Estimated reading time: 5 minutes

Potato production in the Northern Hemisphere faces challenges due to changing consumer requirements, weather patterns and pressure on crop protection strategies. In collaboration with the European Union (EU) funded Economic Partnership Agreement Support Programme, a potato markets study was commissioned to evaluate opportunities for South African potatoes in the European market.

The study concluded that there are indeed opportunities for exporting potatoes to Europe, particularly if value is added to the final product. It must be highlighted that South Africa is currently not on the list of countries permitted to supply the EU. Therefore, a trade agreement will need to be negotiated before exports can commence.

What is happening in Europe?

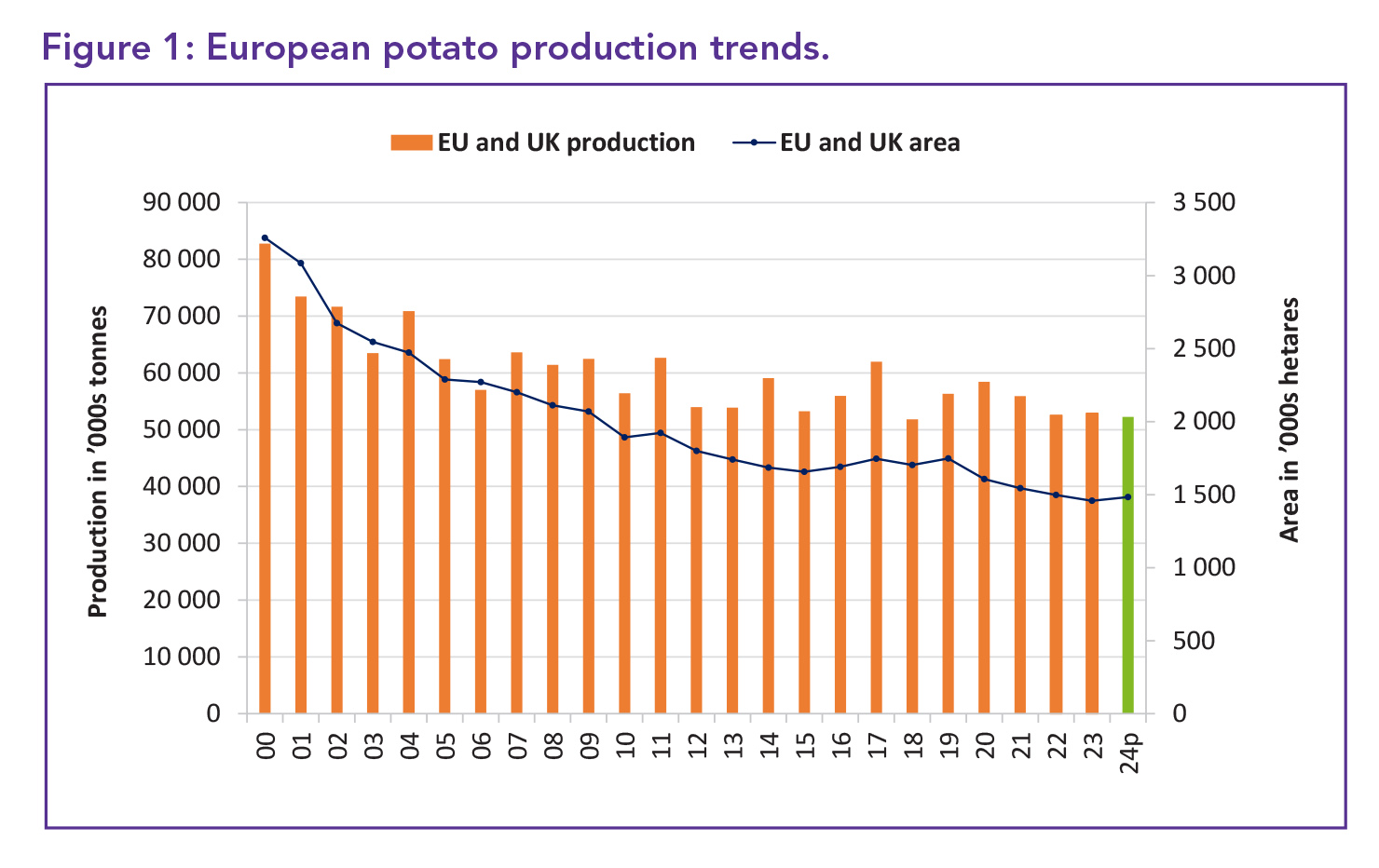

European potato production has decreased by 40% since 2000 (Figure 1). This decline is partly due to changes in EU support for starch potato production. There has been a steady decline in potato consumption in traditional markets. The high costs and risks associated with potato farming have persuaded growers to switch to crops such as cereals and oilseeds. Climate change has also posed challenges, with warmer and wetter winters making potato cultivation difficult.

Potato production in Europe may increase slightly in the coming years due to a shift away from fresh table potatoes to processing potatoes.

European consumption trends

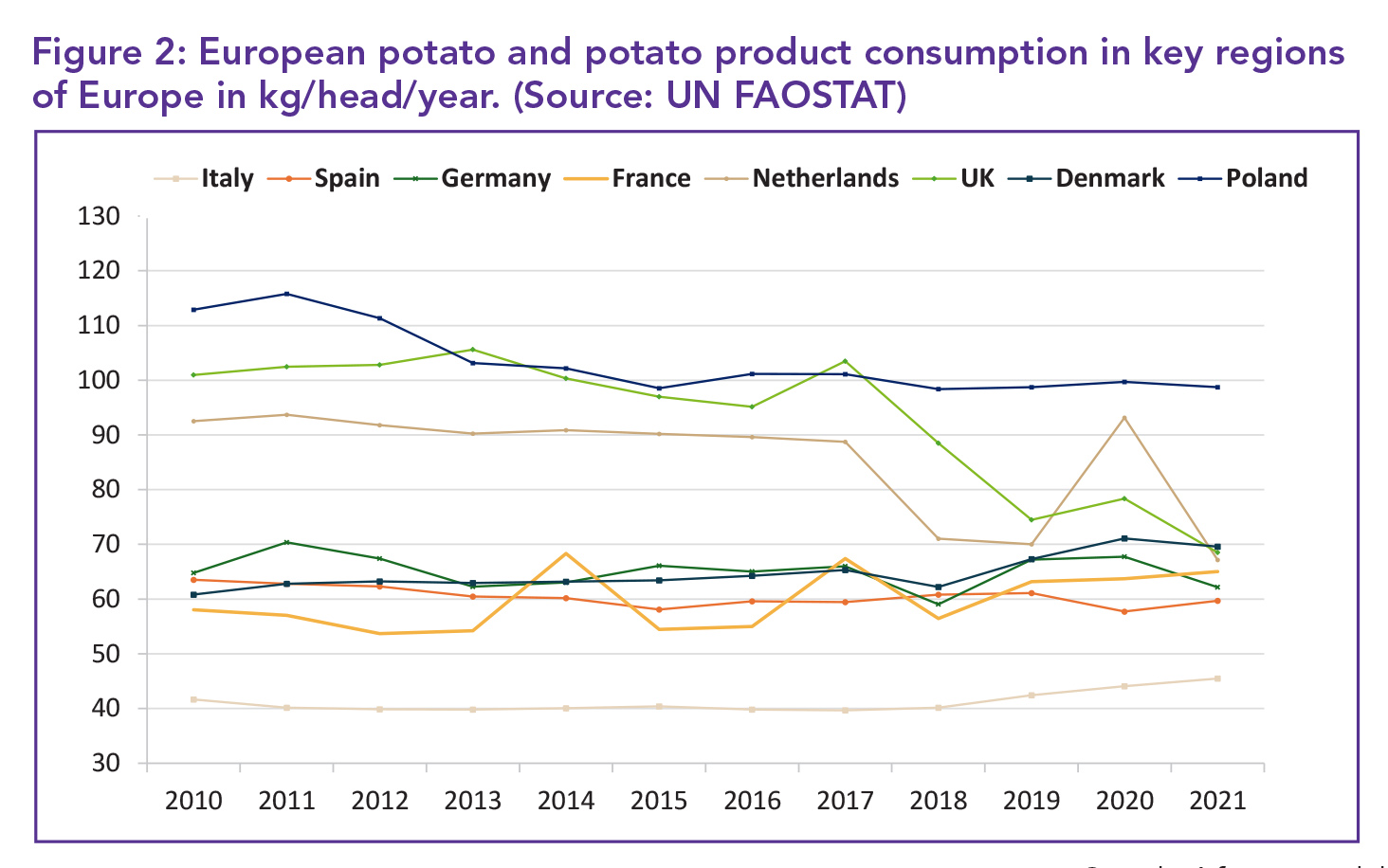

Potato consumption is declining in traditional high-consuming potato countries such as the United Kingdom (UK) and Poland. Interestingly, there has been an increase in potato consumption in countries traditionally favouring pasta, such as Italy, which is showing a rise in per capita potato consumption. In France, consumption has increased by 12.1% mainly in the out-of-home segment. Danish consumption has also increased significantly, with per capita consumption reaching 70 kg in 2021 (Figure 2).

All-rounder potato varieties still dominate sales, though their demand is gradually decreasing. Red-skinned varieties are gaining popularity, along with an increasing demand for specialty types such as fingerlings and petite potatoes. However, these represent a niche in the market.

The decline in fresh table potatoes is expected to continue, but there is evidence of increased demand in countries where potatoes have not traditionally been a staple, such as Italy, France and Spain. This trend offers opportunities for suppliers of fresh potatoes in these countries. The decline in fresh potato consumption is also linked to a shift towards processed potato products.

Export opportunities

With European potato production under pressure and a greater portion of the crop being used for processing, the continent is increasing its importation of fresh potatoes from Egypt. This country is facing challenges from diseases and geopolitics, making its supply vulnerable.

There are opportunities for exporting specific value-added potato products to Europe, as processing can help address phytosanitary barriers. Examples include crisps, salads, and prepared potatoes such as hasselback and even mashed potatoes. It must be emphasised that there is little opportunity for the supply of fries from South Africa to Europe, as Europe can competitively produce in this category.

For South Africa to succeed, it must demonstrate that it is a reliable supplier of responsibly produced potatoes. This is achievable, given South Africa’s extensive experience in exporting almost 1.6 million tonnes of fruit and vegetables to the EU annually. European traders value South Africa for its Southern Hemisphere location and its ability to supply quality produce when Northern Hemisphere supplies are low.

European potato prices have risen rapidly over the last two years, reflecting supply shortages we can benefit from.

In conclusion

The EU and the UK are major consumers of potatoes and potato products. Recently, there has been a shift from producing fresh table potatoes to processing potatoes, which presents opportunities for South African potatoes in the European market.

Due to smaller European harvests in recent years, the demand for imported potatoes has increased, particularly from Egypt. However, quality issues with Egyptian potatoes have made European buyers more hesitant.

With some policy adjustments, South Africa could position itself as a reliable supplier of fresh potatoes to the EU and UK. South Africa’s ability to produce and ship potatoes year-round is advantageous, allowing it to supply Europe during periods when its own supply is under pressure. This is specifically relevant towards the end of the European season when stocks from the previous season are running at their lowest. It is feasible for South Africa to develop a trade of at least 100 000 tonnes of potatoes to Europe annually, valued at €40 million (around R800 million).

South African potatoes are competitively priced, with significant room for price increases while remaining competitive, even when shipping costs are considered. South Africa’s existing trade in fresh fruit and vegetables with the EU is to its advantage.

There is limited potential for the export of frozen potato products to Europe, but processing in other formats for example, South African potato chips/crisps, dehydrated products or value-added options does exist. The greatest obstacle to exporting potatoes to Europe is phytosanitary restrictions, which would need to be negotiated to include on the EU and the UK’s list of approved fresh potato suppliers. This will require convincing EU and UK officials of the plant health status of South African potatoes. –Summarised by Dirk Uys, research and innovation manager at Potatoes SA,

from an EU SADC Commissioned Partnership Report by Cedric Porter from World Potato Markets