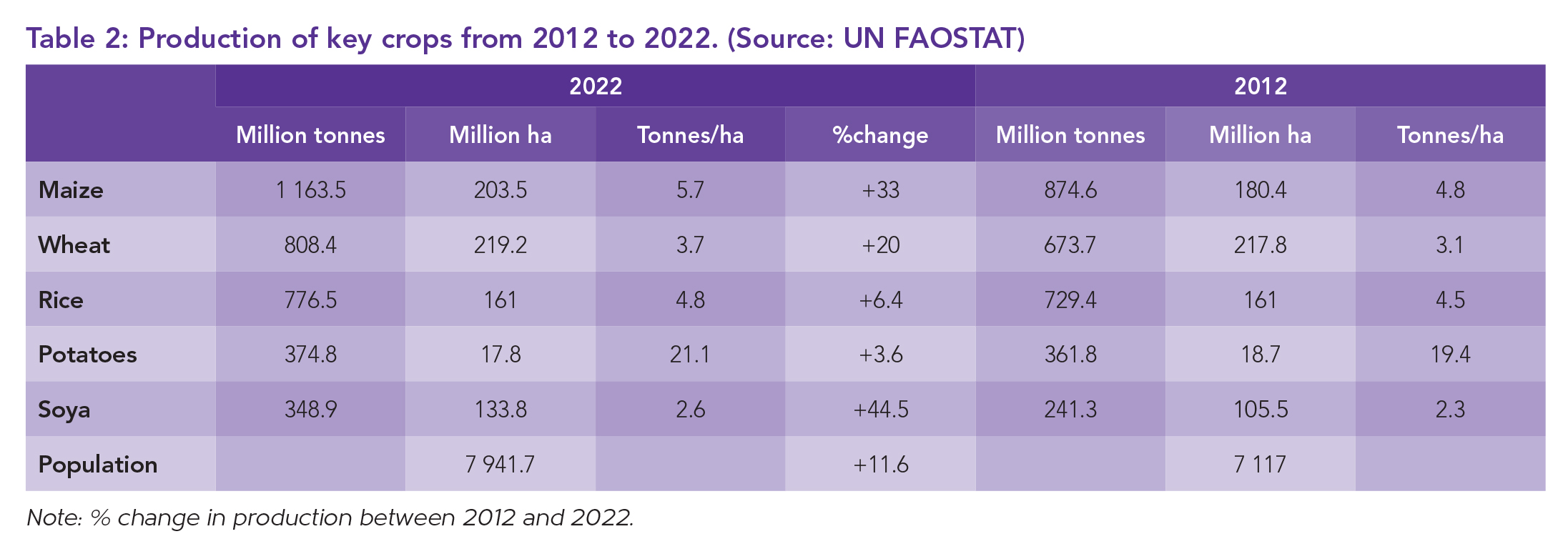

While potatoes maintain the highest yield among major crops, the decade leading up to 2022 saw potato production lag behind other crops such as soya (output jumped by 44.5%), maize (yields up by 17.9%), wheat (yields up by 19.2%), and rice (yields up by 6.4%).

Concerns arise as potatoes fail to match the growth in the world’s population (an 11.6% increase) over the same period. Rice production has also not kept pace with global population growth. Only soya beans and maize have significantly surpassed population growth.

Potatoes remain the highest-yielding crop among the five mentioned, with an average yield of 21.1 t/ha. However, rice showed the smallest increase in average yields over the past decade.

Global players

China and India, the top potato-growing nations, increased production in 2022 (95.631 million tonnes and 56.176 million tonnes, respectively). Noteworthy shifts in production were observed in various countries, highlighting the industry’s dynamic nature.

In 2023, several Asian countries witnessed significant increases in potato production, with Bangladesh reaching 10.145 million tonnes and Pakistan achieving a record crop of 7.937 million tonnes. Despite the war, Ukraine maintained its position as the third-largest producer, although output decreased by 2.1% to 20.899 million tonnes due to a 6.1% reduction in harvested area.

Russia, on the other hand, saw a 3.2% increase in production to 17.792 million tonnes. In contrast, the US experienced one of its smallest crops in recent years in 2022, with a 4.3% decline to 17.792 million tonnes compared to 2017.

Drought in Europe negatively affected yields across the continent, except for Denmark, which saw an increase. Over the past decade, 11 countries (Qatar, Senegal, Burundi, Niger, Guinea, Afghanistan, Turkmenistan, Nicaragua, Lebanon, and Mali) more than doubled their potato production, notably Pakistan.

However, production halved in 12 countries, including the United Arab Emirates, Iraq, Greece, Belize, Uruguay, Lithuania, Rwanda, Hungary, Malawi, Democratic People’s Republic of Korea, Latvia and Laos.

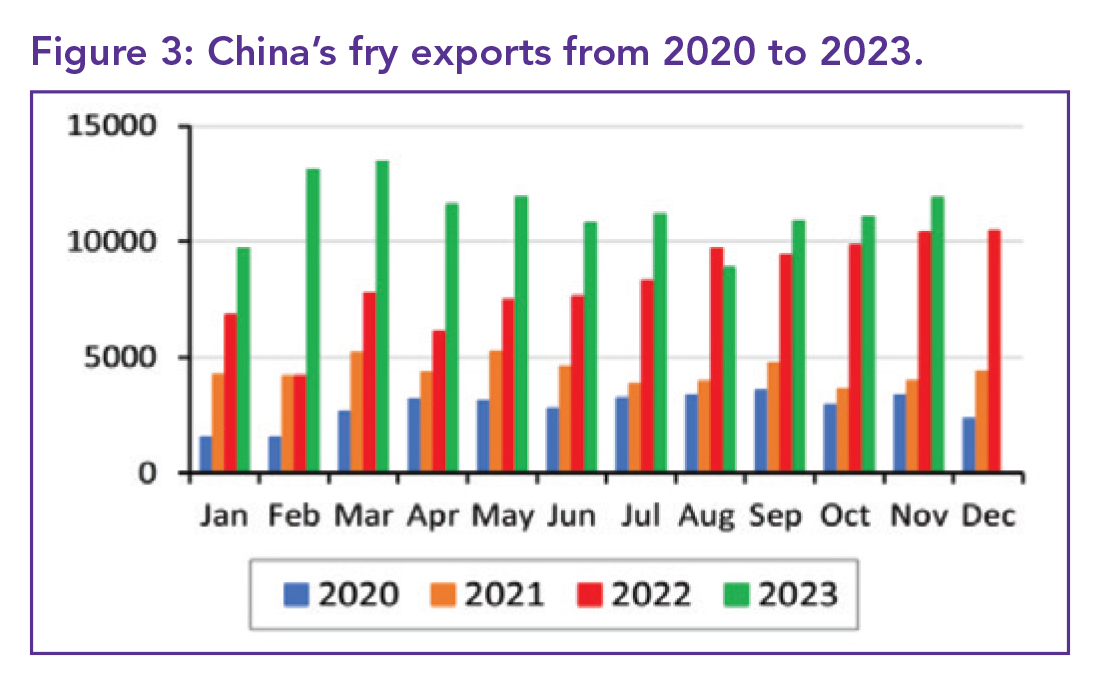

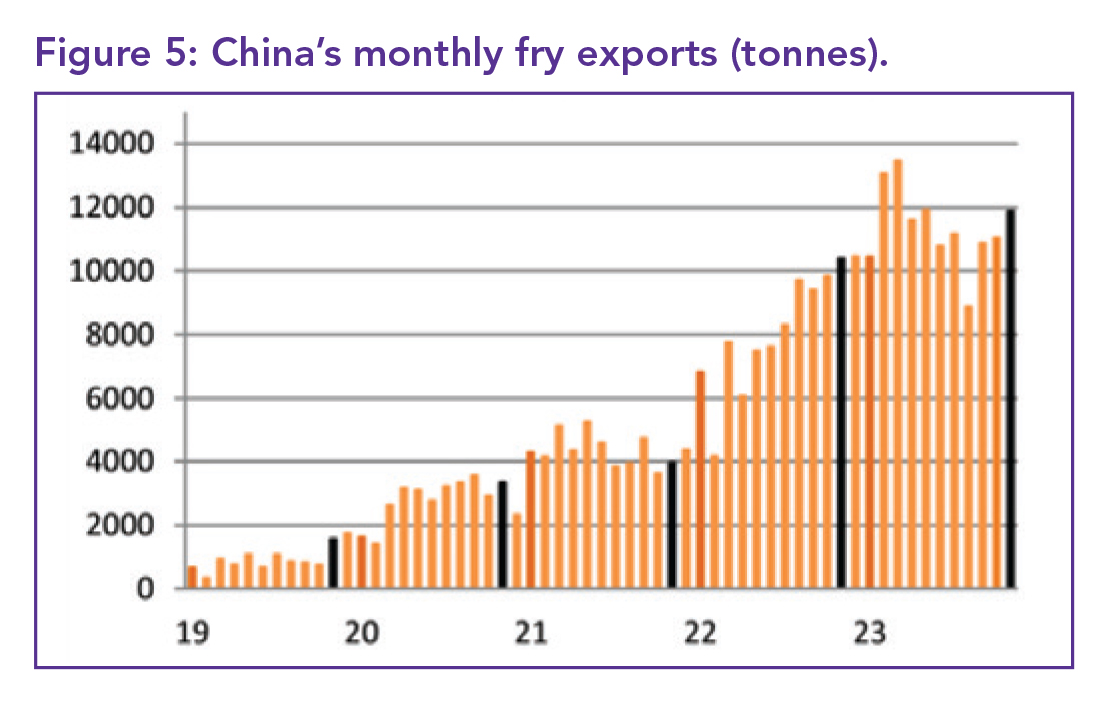

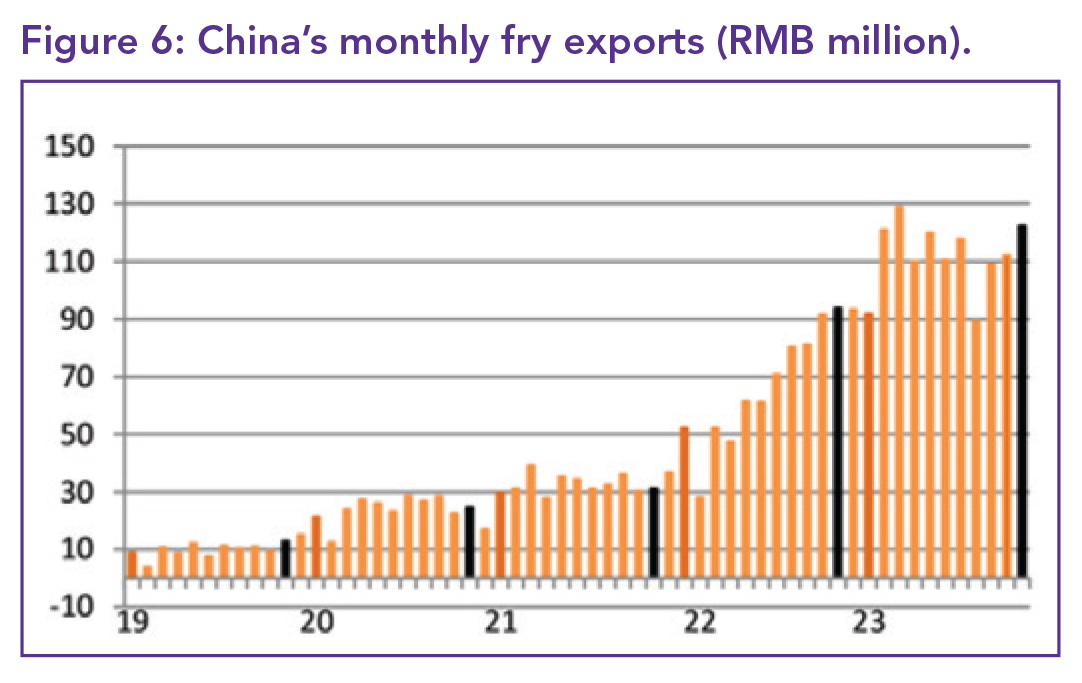

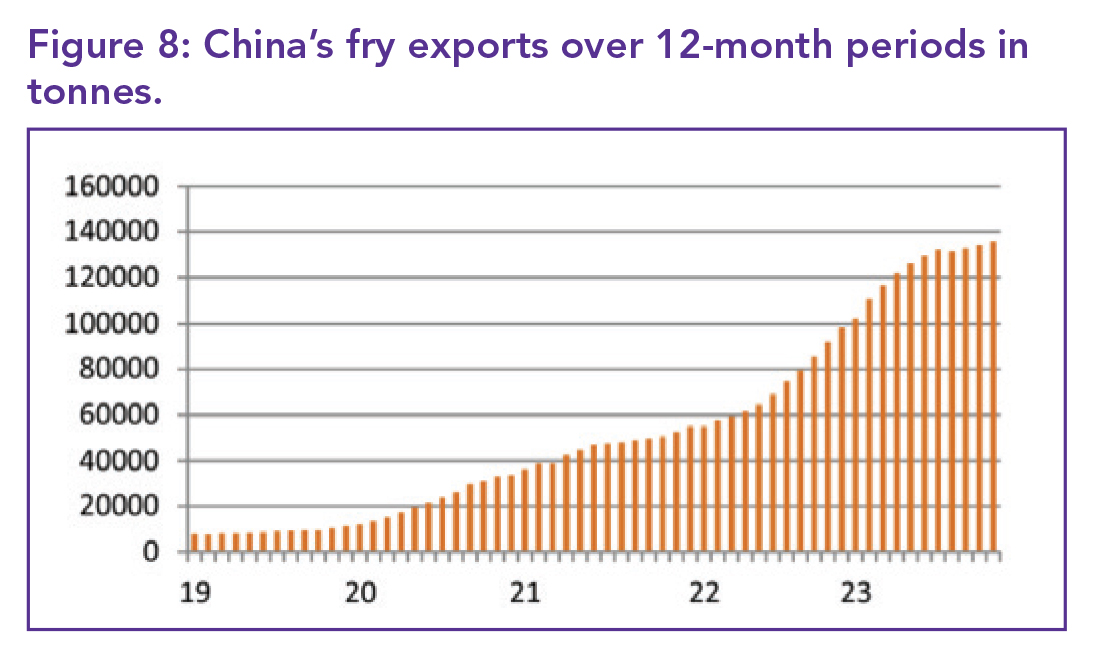

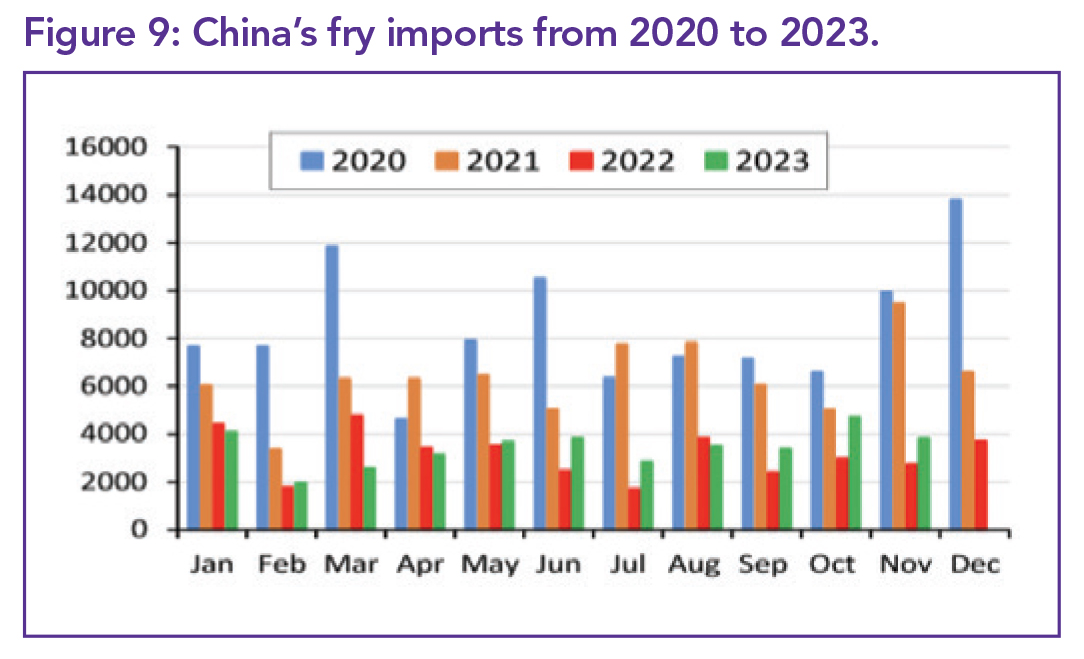

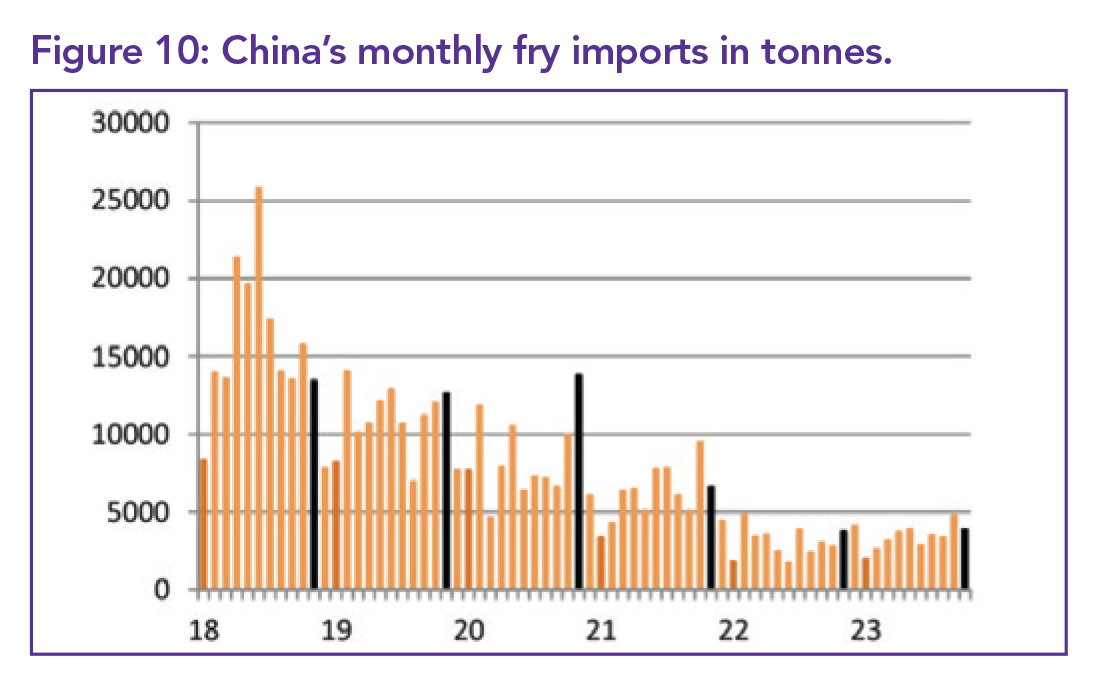

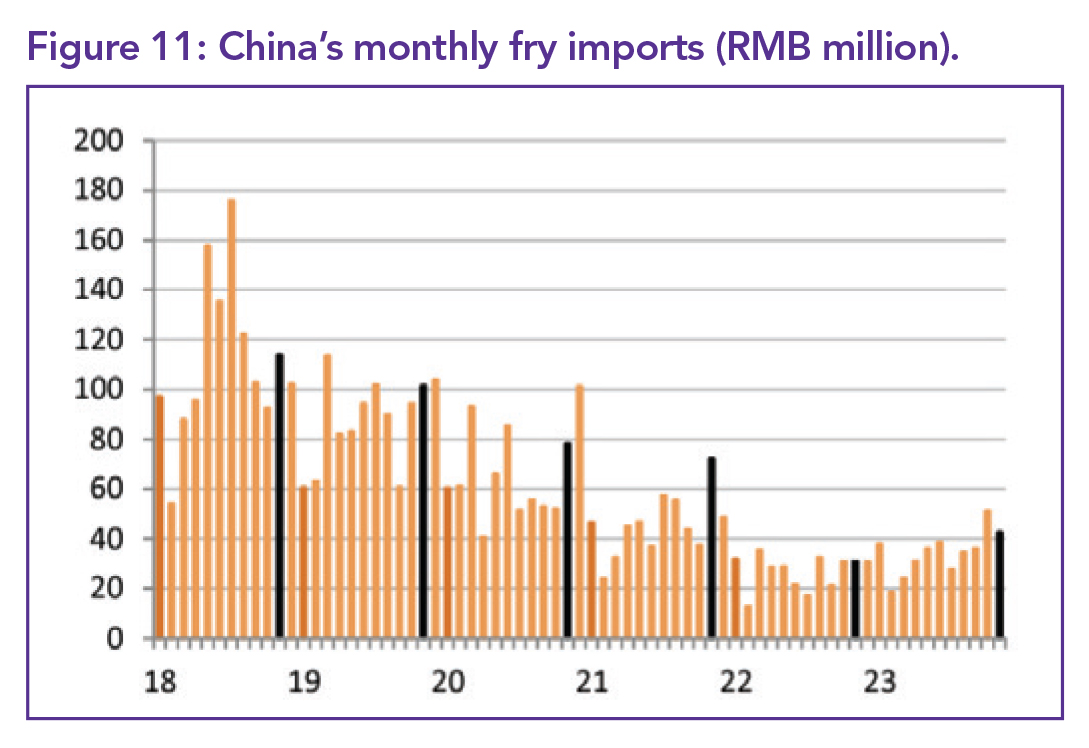

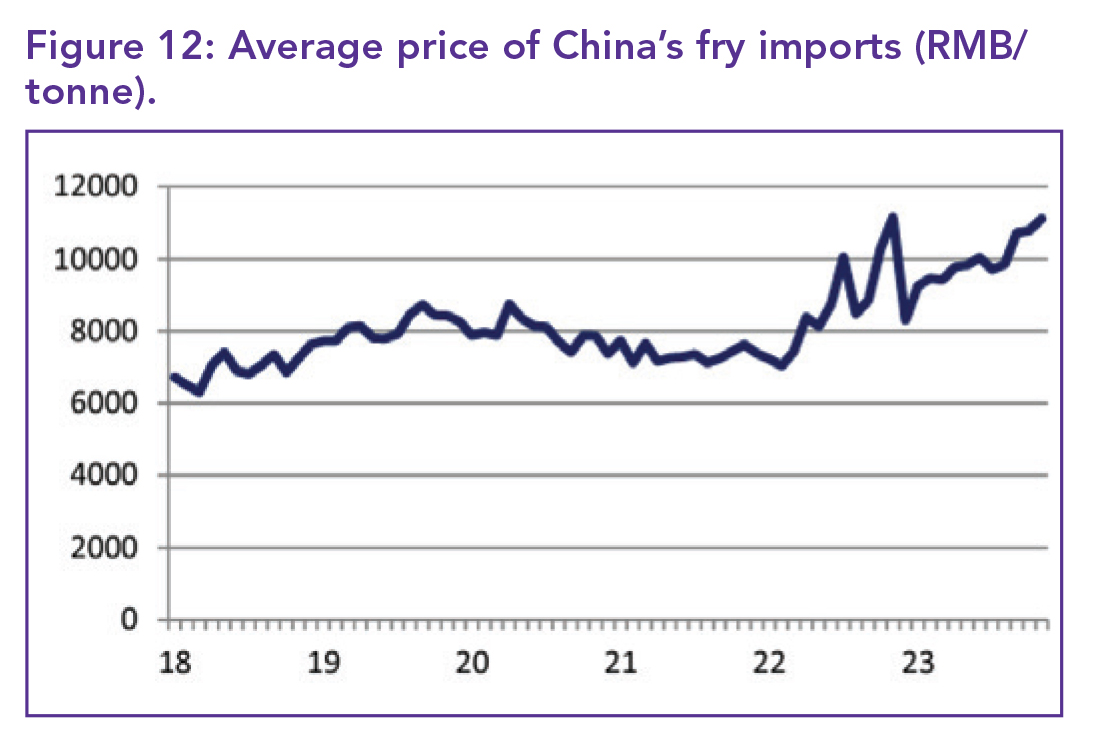

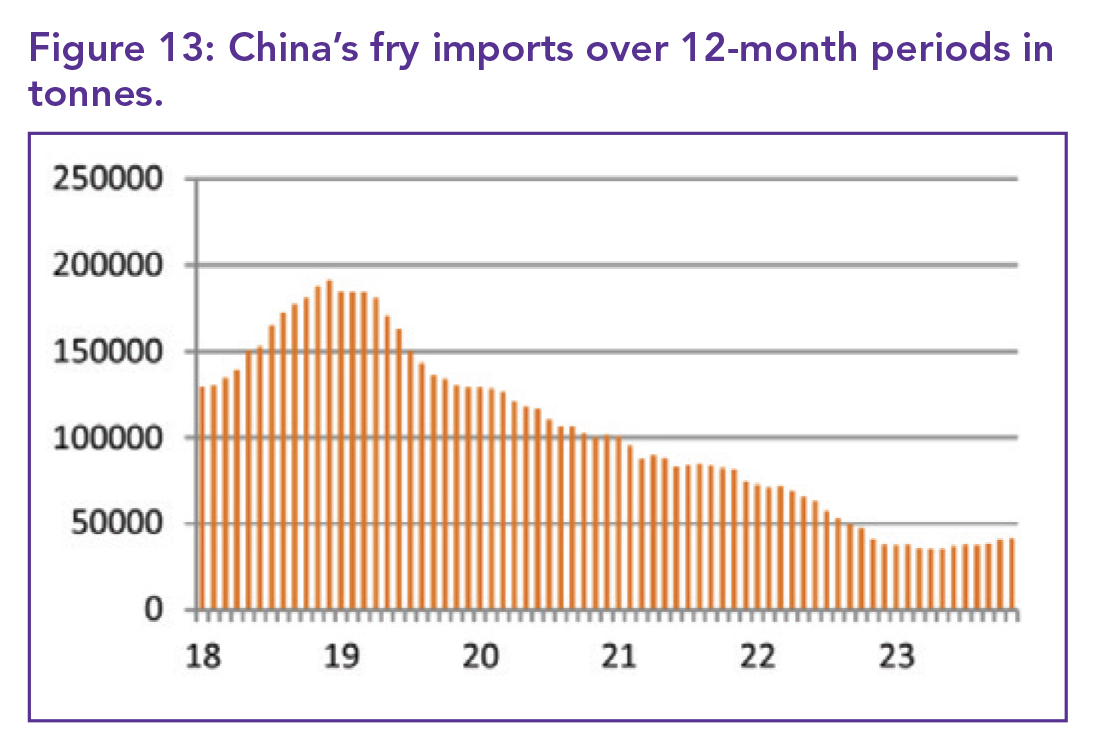

Japan boosts China sales

China’s fry exports witnessed a surge in November, reaching their second-highest monthly earnings at Renminbi (RMB) 122.337 million. Japan emerged as the largest customer, contributing to higher prices and boosting China’s earnings.

Market dynamics

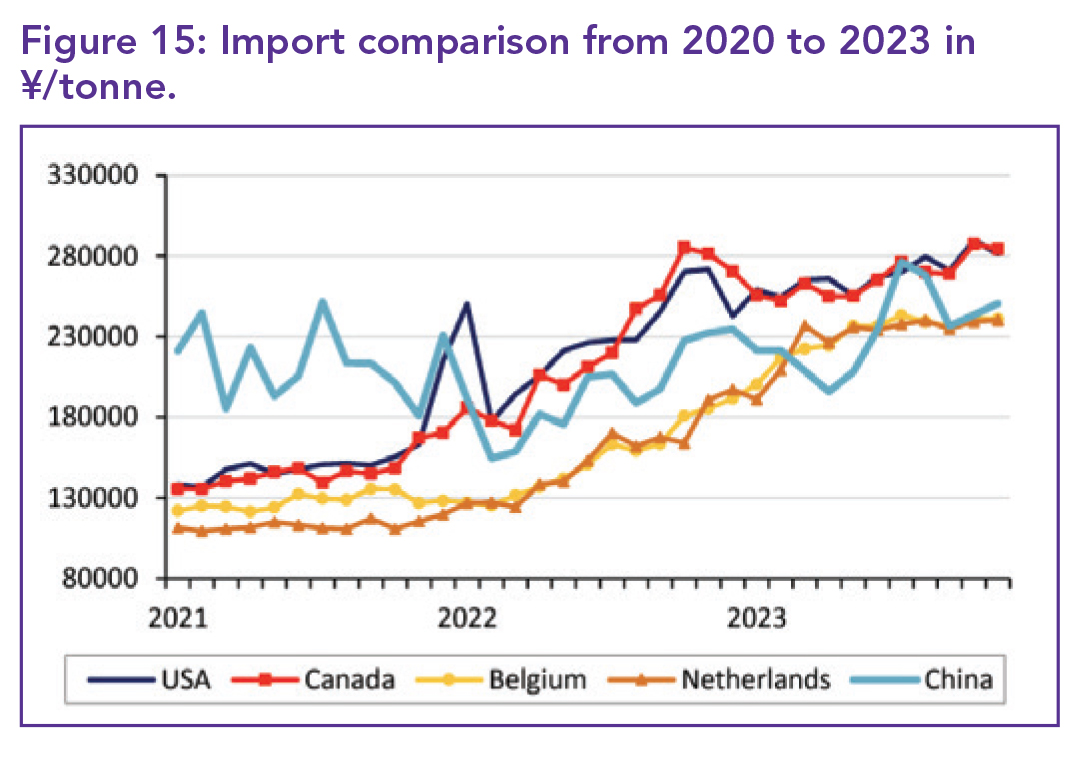

In November, exports of US fries to China experienced a significant decline, reaching just 950 tonnes, marking the worst month since February. Despite this, there was a notable improvement of 38.7% compared to the same period last year. Total imports for the year have slightly increased by 1.5% to 41 433 tonnes, although still significantly lower than in 2020/21.

Turkey emerged as a beneficiary, with its fry exports to China increasing by 79.7% compared to the previous year, reaching 2 536 tonnes for November and 10 805 tonnes for the year, reflecting a rise of 63.9%. Despite being more expensive than US fries, Turkey’s sales were robust. Belgian fries, although cheaper, experienced a price increase of 19.8% over the past year, selling 336 tonnes in November, which was half its October sales. However, annual sales for Belgium still increased by 69%.

France also made an appearance in the market with 16 tonnes of processed product at a higher price point, reflecting the top end of the market.

China’s strategic export moves included sales to the Philippines, Indonesia, Malaysia, South Korea, Thailand and Bahrain, showcasing the versatility and growth potential of the Chinese fry market.

Regional impact

China’s fresh potato exports experienced a 16.7% decline, totalling 41 146 tonnes. Despite lower orders from Vietnam and Malaysia, increased orders from Thailand and Singapore, along with a higher average export price, maintained market stability.

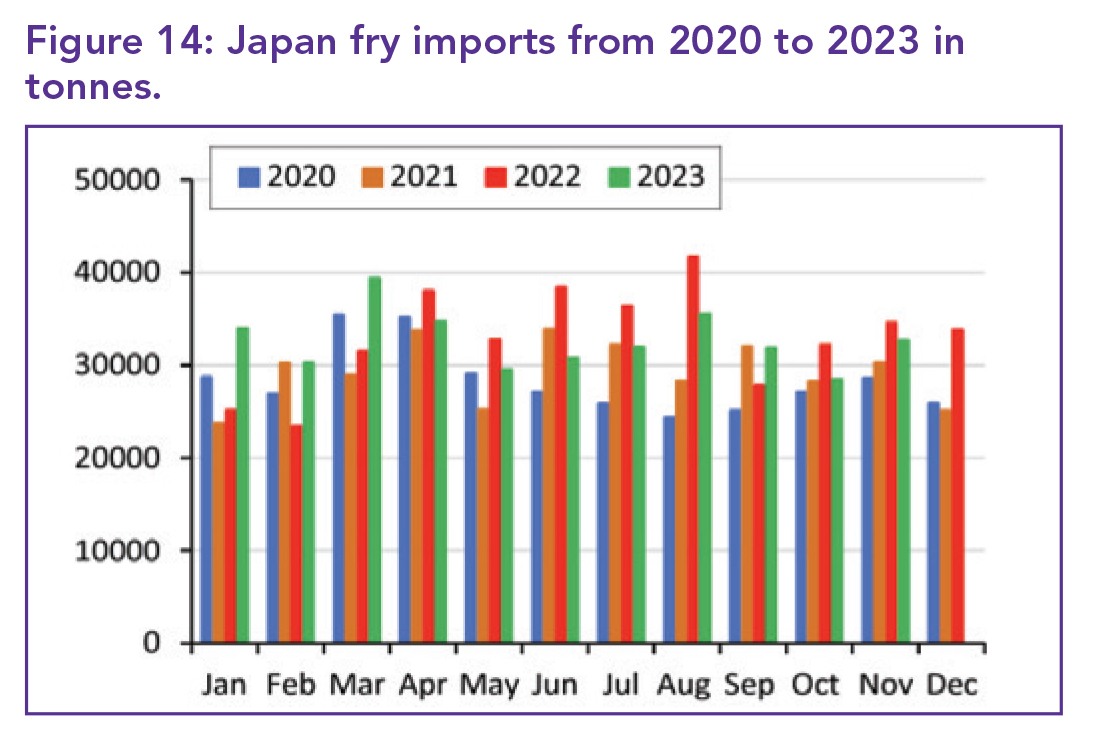

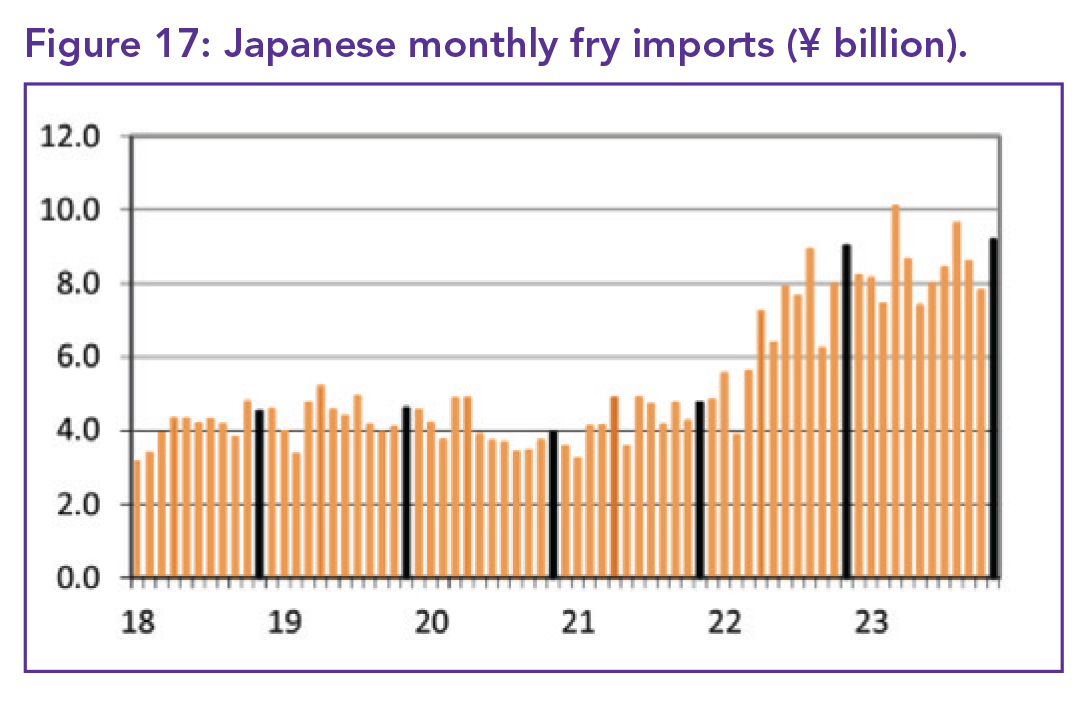

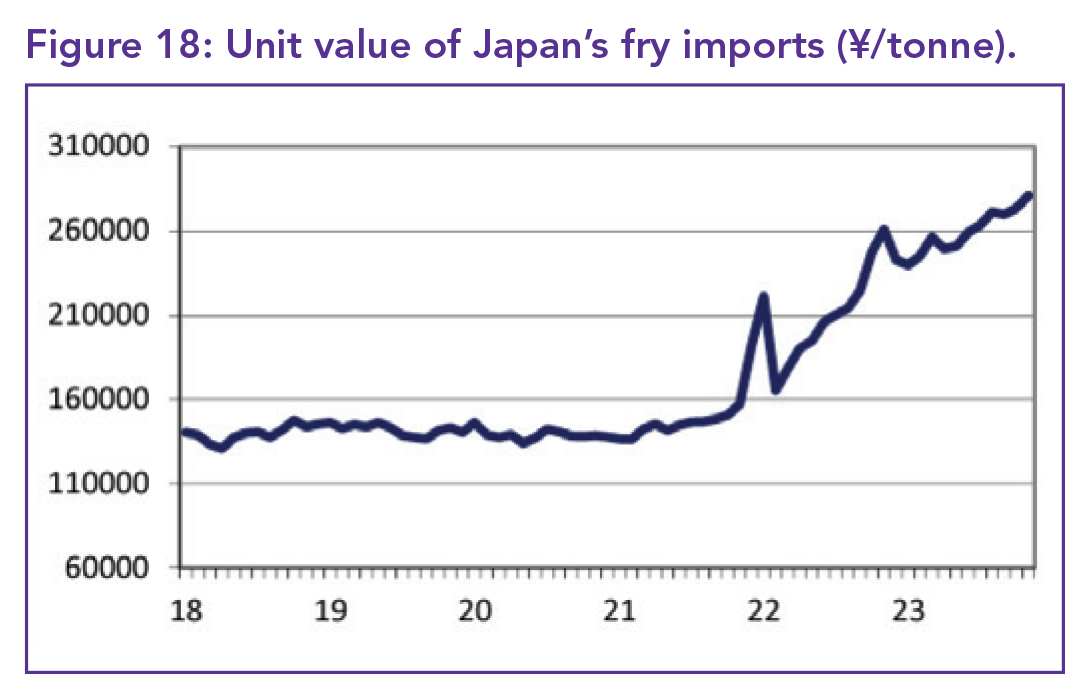

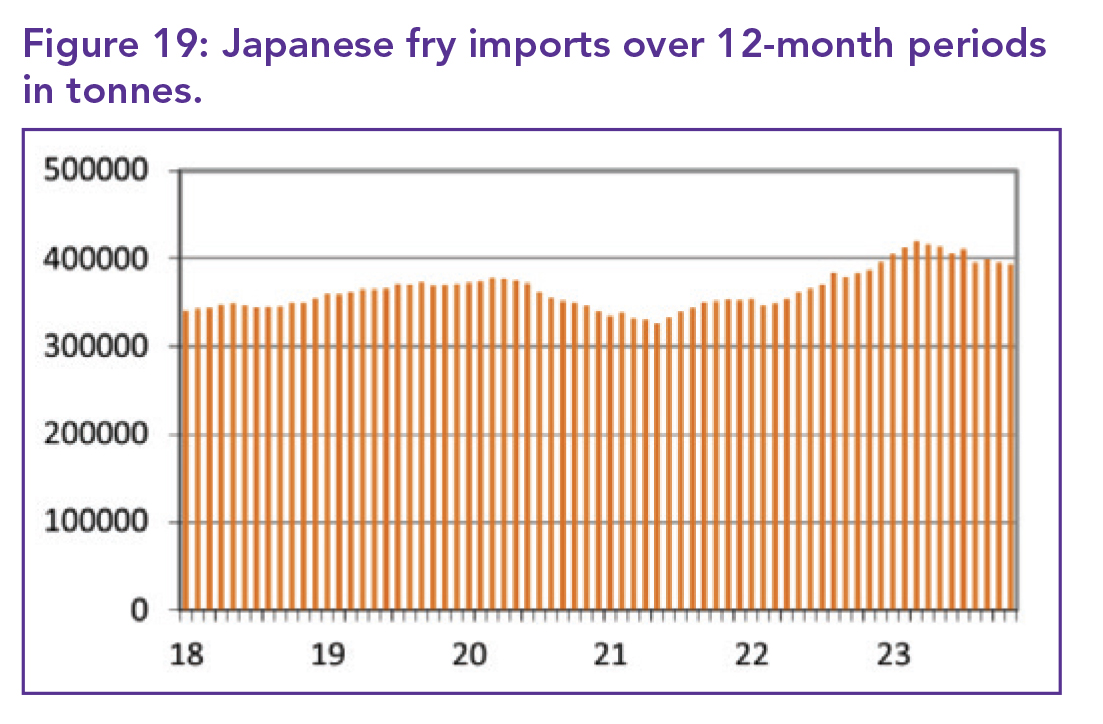

Japan: Rising prices, lower sales

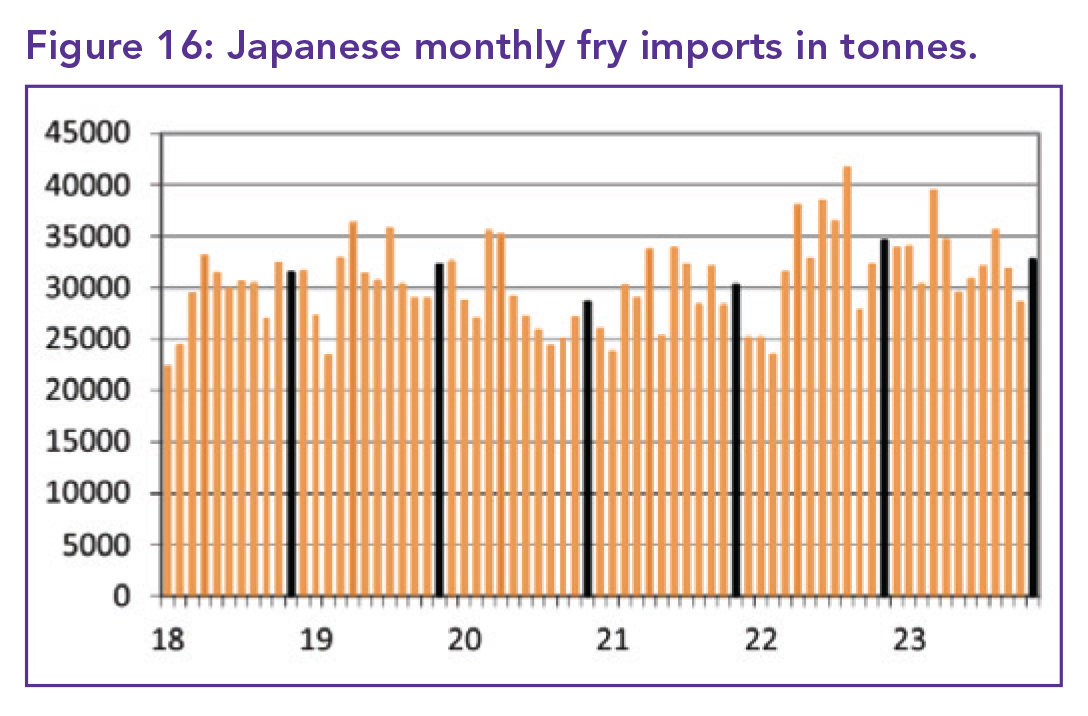

Higher import prices in November last year led to a decline in Japanese fry sales, totalling 32 726 tonnes.

This marks the second consecutive month below 2022 levels. US fries faced a significant 24.2% decrease in fry sales, while Dutch importers emerged as winners with increased sales.

The average import price rose to ¥281 039/tonne, a 7.7% increase from the previous year. US and Canadian fries’ prices surged, impacting overall sales and contributing to market dynamics.

Global competitors

Dutch and Belgian fries experienced sales variations, with Dutch fries achieving significant growth (4 539 tonnes), and Belgian fries facing declines despite higher prices (3 140 tonnes). Chinese fries, with increasing sales (2 718 tonnes, almost 800 tonnes higher) and prices, showcased a competitive edge.

Other players are keenly eyeing the opportunities in Japan’s price-sensitive market. India capitalised on this by selling 195 tonnes, bringing their yearly sales to 1.202 tonnes.

Argentina also entered the market with 173 tonnes, in addition to 86 tonnes imported in October. However, Argentina’s price of ¥327 336/tonne (US$2 295/t; €2 098/t) was not competitive, being ¥31 000 higher than US fries.

The annual cost of Japan’s fry import market has surpassed ¥100 billion, reaching ¥101.694 billion (US$713 million; €652 million). December is a significant month for fry consumption in Japan due to its seasonal celebration of Christmas, making it a crucial test of the import market’s sensitivity.

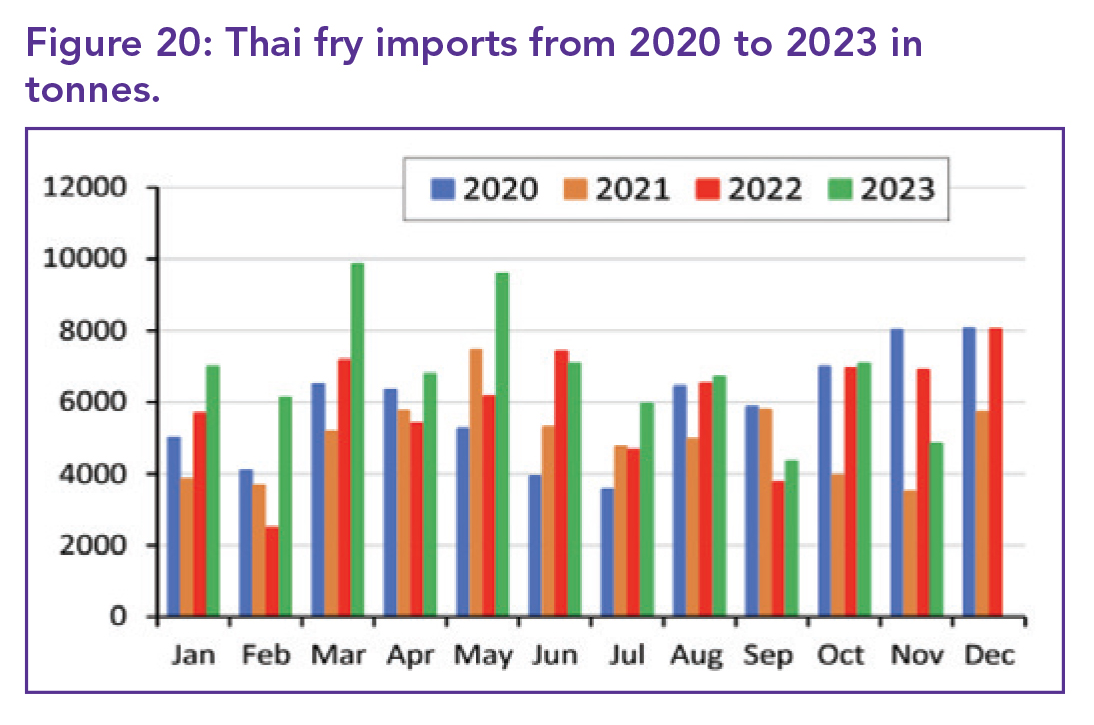

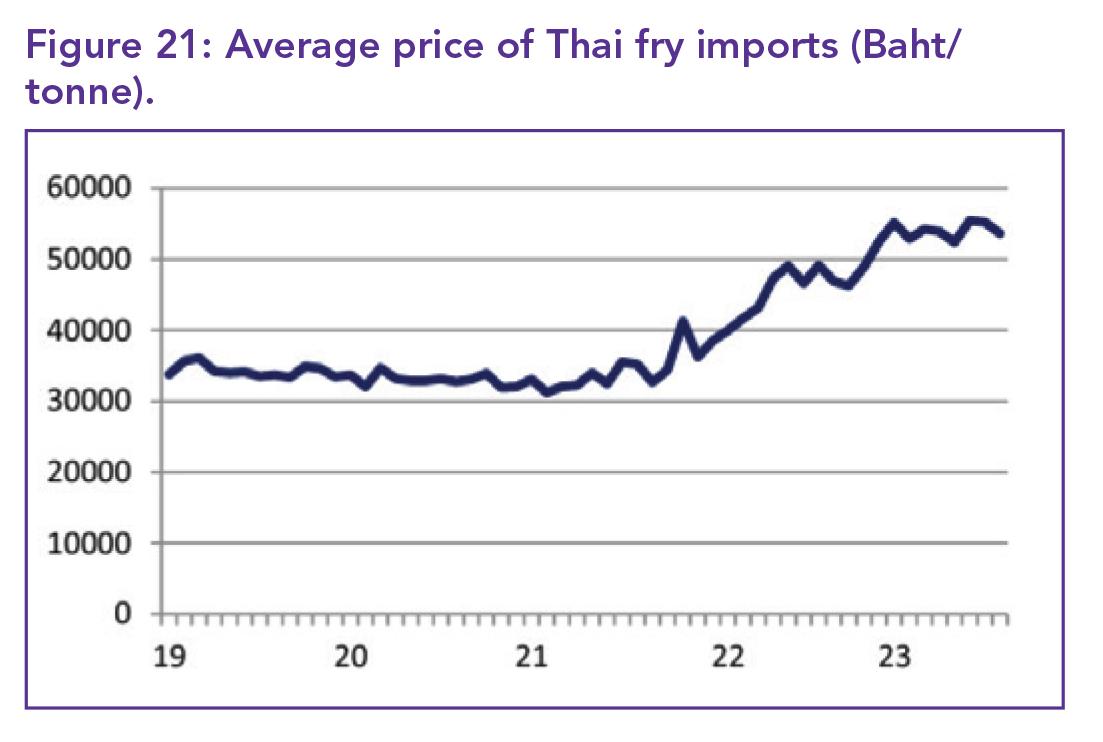

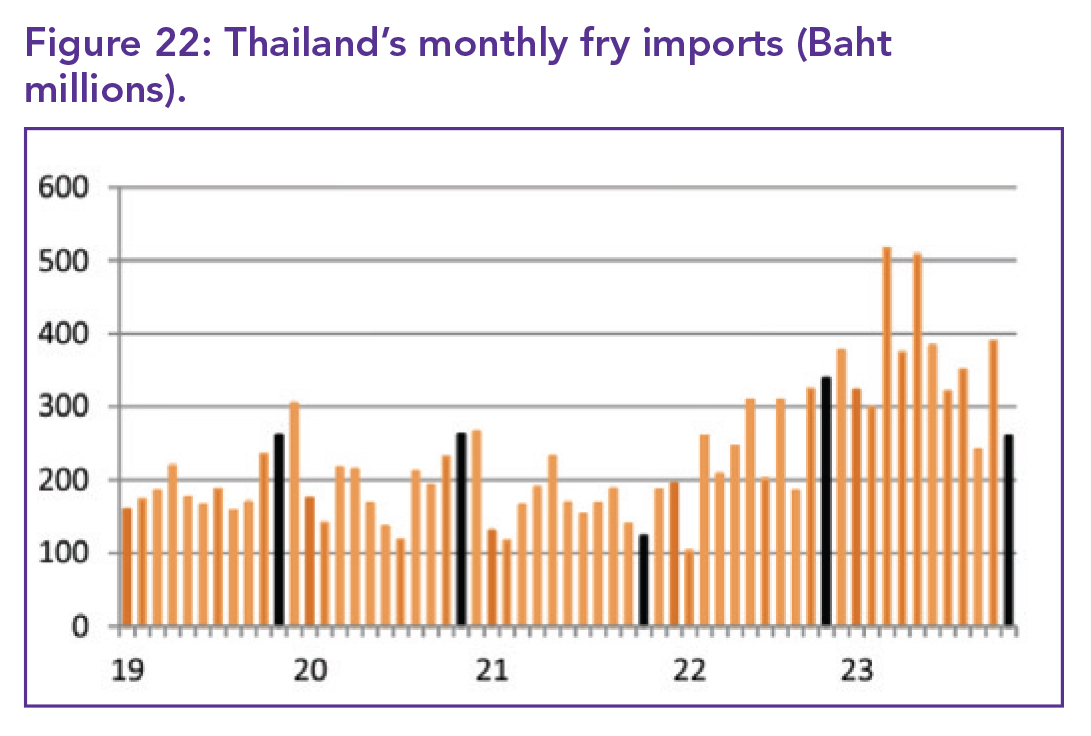

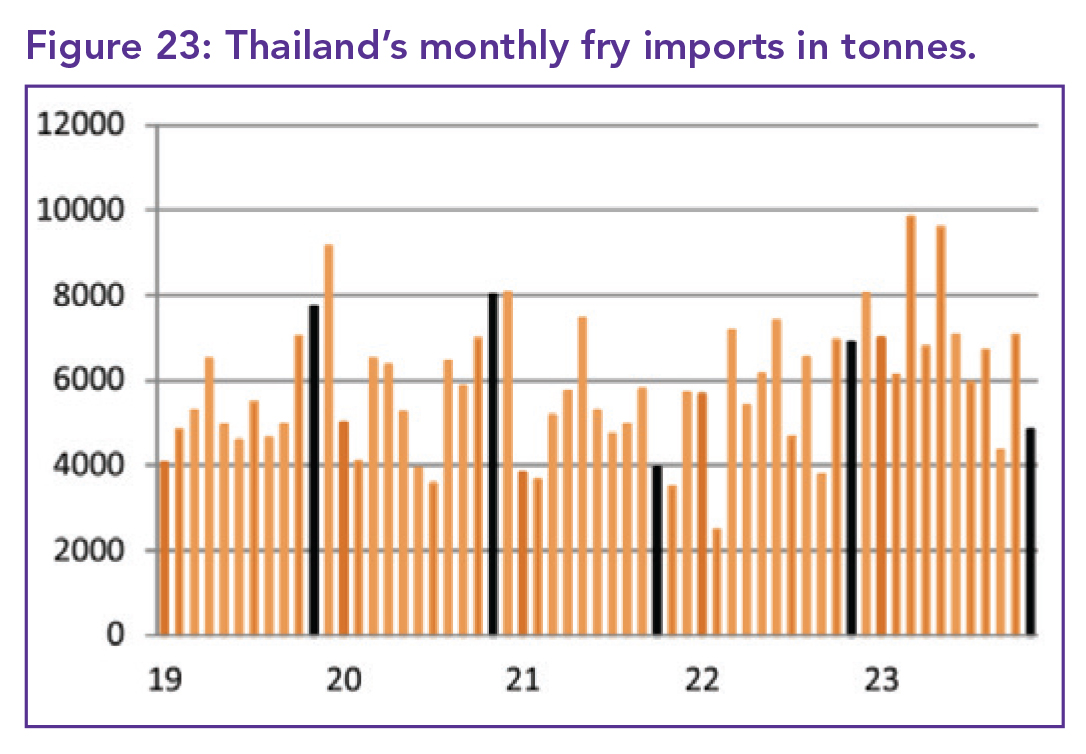

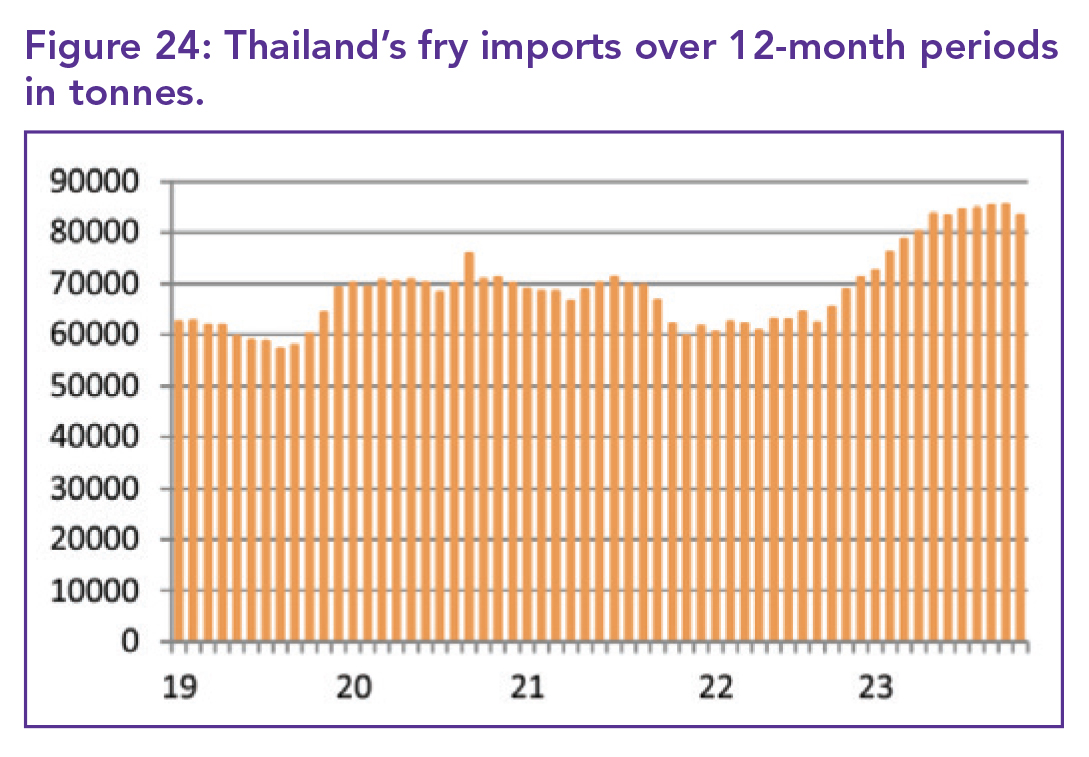

Thailand: Economic uncertainty

In November, potato fry imports into Thailand declined by 2 225 to 4 843 tonnes, indicating economic uncertainty. The hospitality industry’s readiness for the tourist season faced challenges amid ongoing economic shifts.

November’s imports experienced a significant decrease of 29.8% compared to the previous year.

Excluding the Covid-affected tourist season of 2021, this marks the lowest November imports since 2018. In 2019, Thailand welcomed over 39 million tourists, whose spending contributed to 12% of the country’s gross domestic product. Although 2023 saw an estimated 27 million visitors, predictions for 2024 suggest an increase in tourist numbers to between 35 and 40 million.

With Thailand welcoming fewer tourists in recent years, predictions for 2024 suggest potential growth, presenting both challenges and opportunities for the potato market.

Chinese tourists, crucial for the Thai market, are impacted by China’s slow economic growth.

To encourage more Chinese tourists, Thailand’s new prime minister has implemented measures such as permanent visa-free entry and increased security.

Cut back on fry imports

Major fry imports into the country saw a decrease in volume recently. India sold 2 002 tonnes, down by 954 tonnes from October and 14.6% lower than last year, despite a lower price. China reduced its price further and sold 952 tonnes, which is 33.8% less than in 2022.

Dutch fry sales fell by 540 to 1 016 tonnes, 36.7% lower than last year, at a higher price compared to the previous year. New Zealand and the US also experienced a drop in sales, with the US selling just 208 tonnes, 67.3% less than a year ago. Despite the decline in imports, annual sales figures remain higher than in previous years, with Chinese fries showing the most growth. Higher prices have led to an increase in the Thai fry import market, which is now worth Baht 4.349 billion, up 51.5% since a year ago. – Anjé Erasmus, Potatoes SA

For more information and references, email anje@potatoes.co.za or visit www.potatoes.co.za.