Estimated reading time: 6 minutes

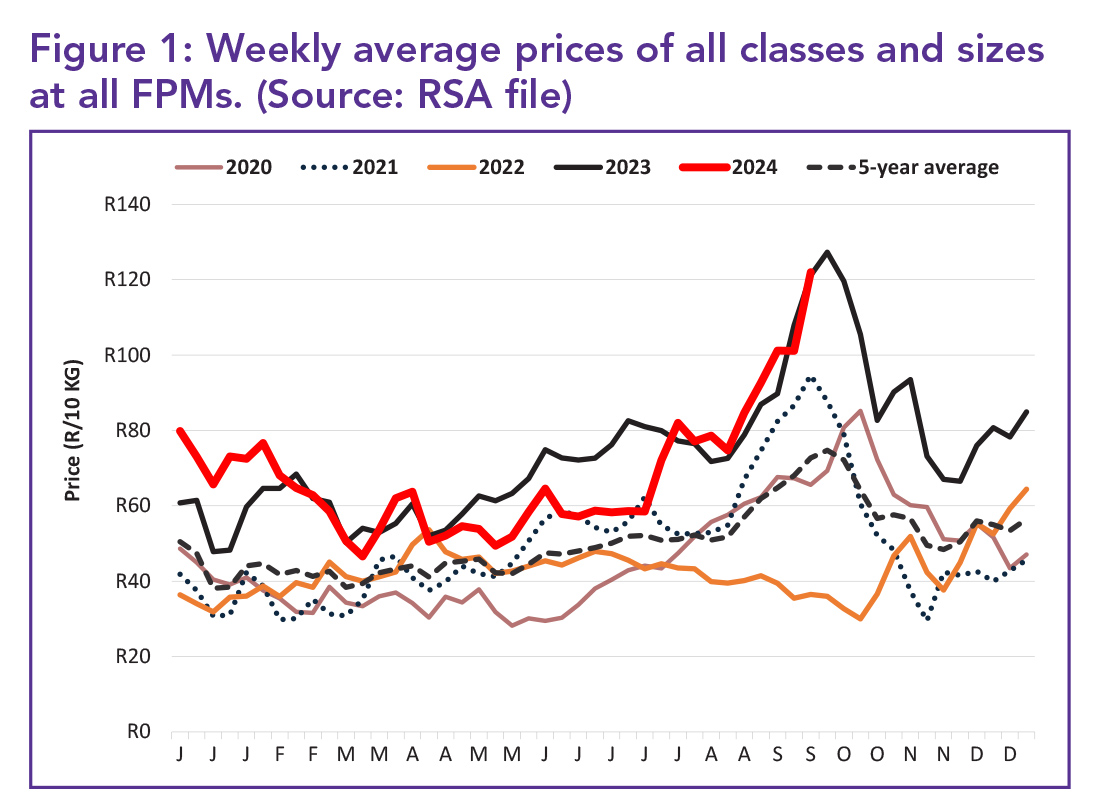

The average weekly price of potatoes in the first 39 weeks of 2024 reflected an upward trend, similar to the first 39 weeks of 2023, with the average weekly price of week 39 at 21% higher than week 38. Figure 1 indicates the weekly average price at all markets for all classes and sizes.

The average weekly price in week 39 was R121.99 per 10 kg bag, R0.83 higher than in week 39 of 2023. The upward trend in the average weekly price in 2024 has mainly been due to the steep increases observed from weeks 29 to 39. The steep price increase in week 39 was primarily due to low volumes of fresh produce received at the fresh produce markets (FPMs) during that week. Deliveries from the Limpopo region in particular were much less (43% less than the five-year average) due to the impact of frost damage in the region.

Lower stock levels

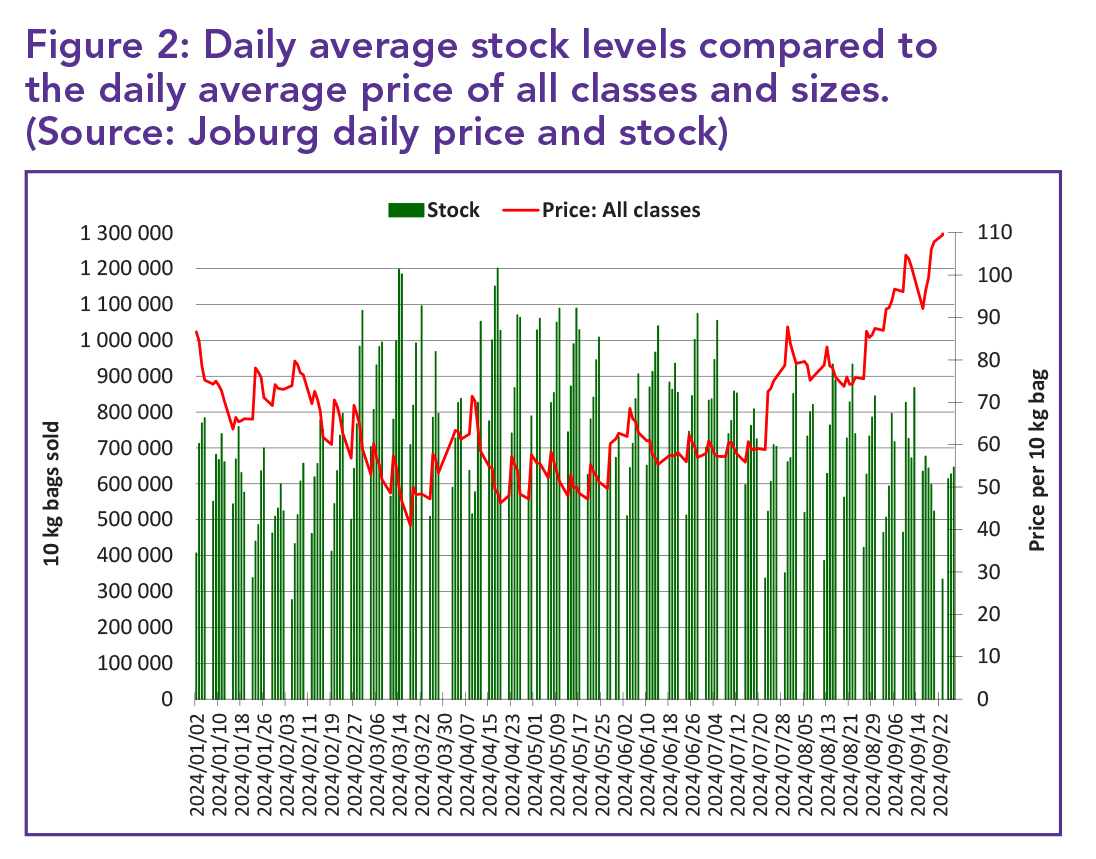

Figure 2 reflects the daily average stock levels and daily average price. It clearly indicates that stock levels decreased to a large extent compared to July and August 2024, and confirms the daily prices received during week 39. In order for daily prices to be sustained, producers should ensure stable delivery patterns (especially in times of higher demand) and good quality products to the FPMs at all times.

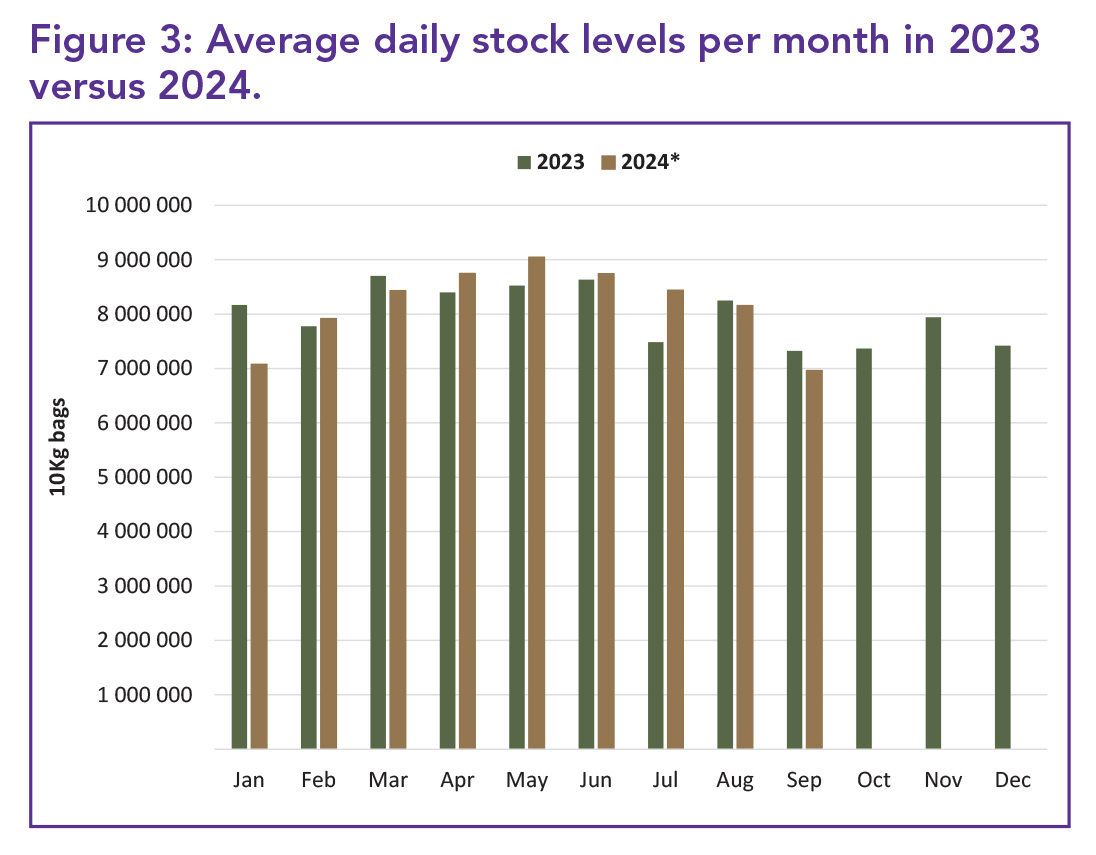

Figure 3 indicates the average stock levels in each month as opposed to levels during the same month a year ago. August and September 2024 reflect a decrease in 10 kg bags of 90 333 and 358 716 respectively, compared to August and September 2023. A comparison of sales in August 2024 to that of September this year shows that 15% fewer bags were sold in September 2024.

Weekly and monthly sales

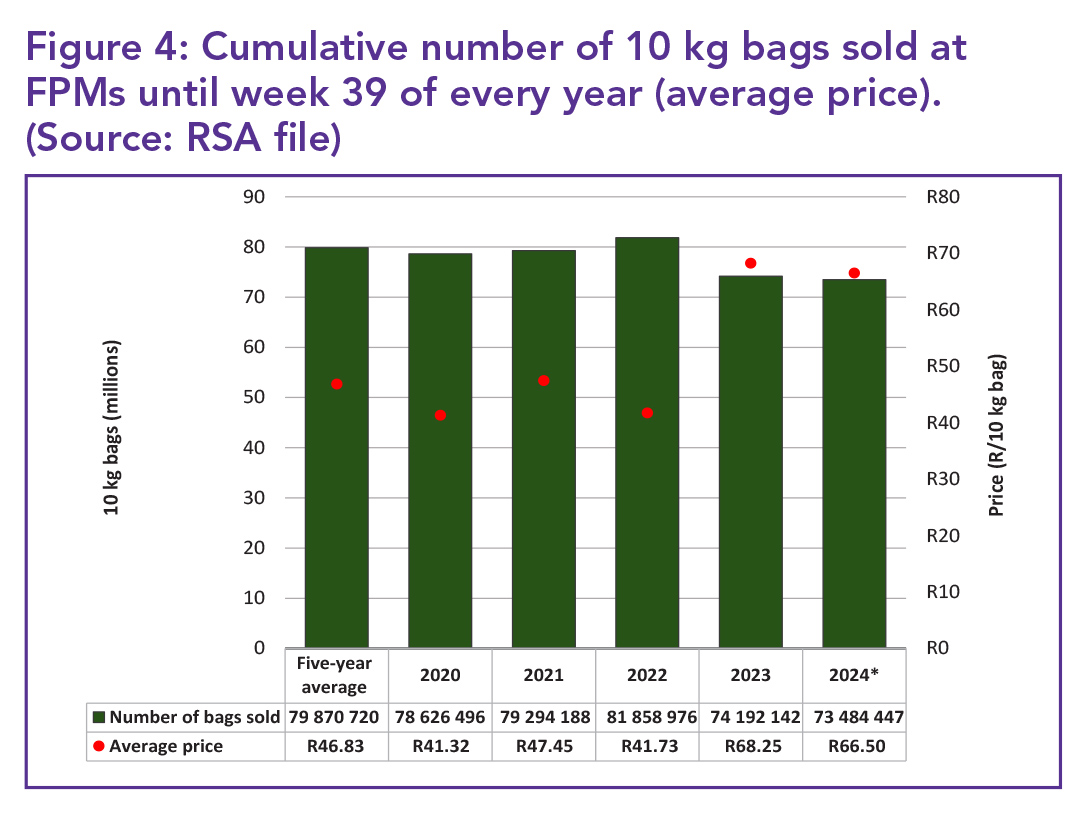

According to Figure 4, sales at the FPMs during the first 39 weeks of 2024 decreased by 1% (approximately 707 695 10 kg bags) since 2023’s corresponding figure. Sales in the first 39 weeks of this year exceeded the 73.4 million 10 kg bag mark. However, 6.39 million 10 kg fewer bags were sold than the five-year average of the same period. The average price for the first 39 weeks is also depicted in Figure 4, with 2024’s average price R19.67 higher compared to the five-year average price.

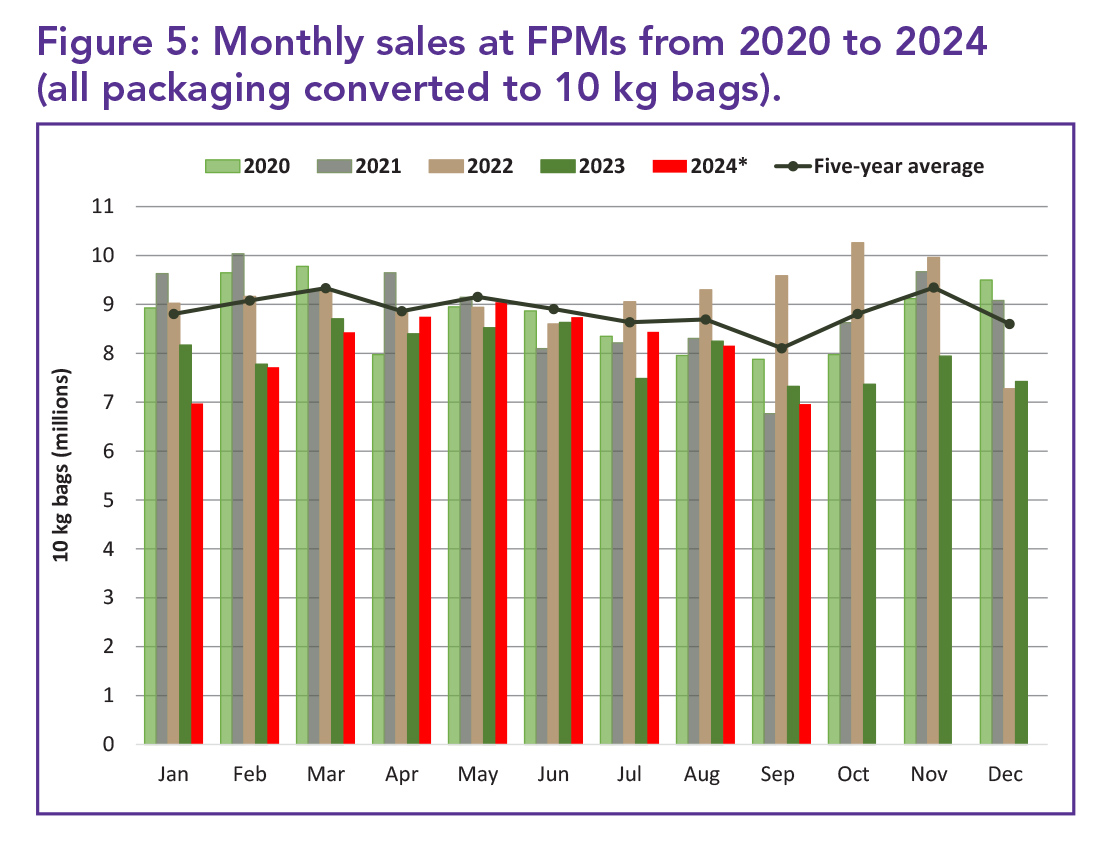

Figure 5 illustrates monthly sales at FPMs since 2020. In August, sales decreased to 8.15 million 10 kg bags, compared to July’s sales of 8.43 million 10 kg bags. In September, sales further decreased to only 6.96 million 10 kg bags, representing a decrease of 15% compared to sales in August this year and 5% in comparison to September 2023.

Top bag sales

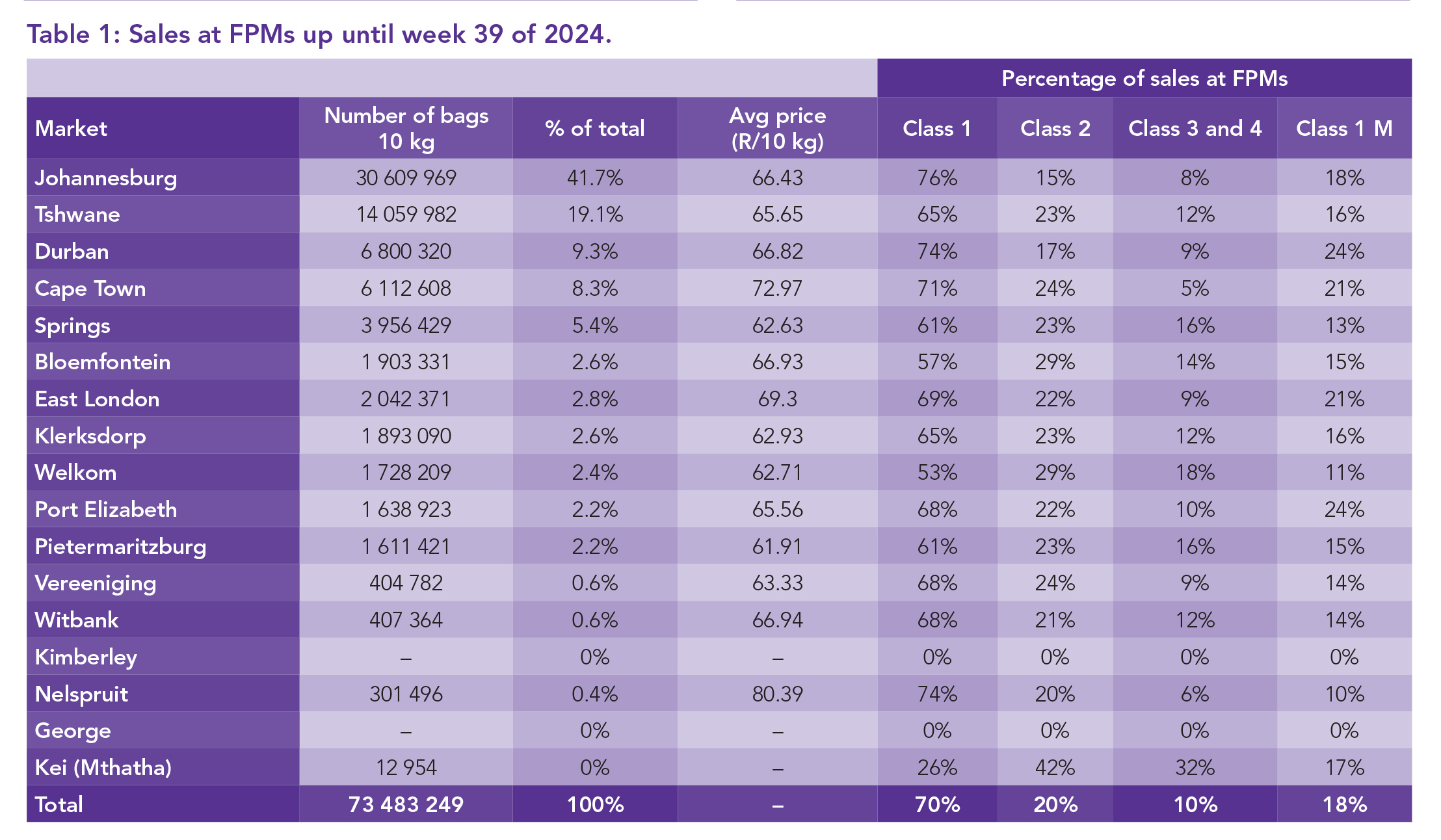

Table 1 contains the number of bags sold at the various FPMs during the first 39 weeks of 2024. The five biggest markets during this period were collectively responsible for 83.7% of the country’s sales. The average price (all classes and sizes) for each market also appears in Table 1.

In terms of the top average price per 10 kg bag received at the markets during the first 39 weeks, Nelspruit Market was in the first place with R80.39 per 10 kg bag followed by Cape Town Market with R72.97 per 10 kg bag, and East London Market with R69.30 per 10 kg bag. In terms of Class 1 (all sizes) sales, Johannesburg, Nelspruit and Durban markets’ total sales consisted of 76%, 74% and 74% Class 1 bags, respectively – the highest of the top five markets.

Price changes

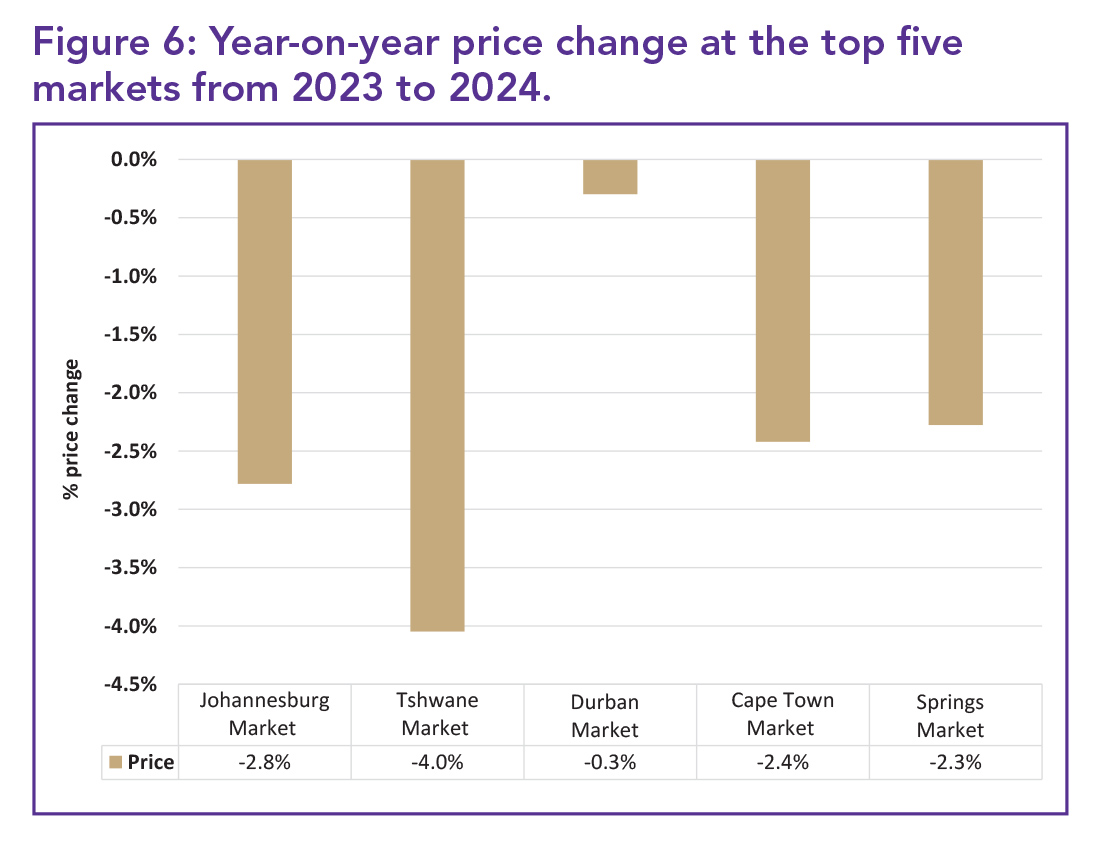

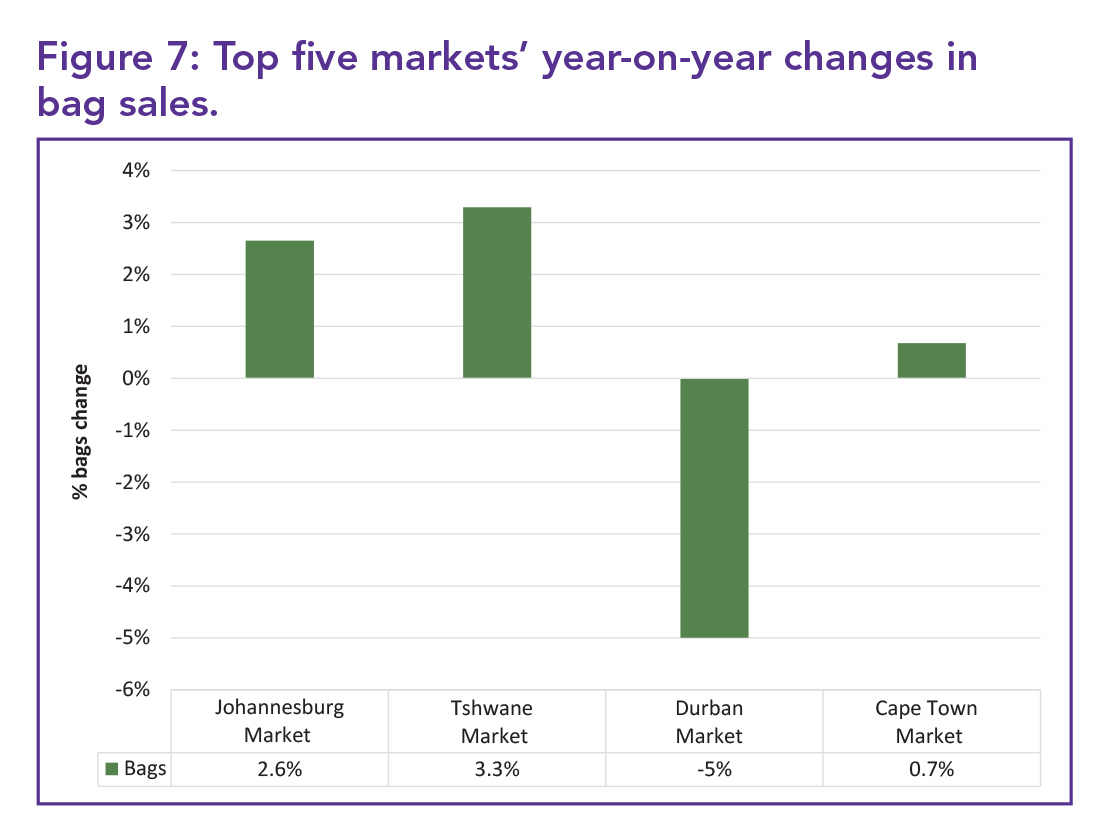

Figure 6 reflects the year-on-year price change at the top five markets for the first 39 weeks of 2024, with prices at all five markets reflecting a decrease. Tshwane Market’s price showed the greatest percentage decline with a price decrease of 4%. The volumes sold at this market increased by 3.3% year-on-year, as shown in Figure 7. The volumes sold at Johannesburg Market increased by 2.6% year-on-year.

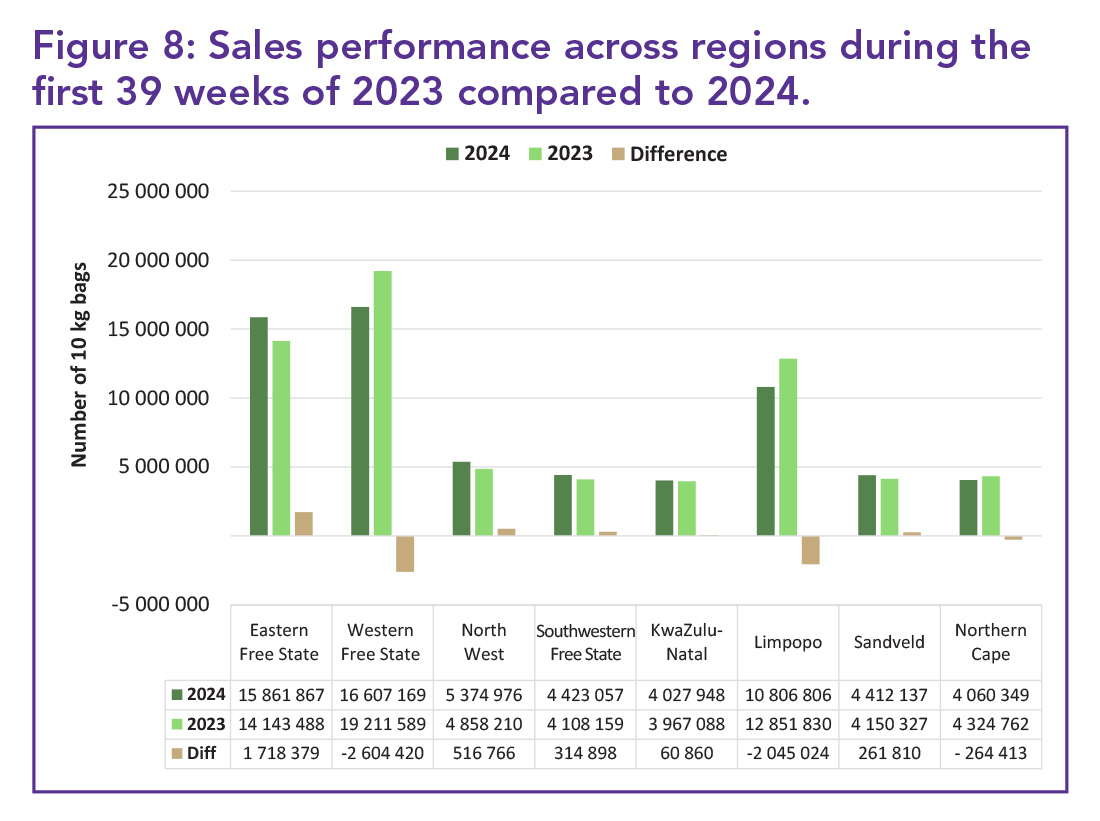

Figure 8 shows a comparison of the eight biggest regions’ sales during 2024 and 2023. The Western Free State, Limpopo, and Northern Cape regions sold fewer 10 kg bags with the other regions all selling more 10 kg bags during the first 39 weeks of 2024 than in the previous year.

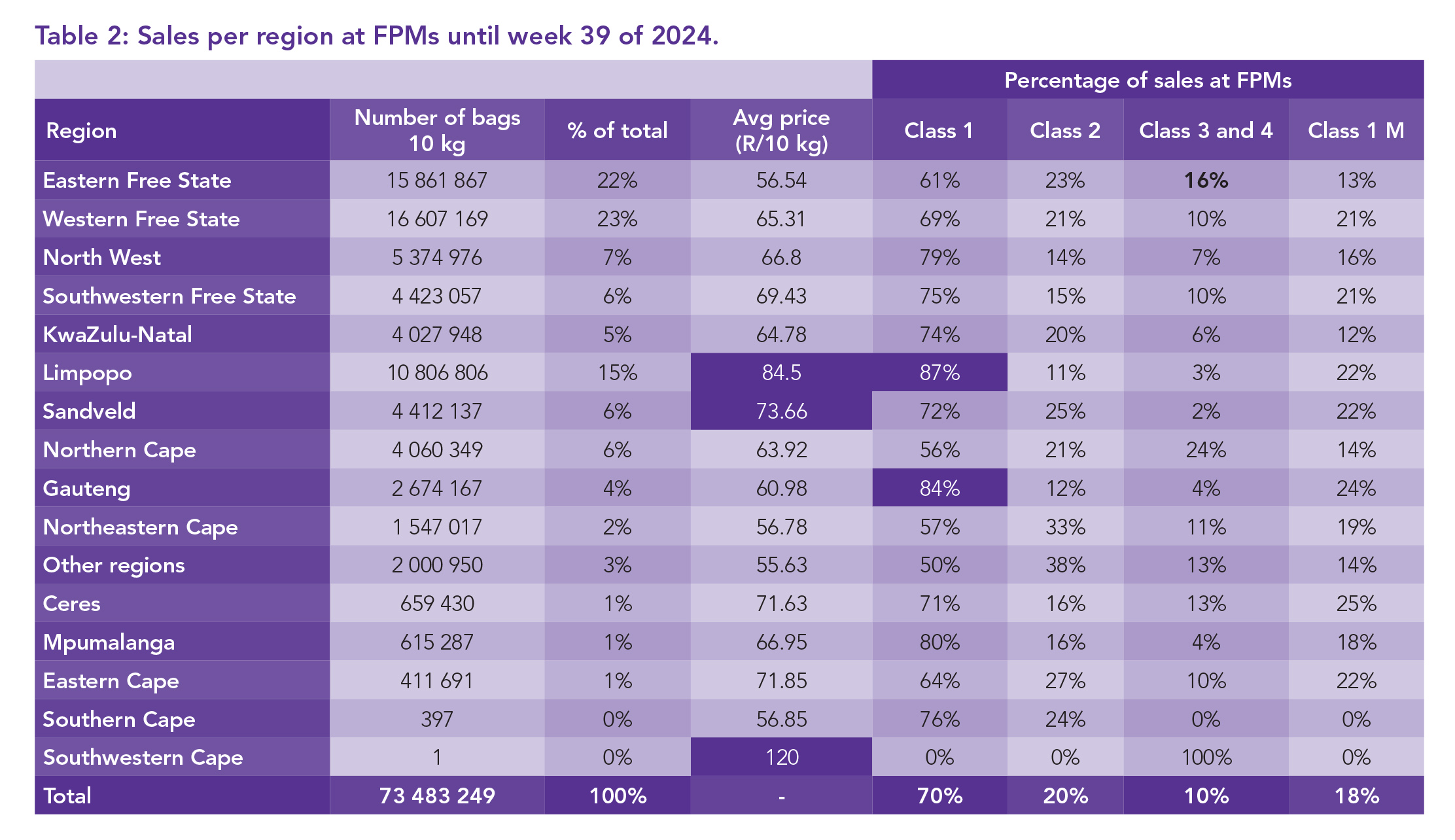

Class 1 sales

The three biggest regions in the market during the first 39 weeks of 2024, sold 59% of the potatoes available at FPMs (Table 2). Table 2 also illustrates the percentage composition of each region’s Class 1, 2, 3 and 4 potatoes supplied during this period. Twelve of the 16 regions had a percentage of Class 1 sales above 60% from January to September 2024. The top five regions in terms of Class 1 sales include Limpopo at 87%, Gauteng at 84%, Mpumalanga at 80%, North West at 79%, and Southern Cape at 76%. – Dikgetho Mokoena and Anjé Venter, Potatoes SA