Estimated reading time: 21 minutes

The United States (US) experienced its best month for frozen fry exports in the past 16 months during March. It also proved to be a strong month for US fry exports, marred only by continued resistance from Middle Eastern markets due to the US’s position on the war in Gaza. March’s total exports of 84,450 tonnes were the highest for the last 12 months and 10.8% up on a year ago.

But, apart from March 2023, it was also the lowest March export volume for the past five years. Average export prices remained steady at US$1,704/t (€1,582/t), which was 5.1% higher than in March 2024, but also remained US$320 higher than those of Canadian and European Union (EU) competitors.

The biggest boost to sales figures came from demand in Japan which increased by 6,300 tonnes to 25,565 tonnes, 21.9% higher than a year ago. The price was US$22 higher than in February at US$1,686/t (€1,565/t), which was 9.9% up on a year ago. Annual purchases by Japan were still 6.6% lower for the year up to March, as lower-cost imports continue to be a growing option in the country.

Sales and imports

In March, Mexico experienced a bigger price rise – a US$115 increase on February’s price to US$1,667 (€1,548/t). Even so, this was 2.2% lower than a year ago. Sales were 2,900 tonnes lower at 19,187 tonnes, but still 21.7% higher than a year ago. Annual sales to Southeast Asian customers across the Pacific were still lower for 2023/24 than for the previous year, but March also saw improvements in sales to South Korea and the Philippines. South Korea bought 7,619 tonnes, 2,400 tonnes more than in February and 57.2% up on a year ago. The price was only US$4 up on the previous month at US$1,777/t (€1,650/t), and 4.4% higher than a year ago.

The Philippines had to contend with a US$26 price increase to US$1,724 (€1,600/t), 16.1% up on a year ago. The March order was 2,300 tonnes higher at 6,847 tonnes, 48.2% up on a year ago. Elsewhere in the Pacific, there was little change in demand from countries such as Malaysia, Indonesia, Singapore and Taiwan, but Malay buyers had to cope with a 27.9% higher price than a year ago, paying US$1,802/tonne (€1,673/t) for their 2,396 tonnes. They doubled their February order, buying 784 tonnes and paying US$1,547/t (€1,436/t), which was 5% less than a year ago when they bought 1,807 tonnes.

March’s Canadian price was US$26 lower at US$1,359/t (€1,262/t). This was 11.4% lower than the year before – the biggest discount enjoyed by any of the US’s main customers. They purchased an additional 1,600 tonnes, making their March order 5,092 tonnes, which was 13.8% higher than a year ago.

March’s imports hit an all-time high of 137,900 tonnes, 19,300 more than in February and 5% higher than a year ago. Average prices were US$26 higher at US$1,473/t (€1,367/t), which was 7.3% higher than a year ago but still US$231 less than the price the US sold its fries abroad for in March.

Fry prices increased

The Canadian fry price rose US$33 to US$1,455/t (€1,351/t), which was 5.6% up on a year ago. Still, sales rose by 15,000 to 114,390 tonnes, the largest monthly consignment ever to cross the 49th parallel. The price of Dutch fries rose by US$40 in March to US$1,451/t (€1,347/t), 19.2% higher than last year. Imports rose by 1,688 to 4,324 tonnes, 29.1% higher than a year ago.

At US$1,560/t (€1,448/t), the Belgium price was 17% higher than a year ago, and still looking expensive compared to its main competitors. Egypt lowered its import price by US$32 to US$1,387/t (€1,288/t), 4.6% lower than last year, but its sales slipped by 363 to 1,155 tonnes, making it the only major importer to record lower sales in March than last.

German products priced at US$1,242/t (€1,153/t) sold just 902 tonnes, 480 tonnes less than in February and down by nearly half on a year ago. Brazilian fries, priced similarly at US$1,292/t (€1,199/t), continue to spark interest with sales of 198 tonnes, taking their annual imports up to 2,452 tonnes.

March’s imports further pushed up the US import bill for the year which now stands at US$2.074 billion (€1.93bn), some US$582 million more than the country’s export earnings from frozen processed potatoes of US$1.492 billion (€1.39bn).

Ware potato exports

There is still a need to buy raw material. A record volume of ware potatoes did not cross the 49th parallel into the US in March, but at 55,208 tonnes, it was still the highest amount for the past 12 months, although 20% lower than a year ago. Annual fresh potato import costs were still 10.9% lower at US$369.366 million (€342.9bn). Ware export earnings for the year were 11.8% higher at US$328.684 million (€305.12m) but still in deficit, like the fry trade. March exports of 18,081 tonnes were 8,800 lower than February, but still 58.1% higher than in March 2023.

Record sales for Canada

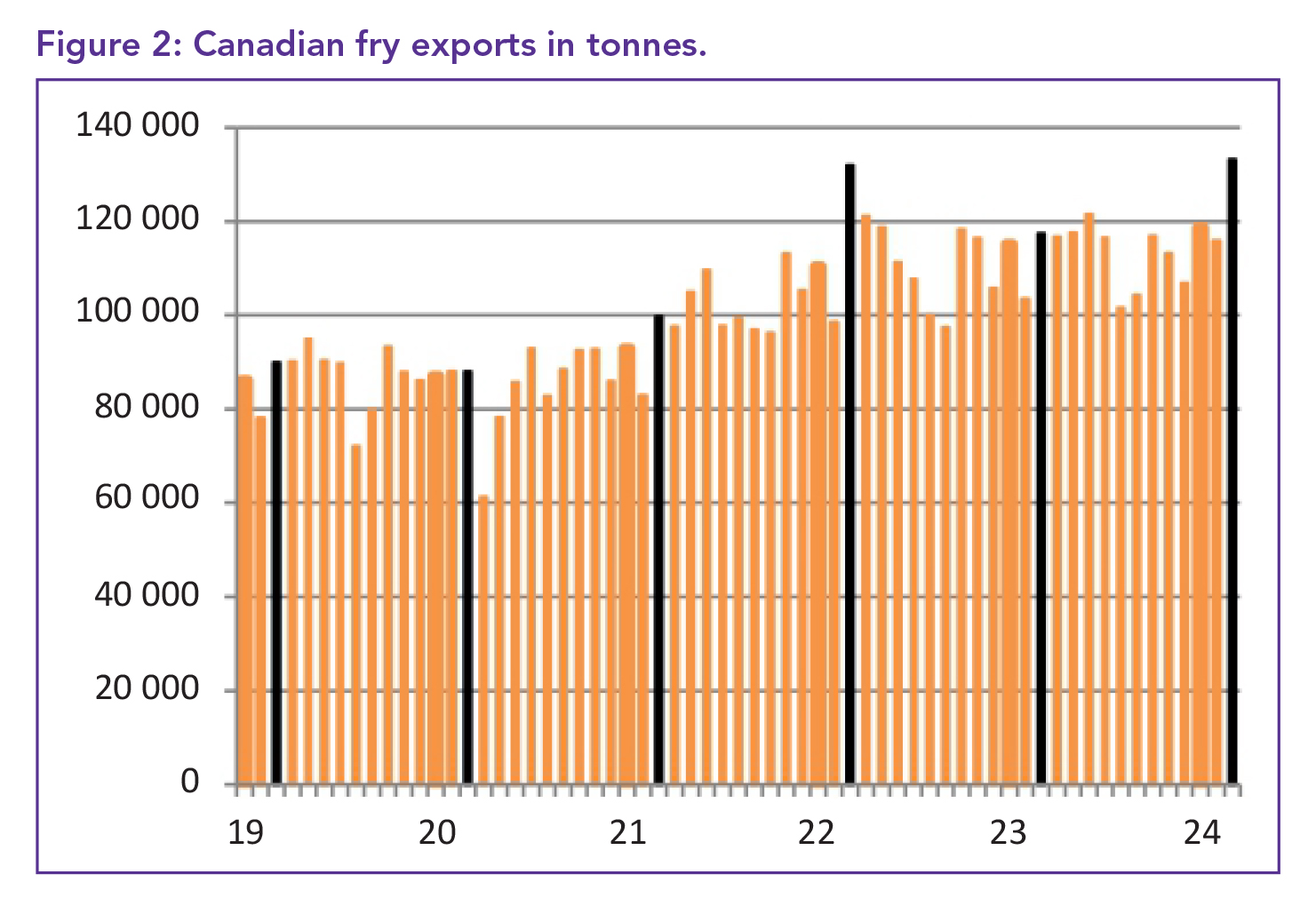

Canada fry exports and earnings hit record levels. Canada made the most of last year’s bumper crop with record March fry exports of 133,196 tonnes, earning the country C$253.462 million (US$185.28m; €172.05m), which was further supplemented by C$53.645 million (US$39.22m; €36.41m) from the sale of 55,157 tonnes of fresh potatoes to the US, its biggest ware consignment of the year.

As well as record fry sales, Canada was also able to lift the average fry export price by C$33 to C$1,903/t (US$1,391/t; €1,292/t), getting it back closer to January’s all-time high. Despite the firmness of the March price, it is only 3.1% higher than a year ago, while the US price is 5.2% higher.

The US ordered 114,460 tonnes of fries, which was 1,136 tonnes less than March 2022’s epic order. This March it paid an average of C$1,995/t (US$1,458/t; €1,354/t), C$50 more than in February, but C$53 less than January’s peak US trade. March’s order cost the US C$228.382 million (US$166.95m; €155.0m), 15.8% more than it spent a year ago, and means the US has spent C$2.310 billion (US$1.69bn; €1.57bn) on importing Canadian fries over the past year, despite the size of its own 2023 potato harvest.

With a price of C$1,394/t (US$1,019/t; €946/t), the price just 1% more than a year ago, they bought 4,642 tonnes. Buying at C$1,511/t (US$1,104/t; €1,026/t), which was slightly less than the year before, Japan bought 2,562 tonnes, 730 tonnes more than February and 10.4% higher than March 2023.

Sales and ware exports

Canada’s sales were overtaken by Panama which bought 2 947 tonnes in March, an increase of 145% on a year ago. Its price was an unrepeatable C$1 208/t (US$883/t; €820/t), C$42 lower than in February and 19.3% less than in 2023. Its March price of C$1 187/t (US$868/t; €806/t) was 14.7% less than in 2023.

Although Australian sales prospects continue to recede (March saw it buy just 481 tonnes, which was better than the previous two months), Canada’s annual exports are still 3.7% higher at 1.383 million tonnes, another all-time high. Annual exports of fresh potatoes are 15% lower than last year at 557 257 tonnes, with annual earnings 8.1% lower at C$548.034 million (US$400.6m; €372m).

March ware exports were 17.2% lower at 60 330 tonnes, but there was still strong demand from the US taking 55 157 tonnes and paying an average of C$969/t (US$708/t; €658/t), 1.4% higher than a year ago. Canada’s imports of fries rose by 1 374 to 4 746 tonnes in March, the highest volume since last June. Some 77%, 3 677 tonnes, came from the US, at an import price of C$2 394/t, (US$1 750/t; €1 625/t), C$142/t up on February’s price and 6% higher than a year ago.

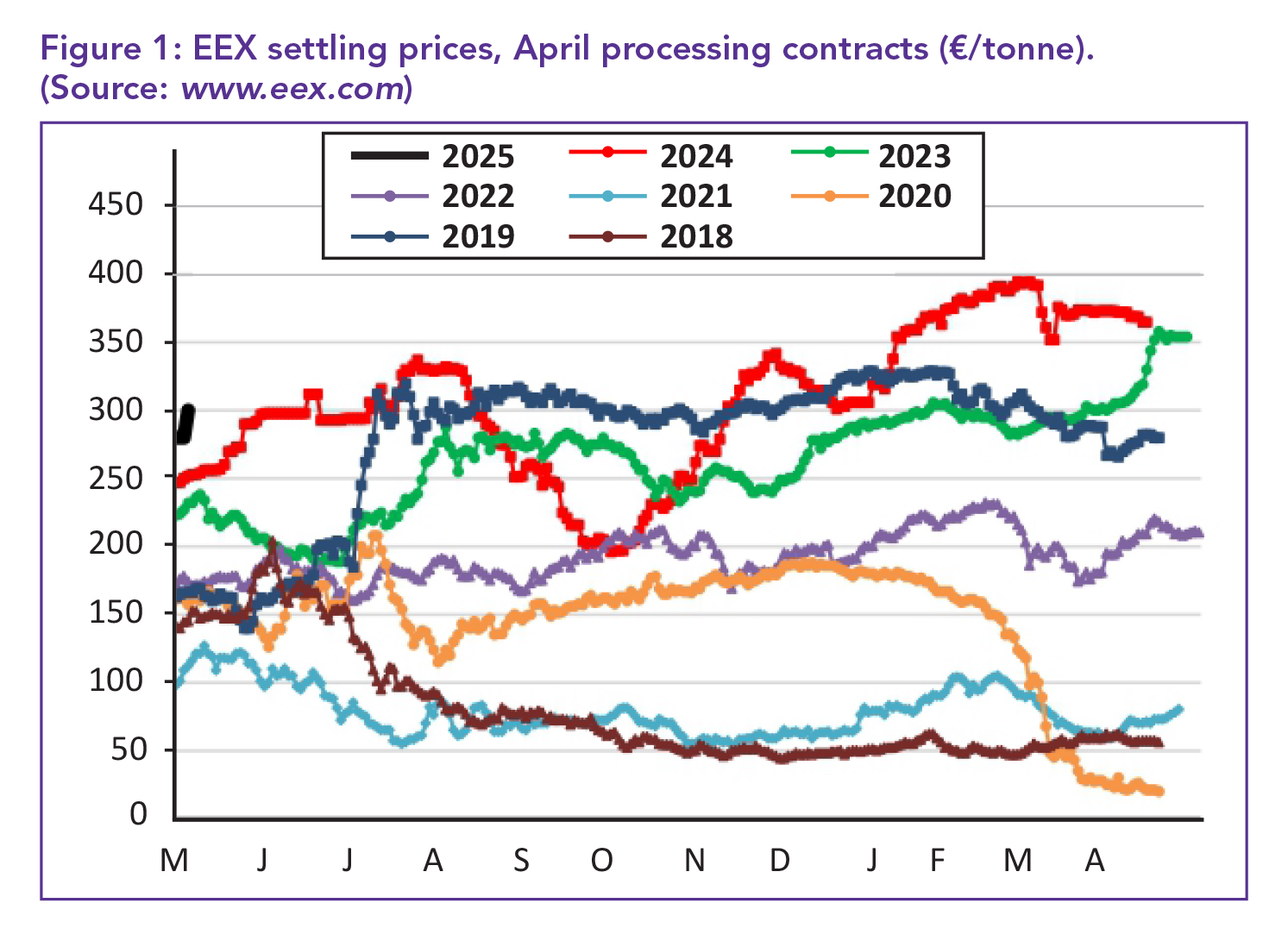

European potato scarcity

A break in the weather allowed European growers to make significant progress in planting, but subsequent rainfall has caused delays. Germany made the most progress in planting, having avoided the worst of recent rain that affected other parts of Europe. Despite this, Germany was still behind its usual planting schedule. In contrast, Belgium had only planted a fraction of its crop.

European processors are actively seeking more potatoes, willing to pay between €400 and €500/t. The European Energy Exchange futures market reflects this demand, with June values exceeding €430/t. The scarcity of potatoes in Europe has led to a surge in French ware potato exports. Additionally, there has been a notable increase in the value of Brazilian fry imports, reaching €44 million in April, an 83% rise from the previous year. Mexican imports also showed signs of recovery, with positive developments for US shippers in the Philippines and Indonesian markets.

France saw surge in market

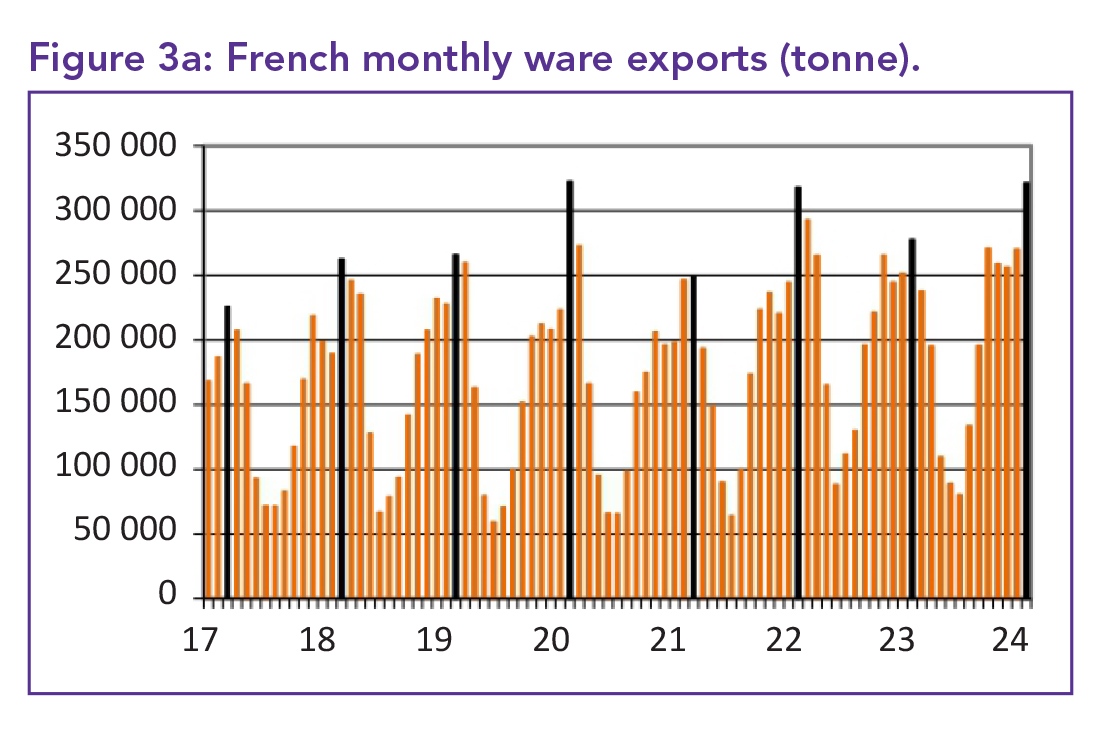

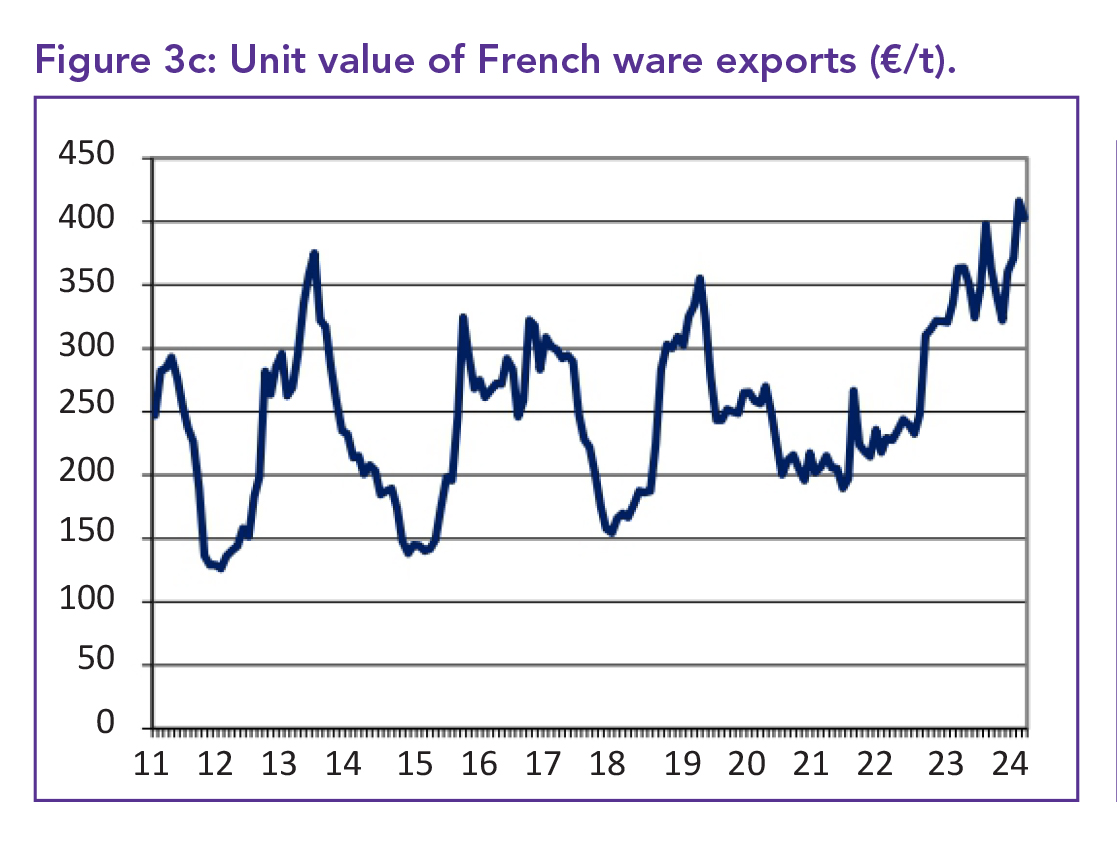

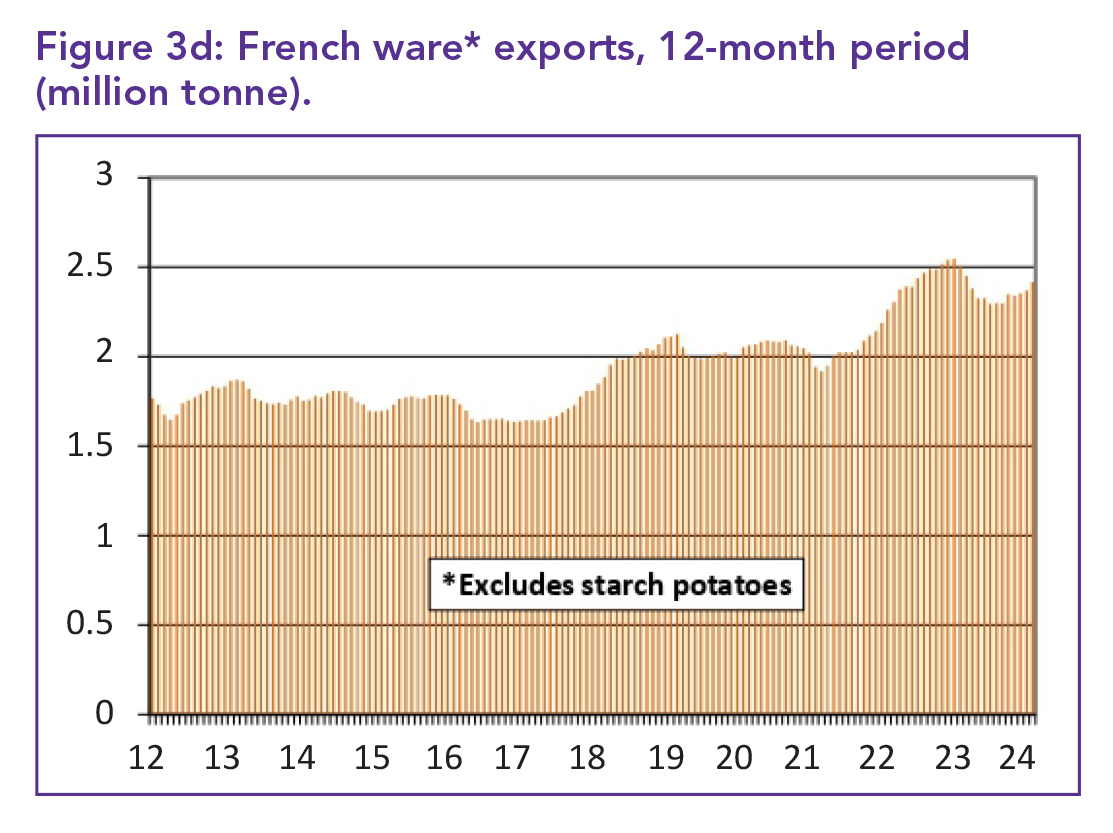

In March, France achieved a new monthly record in ware potato exports, sending out 321 145 tonnes of consumption potatoes, marking a 6.3% increase from March 2023. This export volume is almost a record high, with only March 2020 surpassing it at the onset of the Covid-19 pandemic.

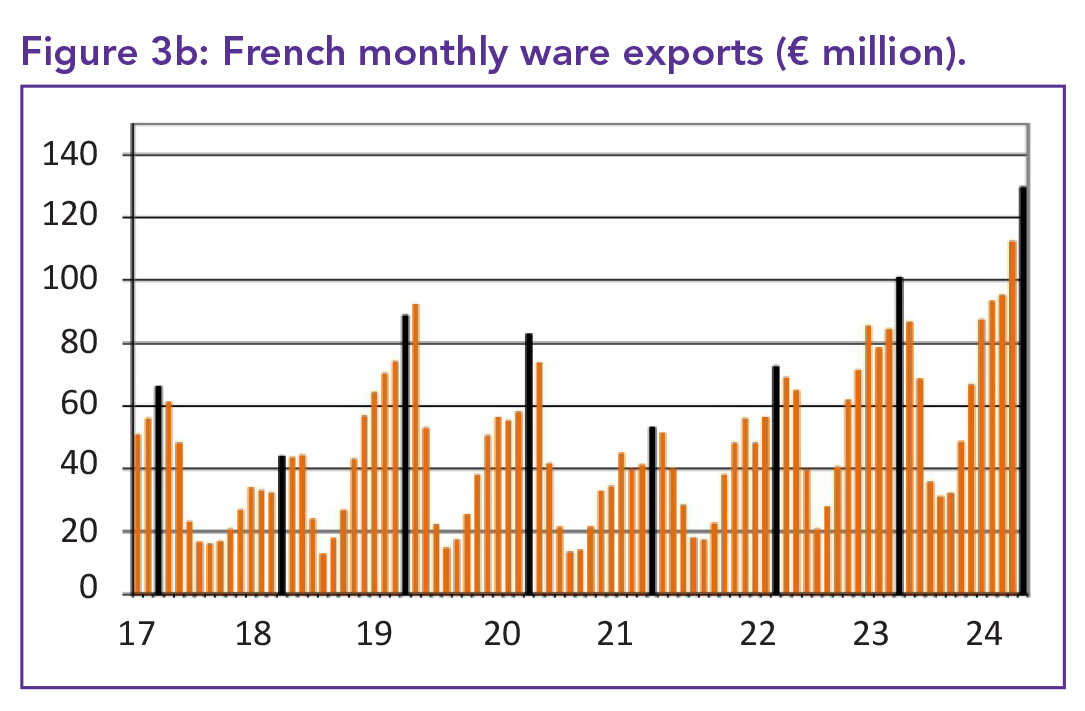

The surge in exports is driven by high demand from other countries facing shortages, as France traditionally exports the most potatoes in March when stocks are still sufficient. However, the record export volumes have led to a strain on supply, putting pressure on sales. Exports reached a new monthly record value of €129.479 million, marking only the third instance where sales exceeded €100 million. This achievement follows the previous milestones set in February of the current year and March 2023. The average price of French potato exports in March stood at €403/t, reflecting a substantial 55.1% increase compared to the same period last year.

Spain emerged as the primary market in March, importing 100 079 tonnes of French potatoes, representing a 4.3% growth from March 2023. Conversely, sales to Belgium decreased to 77 754 tonnes compared to the previous year. Notably, there was heightened demand from the Netherlands, with significant increases observed in shipments to Eastern European countries and Greece.

The overall demand from regions further east and south contributed to a 6.5% rise in total French potato exports over the nine months leading up to the end of March, totalling 1.983 million tonnes. In March, the demand for French seed potatoes decreased due to late planting in Belgium, resulting in a 14% decline in exports compared to the same month last year, with only 23 503 tonnes exported. However, despite this drop in demand, total seed potato exports for the nine months leading up to the end of March increased by 0.4% to 168 346 tonnes.

Seed export price increase

The value of these exports also rose significantly by 19.6% to €106.677 million. Furthermore, the average price of seed exports increased by 19.2% over the season to reach €634/tonne. Sales of French potatoes to Belgium saw a notable decline of 39.2% compared to March 2023, amounting to 8 106 tonnes. Over the nine months leading up to March, sales to Belgium were 25.8% lower, totalling 22 177 tonnes. Despite this decrease in sales to Belgium, there has been an improvement in sales to other EU markets, with a significant 21.9% increase in demand.

Regarding potato prices, there were no export quotations available from RNM. However, table potato prices experienced an increase due to a tightening of supply. The benchmark Category I Nord Basin price rose by €10/t to €580, maintaining the same value as at the beginning and end of the previous season.

Other Category I and II potato types also saw price increases. In terms of processing potatoes, there was no change in price during the week, with Innovator maintaining a €10/t premium over Fontane and Challenger. Processors are eager to secure supplies, but growers are reluctant to release potatoes unless the price meets their expectations. Planting progress in France indicates that around two-thirds of the national crop has been planted, slightly lagging behind last year’s progress but significantly behind previous years.

Drop in UK exports

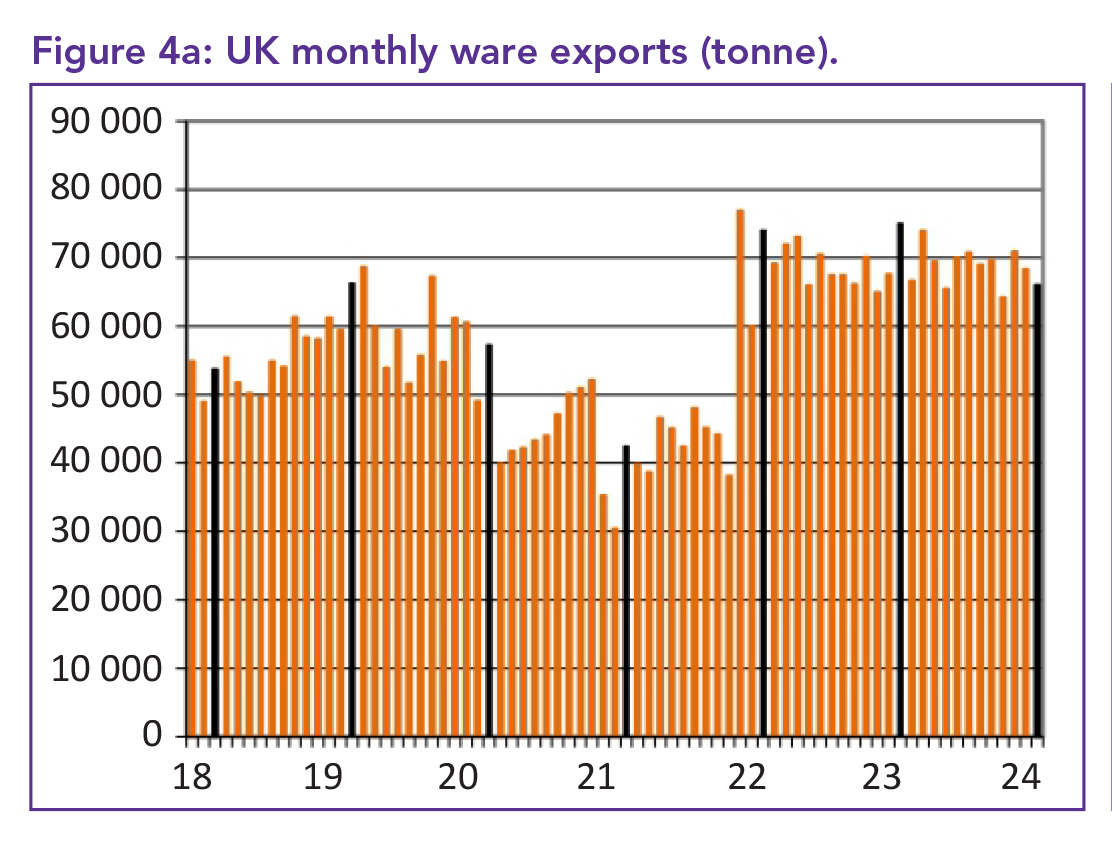

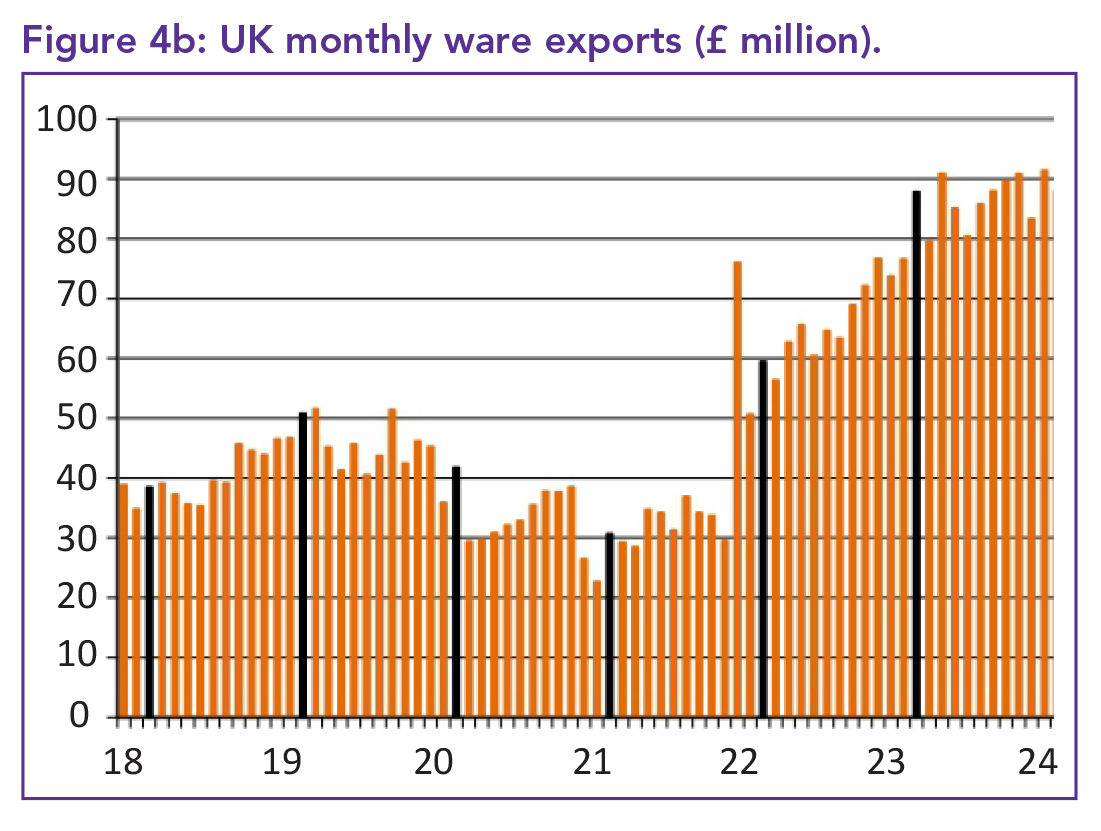

The United Kingdom (UK) is experiencing a decline in fresh potato exports and an increase in imports due to supply pressures. In March 2024, the UK exported 10 704 tonnes, a 47.8% reduction from March 2023, but higher than February 2024. Over the nine months to the end of March, exports were a third lower at 99 139 tonnes. Despite lower demand, higher prices have partially offset the decline, with the average export price in March at £673/t, a 63.4% increase from March 2024. The total value of exports for the nine months was £58.371 million, down by 4.1%.

Ireland, facing its own potato shortage, increased its imports from the UK by 8.5% to 7 514 tonnes in March compared to the previous year. Over the nine months, Irish imports from the UK were 1.5% higher at 48 835 tonnes. Among major importers, only Norway and Poland saw an increase in demand in March. Spain, the UK’s second-largest market, experienced a 37.9% decrease in shipments over the nine months. UK imports of potatoes exceeded exports by 2 576 tonnes in March, totalling 13 280 tonnes, a 130.2% increase from the previous year. The nine-month total was 50 088 tonnes, up by 31.8%.

In terms of seed exports, the UK saw a 21.4% increase in March shipments to 3 457 tonnes, with total exports up by 0.5% to 92 150 tonnes over the season. The value of seed exports for the nine months was £66.676 million, a 4.9% increase from the previous season. The average price of seed exports rose by 41.3% to £725/t. Egypt remained the largest buyer of UK seed despite a 4% drop in seasonal demand. Morocco and Saudi Arabia showed demand increases, while Spain reduced its demand. Import of seed increased slightly by 3.9% in the nine months to the end of March.

Expectations exceeded in Portugal

In Portugal, the early potato harvest has commenced in Peninsula de Setúbal, located south of Lisbon. Producers in the region have reported good quality and regular yields for the crop, which have exceeded expectations despite heavy rains and disease attacks in March. The yield is approximately 50t/ha, and the potatoes are of exceptional quality, fetching prices ranging from €550 to €600/t for the initial plots.

The average ex-farm price of new potatoes in Portugal was €770/t in the week ending 5 May, remaining stable compared to the previous week. However, this price reflects a 17.2% decrease from the same period last year and a 17.6% increase compared to the same week in the triennium 2021 to 2023.

Good weather benefits Germany

In Germany, the planting rate for potatoes was higher than that of other countries due to favourable weather conditions. More than three-quarters of the planned area has already been planted, with the rate likely higher than the previous year. Both the northern and southern regions of the country were expected to avoid the heavy rain forecasted for western countries, allowing planting to continue uninterrupted.

The shortage of potatoes from the 2023 harvest, coupled with increased demand from processors, has led to a rise in free-buy potato prices in Germany. The average price quoted by the Rhineland organisation, REKA, is currently at €415/t, which falls within a range of €400 to €430/t. This price level is slightly lower than the prices seen at the same time last year, which were as high as €600/t in May and June.

Dutch hopeful after late planting

In the Netherlands, rain returned after a period of drier weather that facilitated planting, with temperatures around 20°C expected to aid in the development of the planted crops. The planted area surpassed 40% at the time, with a significant increase in planting observed.

However, this planting rate is still lower than that of the previous year, which was characterised by late planting. In typical years, most of the crop would already be in the ground by mid-May. Late planting poses risks as the crop may need to remain in the ground longer, increasing exposure to wetter weather conditions. This scenario occurred last year when a late-planted crop faced challenges during a wet autumn, leading to some crops being abandoned due to harvesting difficulties.

The scarcity of the 2023 crop and the delayed planting of the 2024 crop continue to impact free-buy prices in the Netherlands. The latest average potato price surged by €40/t, reaching €430/t. This price was €10/t higher than the same period last year, although it remains lower than the end-of-month price in May 2023. Additionally, other prices have also increased, with lower-grade flaking potatoes fetching almost €200/t. Growers are hopeful for a price trend similar to that of the previous year, where end-of-season values reached almost €600/t.

Old-crop market strong in Belgium

In Belgium, planting progress accelerated, with more than a third of the national crop now in the ground, similar to the planting area at this time last year. However, this progress was hindered by rainfall in May, causing the planting rate to fall behind compared to the previous year. In 2023, growers were still planting into June to compensate for the late start.

Organisations such as PCA and Fiwap reported that almost all early-planted crops were sown in May, but only 25 to 35% of the main crop was planted. Progress varied regionally, with some areas at 50% planted while others are at 20%.

The old-crop market remains strong in Belgium, with processors re-entering the market. However, growers with free-buy potatoes were hesitant to sell as they expected further price increases in May due to delays in the 2024 crop’s arrival.

In line with expectations, the free-buy prices for Fontane and Challenger rose by €50 to €400/t last week. The price gap between free-buy and contract prices is currently at its widest this season, reaching almost €140/t. Limited price increases were observed in the PCA/Fiwap quotations, with Innovator regaining its €10/t premium over Fontane and Challenger, priced at €410/t.

Despite a 3.5% decrease in price compared to the previous year, Belgian fries were relatively expensive at US$1 503/t (€1 393/t). India, with reduced prices at US$1 243/t (€1 152/t), saw its fry sales surpass those of the US.

Record imports for Brazil

Brazil’s ambitions to reduce its reliance on imported fries appear to be over as April saw it record its highest ever imports for April of 34 998 tonnes, with monthly spending reaching an all-time high of BRL247.153 million (US$47.93m; €44.42m), 83% higher than April 2023. April’s average import price of BRL7 062/t (US$1 370/t; €1 269/t) was just 3.9% higher than a year ago.

The price of April’s largest supplier, Argentina, was BRL50 lower than in March at BRL8 073/t (US$1 566/t; €1 451/t) as the continuation of that country’s currency controls continued to aid its exporters. Imports from Belgium were only 1 100 tonnes higher than in March at 12 861 tonnes, but this was 153.2% more than a year ago. The Belgian price of BRL6 180/t (US$1 198/t; €1 111/t) was almost BRL180 higher than in March, but 11.4% lower than what it had been a year ago.

Twelve-monthly imports from Argentina were still 18.5% lower than the previous year at 139 400 tonnes, while Belgian imports for the same period were 15.4% lower at 102 879 tonnes. Sales were more than 1 200 tonnes higher in April at 2 352 tonnes, which was its best month for imports.

The Egyptian price was BRL5 382/t (US$1 044/t; €967/t), BRL82 higher than a month ago. Brazilian buyers also tested the water with other suppliers in April: The US sold 46 tonnes at BRL10 013/t (US$1 942/t; €1 800/t), Poland sold 49 tonnes at BRL8 716/t (US$1 690/t; €1 567/t) and China sold 24 tonnes at an inviting BRL4 771/t (US$925/t; €857/t). May’s import bill of BRL247.153 million follows March’s import bill of BRL207.536 million, 22.5% higher than a year ago and BRL36.656 million more than December’s bill.

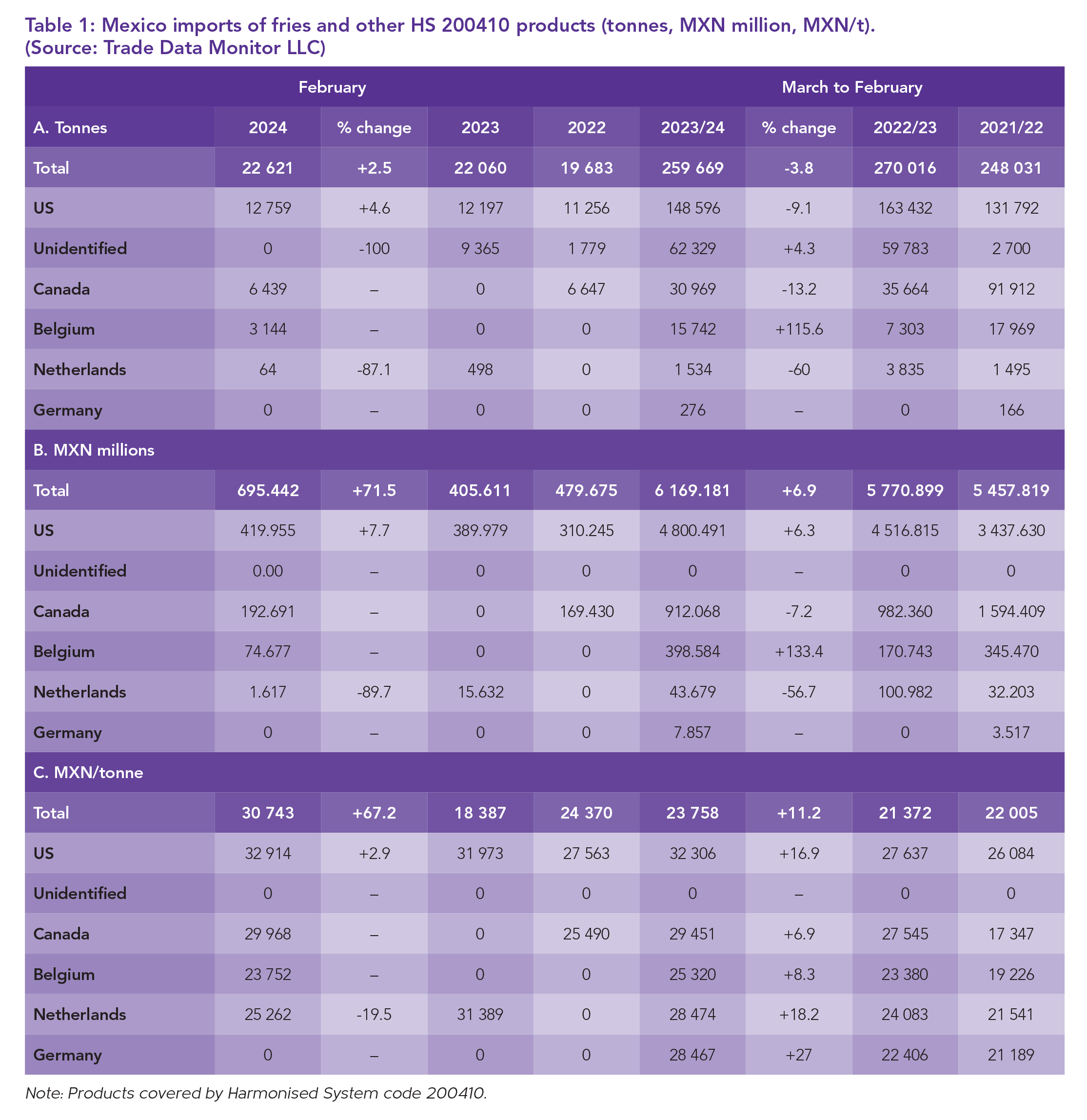

Mexico’s transparency pays off

Mexico experienced an increase in import volumes of processed potatoes during the first two months of 2024. February saw imports of 22,621 tonnes, which was 2.5% higher than the previous year but 2 350 tonnes less than January’s 24 970 tonnes, the highest monthly figure since October 2022. The average prices recorded by WPM were MXN4 000/t higher than in December, mainly due to the Mexican Economy Ministry’s decision to stop listing some imported fries as ‘unidentified’. This move towards greater transparency is a positive development for the market.

With no unidentified volumes recorded, January and February witnessed higher fry imports from both the US and Canada. In January, the US imported 15 538 tonnes, up from 19 346 tonnes in December, while Canada imported 7 274 tonnes, up from 5 656 tonnes in December. February’s imports from both countries were slightly lower, with the US importing 12 759 tonnes.

The US reduced its price by MXN2 000/t in January to MXN30.123/t, helping secure a large order. However, by February, the import price rose again to MXN32.915/t. Canada’s prices also fluctuated, with January seeing a rise to MXN30.198/t and a decrease to MXN29.968/t in February.

Compared to their main EU competitors, Belgium and the Netherlands, both the US and Canada are currently more expensive. In February, Belgian fries were priced at MXN23.752/t, while Dutch fries were priced at MXN25.262/t. Germany was absent from the Mexican sales roster, with Poland making an entrance by selling 224 tonnes at a price of MXN29.071/t.

The annual cost of importing fries into Mexico appears to be increasing, partly due to the absence of value for ‘unidentified’ imports in the official statistics in 2023, leading to lower averages. The agreement allowing greater access for US fresh potatoes into the Mexican market resulted in a significant increase in shipments, with February 2024 seeing a 147% rise in fresh US potato imports compared to February 2023.

Indonesian imports increase

In March, Indonesia experienced a slight improvement in fry imports, with sales increasing by 1 150 tonnes to reach 5 134 tonnes. However, this figure still represents a 42% decrease compared to the previous year. Despite the growth of the Indonesian economy by 5.1% in the first quarter of 2024, annual fry imports have declined by 12.7% to 81 470 tonnes compared to the previous year. The average import price for fries in Indonesia in March was US$1 524/t (€1 412/t), which is 2.7% lower than the previous year. The decline in prices might have contributed to the increase in demand during the month of Ramadan. Notably, China was the largest seller in March, with sales of 1 552 tonnes. Although this represented a 24.7% decrease compared to the previous year, China managed to lower its price to US$1 234/t (€1 144/t), making its fries more competitive in the market. The US increased its price in May by US$55 to US$2 120/t, while India reduced its price by US$27, selling at a much lower US$1 243/t, 19% less than a year ago. India has seen its annual sales increase by 44.8% to 8 747 tonnes.

FAO values small-scale producers

The Food and Agriculture Organization of the United Nations (FAO) emphasises the crucial role of small-scale family producers, particularly women, in preserving the diverse spectrum of potato crops. The FAO International Day of the Potato, celebrated on 30 May, served as an opportunity to raise awareness about the importance of this versatile crop and its contributions to global food security and sustainable agriculture. Additionally, the cultural and culinary aspects of potato cultivation and consumption are celebrated on this day.

The FAO provides a brief history of the potato:

• Originating in the Andes, the potato was vital to the Inca civilisation and revered as the ‘flower of ancient Indian civilisation.’

• Introduced to Europe in the 16th century, the potato contributed to urbanisation and fuelled the Industrial Revolution.

• During the Qing Dynasty, the potato played a key role in alleviating famine in China, establishing itself as an essential crop.

• In times of conflict, such as World War II, the potato’s high yield and resilience ensured food security during shortages.

• The Great Famine in Ireland during the 1840s serves as a stark reminder of the consequences of a lack of genetic diversity in potato crops and cropping systems.

• Today, the potato is recognised as a symbol of food security and a cornerstone of sustainable agriculture. With over 5 000 potato varieties available, they offer a rich genetic resource to combat pests, diseases, and the impacts of climate change, guiding sustainable agricultural practices.

World Potato Congress

The World Potato Congress held in Adelaide, Australia in June 2024, focussed on the theme “Old world meets new”. This theme aimed at highlighting the historical significance of potatoes as a staple food, the innovative technologies applied to their production, and the substantial investments in research and development. The event addressed global changes in sustainability, climate, culture, and population dynamics. – Francois Strauss, Potatoes SA

For more information, email Francois Strauss at francois@potatoes.co.za or visit www.potatoes.co.za.