Estimated reading time: 8 minutes

Northern Europe recently experienced temperatures of around 30°C, while in southern Europe it exceeded 40°C. While rain was expected soon, it would not be enough to significantly benefit potato crops. Despite one of the driest starts to the season on record, planting conditions were favourable, especially for irrigated crops.

New data shows record or near-record potato plantings in the Netherlands and Belgium, which is pressuring the market. Even drought-affected crops are expected to yield well. Historical trends show that potato prices can rise sharply after weather-impacted seasons, but the November 2025 futures price fetched a relatively low €140/tonne.

Globally, trade tensions are growing with the return of higher United States (US) tariffs. At the same time, India and Japan are setting records in fry exports and imports, respectively.

Trump vows to impose tariffs

The 90-day pause on US tariffs, introduced by president Donald Trump in April, ended on 9 July. Trump confirmed his plans to proceed with new tariffs, potentially as high as 50%, depending on how countries ‘treat’ the US.

A blanket 10% base tariff would apply where no specific deals were struck, with 83 countries facing variable rates based on trade deficits, not reciprocal tariffs. Some deals – such as those with the United Kingdom (UK) and China – cover specific goods such as cars, steel, rare earths, and tech.

Weather

The very hot weather across Europe had an impact on potato growth. Temperatures at the time were due to drop with expected thunder showers. There were three or four days during which temperatures were above 30°C across England and Poland’s growing region. Further south, temperatures as high as 45°C were recorded.

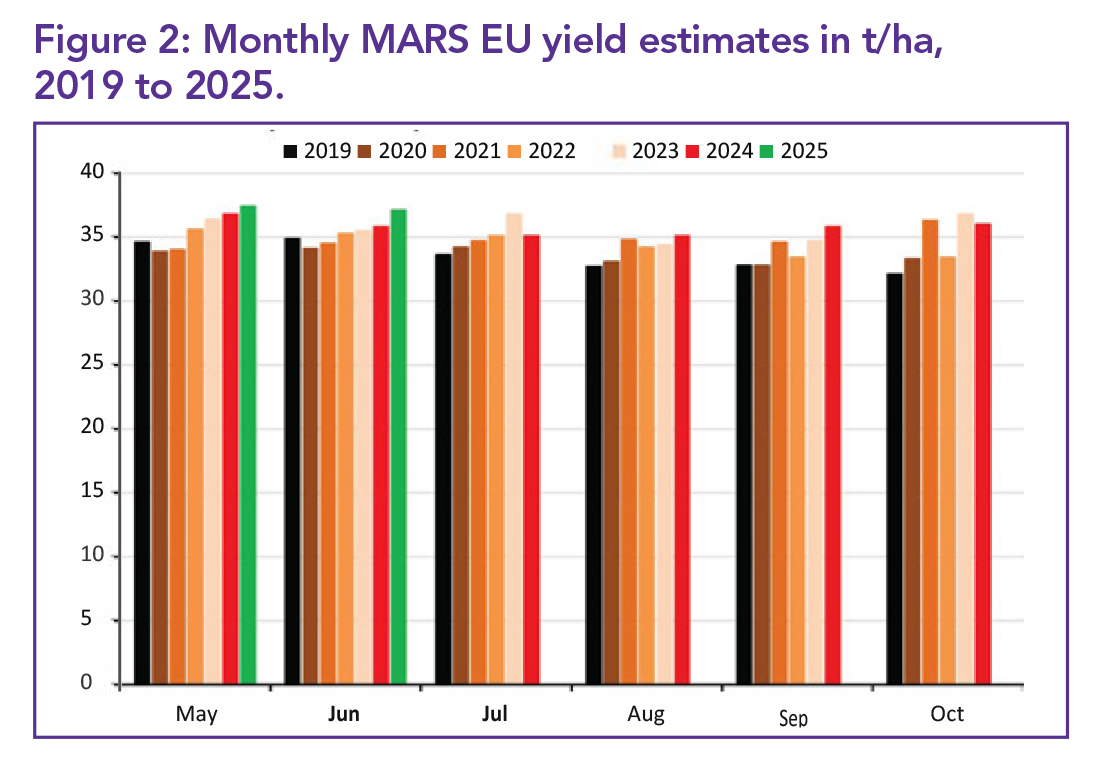

The EU’s Monitoring Agricultural ResourceS (MARS) agency lowered its 2025 potato yield forecast by 0.8% to 37.1 t/ha in June. Despite the downgrade, this was still the highest June yield estimate since 2017, and above both 2024 (+1.1%) and the five-year average (+1.9%).

However, key producing countries (Germany, the Netherlands, France, Belgium) saw a 2.9% drop in yield expectations from May to June, likely due to ongoing hot and dry weather.

Economic impact of US tariffs

- Inflation rose slightly to 2.3% in May.

- GDP fell 0.5% in Q1 2025, more than the expected 0.2% drop.

- Food prices increased 0.2% month-on-month.

Potato trade effects

- April US potato exports fell 4% year-on-year to $192.5 million.

- Sales to Mexico dropped 29%, Canada 13%, while Japan rose 24%.

- US imports of potato products declined by 9%, with notable drops from Canada (-12%) and Belgium (-17%), while Dutch imports rose 26%.

- The United States-Mexico-Canada Agreement (USMCA) protects trade with Mexico and Canada from tariffs, but that deal is up for renewal in 2026, potentially ending potato exemptions.

EU impact

Tariffs on European Union (EU) frozen fries may double to 20%, worsening already declining exports to the US – April shipments were 16% lower than April 2024 and the lowest since August 2024.

While early planting conditions at the time were favourable, the next six to eight weeks would prove critical, with continued drought threatening to cause significant damage to maincrop yields. Very warm temperatures were recorded in the North-West of the US, but night temperatures were much lower, and irrigation continued as normal.

The Netherlands

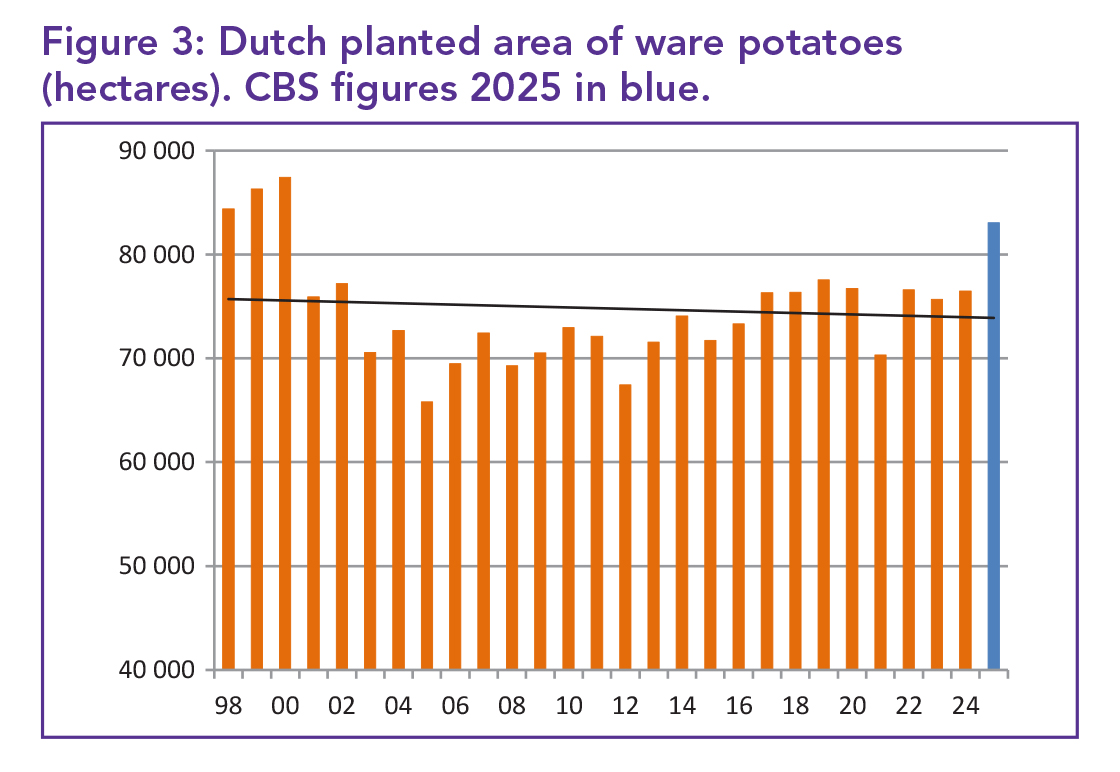

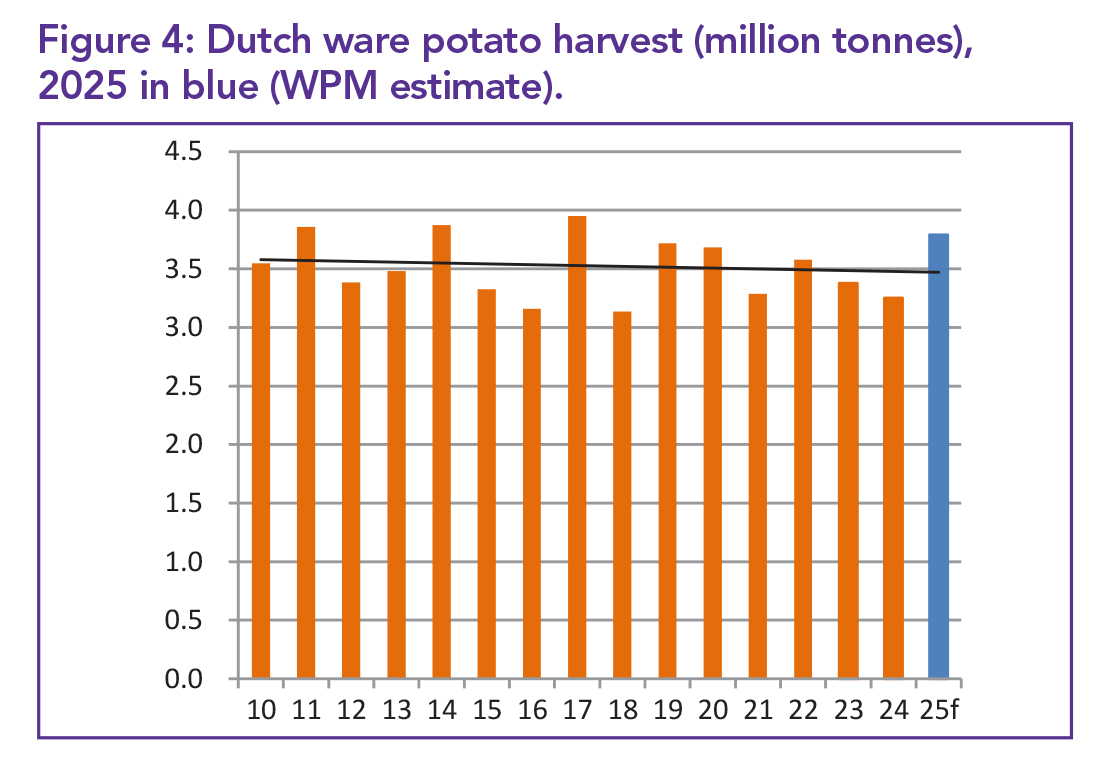

Dutch growers have planted the largest potato area since 2020. Average yield would deliver the largest crop in four years. A total of 164 372 ha was planted this year; this represents a 6.2% increase on last year. If five-year average yields (2020 to 2024) are achieved, total Dutch potato production would rise 7.9% to 6.868 million tonnes, including:

- Consumption potatoes: up 16.6% to 3.790 million tonnes (largest since 2017).

- Seed potatoes: up 3.4% to 1.483 million tonnes.

- Starch potatoes: down 2.9% to 1.631 million tonnes.

Past seasons show mixed results in hot, dry years:

- In 2022, yields reached a high 42.4 t/ha (equal best in five years).

- In 2018, drought reduced yields to 36.5 t/ha, the lowest since 1998.

Depending on conditions

- A 2022-level yield would produce 6.969 million tonnes.

- A 2018-level yield would produce 5.999 million tonnes.

Germany

Weather: Temperatures exceeded 30°C during June but were expected to drop, with rain and thunderstorms forecast in the south.

Crop area and yields: Germany has planted its largest potato area in over 20 years, but the EU cut yield forecasts by almost 3% in June, likely limiting production.

Prices

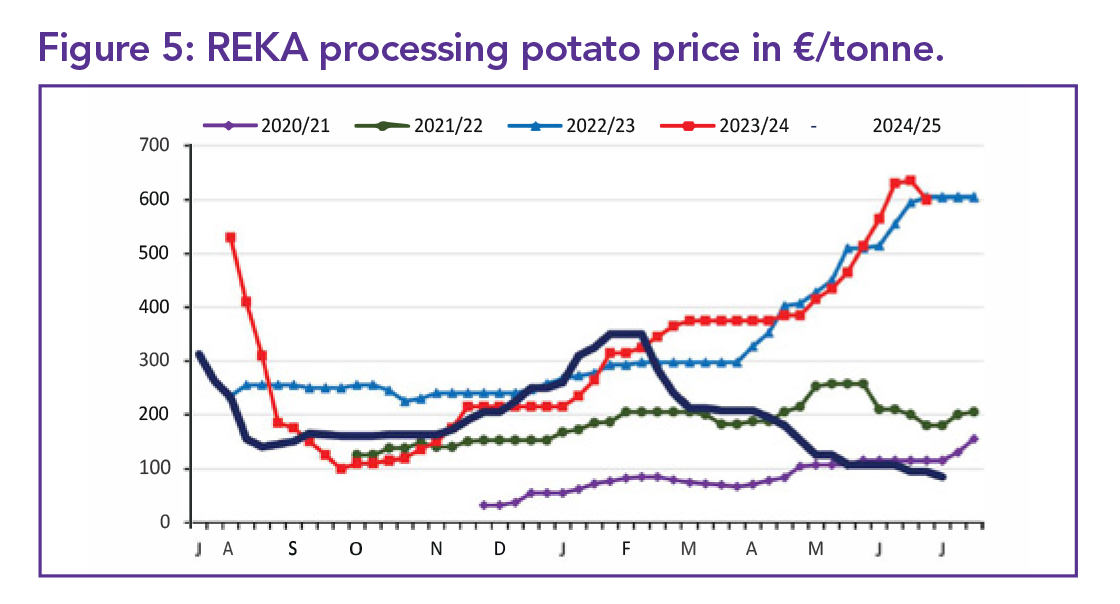

- The German organisation REKA’s processing potato prices dropped to an average of €85/t, down €10 from the previous week.

- This is the lowest price since April 2021, and €515/t lower than last year.

- Prices are also €265/t below levels seen in January/February 2025.

Seed potatoes

Seed potato area rose to a record 20 490 ha (+2.6% year-on-year), exceeding 20 000 ha for the first time.

Top varieties by area: Belana (621 ha), Fontane, Bernina, Edison, and Jelly (each >500 ha).

Belgium

The Belgium potato area is the largest ever with 111 444 ha planted. The early potato area increased by 48.5% to 8 342 ha, with virtually all of that production in the northern Flanders region. Ongoing drought will mean that the earlier plantings will be lifted earlier, putting pressure on old stock.

Maincrop (storage) potato area increased 4.9% to 99 620 ha.

- Wallonia: up 8.2%.

- Flanders: up 2%.

- Flanders’ share of maincrop area slipped from 55.3 to 55%.

Seed potato area rose 6.5% nationally.

- Wallonia: up 10.9%.

- Flanders: up 2.2%.

- Wallonia overtook Flanders as the main seed potato-growing region.

Total potato area

- Flanders: 61 138 ha (54.9% of national total).

- Wallonia: 50 306 ha.

Poland

In the second half of June 2025, there was a partial stabilisation of the market following the price collapse earlier in the month. Pressure regarding an oversupply of especially new potatoes remains. Wholesale prices of potatoes have fallen to a level not seen for many years.

United Kingdom

Drought has had an impact on the old crop market with prices dropping as growers rush to empty stores. A year ago, Maris Piper potatoes were in such high demand that prices exceeded £800/t, but now sales are scarce due to weak buyer interest, with some varieties selling for as little as £50/t.

Despite official data suggesting April 2025 prices were 69% above 2020 levels, the real increase is likely just 10%, leaving prices below input costs for the first time since 2022. At the same time, the UK has experienced a hot, dry spell, particularly in eastern England, where rainfall is well below average, and irrigation is restricted due to water abstraction limits.

India

India’s potato exports surpassed 20 000 tonnes for the third consecutive month in April, reaching 21 144 tonnes – a 45.8% increase from the previous year – and total exports for the year rose 34.3% to 190 541 tonnes. The country’s potato production also grew by 5.5% to 60.18 million tonnes, reflecting the overall strength of India’s agricultural sector, especially in Gujarat, where most processing operations are concentrated.

Japan

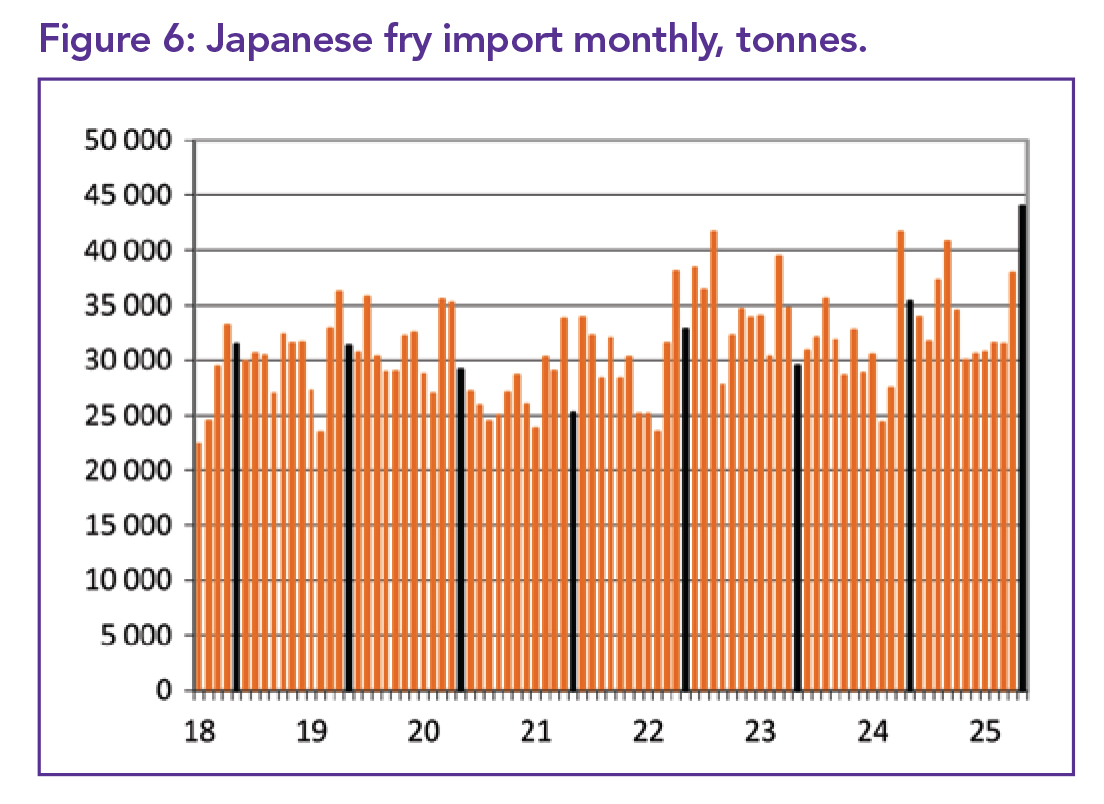

Japan’s frozen fries imports reached a record high of 44 001 tonnes in May, marking the first time the 40 000-tonne threshold was exceeded, driven partly by a rice shortage prompting demand for alternatives. This represents a 24.5% increase from May 2024, with year-to-date shipments up 9.1% to 414 366 tonnes – just shy of the all-time record set in March 2023, indicating strong and growing global demand for potatoes.

Falling prices likely boosted Japan’s frozen fry demand, with average import prices in May 2025 down 10.6% from a year earlier, though still 85% higher than in early 2021. Despite lower prices, import value rose 11.3% to ¥11.047 billion in May and reached a near-record ¥109.469 billion over the past 12 months.

The US remains Japan’s largest supplier, increasing sales by 7.6% but losing 1% market share to 61.5%, offering higher-priced fries mainly to quick service restaurants, while cheaper suppliers such as China gained ground.

New Zealand

New Zealand enjoyed its best exporting month since April 2023. In May it shifted 5 690 tonnes, a 56% increase on the same period a year ago.

Argentina

In May, Argentina’s average export price for fries fell slightly by US$9 to US$1 577/t (€1 343/t), but fry exports dropped to 16 924 tonnes – the lowest May sales since 2000, down 7.9% from the previous year and 1 394 tonnes less than April. Despite this, prices remained 2.3% higher than a year ago, even as other exporters offered discounts.

For Argentina’s biggest buyer, Brazil, May prices were US$24 lower than the previous year but still 1.3% higher year-on-year, with sales falling 10.8% to 12 051 tonnes. – Damien Da Cal, Potatoes SA

For more information, email the author at damien@potatoes.co.za or visit www.potatoes.co.za