Estimated reading time: 5 minutes

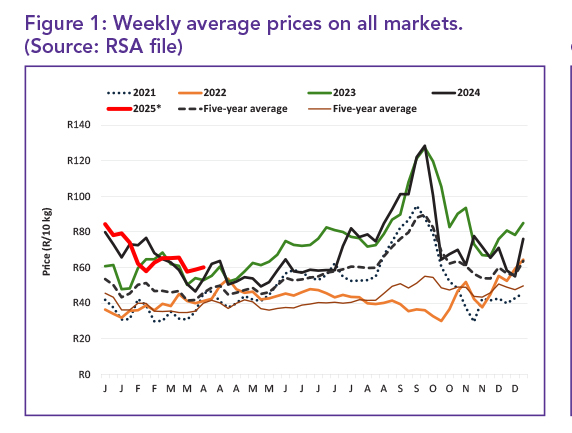

The average weekly price of potatoes during the first 13 weeks of 2025 showed a slight increase, with the week 12 price increasing by 2%, the same increase as in week 13.

As illustrated in Figure 1, which tracks the weekly average price across all markets and potato classes and sizes, the average price in week 13 stood at R60.09 per 10 kg bag. This represents not only a week-on-week increase but also a year-on-year increase of R6.46 compared to the corresponding week in 2024, underscoring heightened price volatility and market fluctuations.

Supply and demand

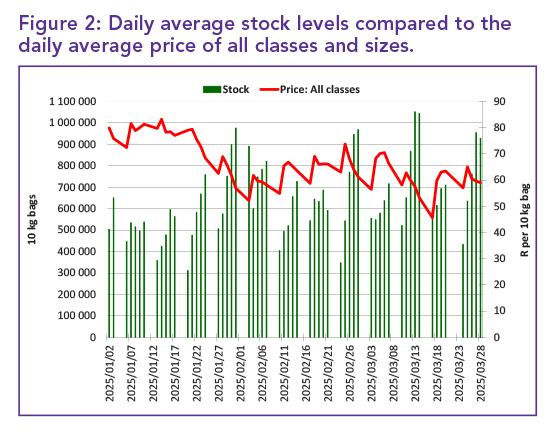

Figure 2 provides insight into the interplay between supply and demand by analysing daily average stock levels and price movements. On average, there were 646 106 10 kg bags in stock daily across South Africa’s fresh produce markets (FPMs) during the first 13 weeks of 2025.

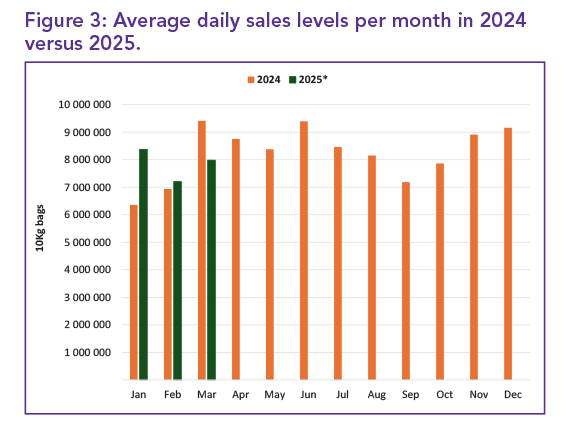

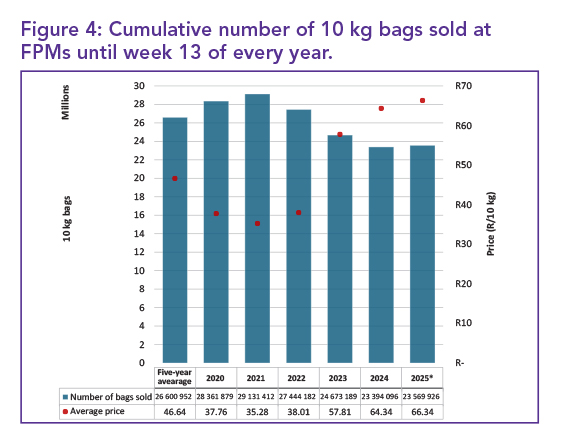

Figure 3 compares monthly sales levels year-on-year, highlighting a 10% decline in March 2025 compared to March 2024. The cumulative sales volume in the first 13 weeks of 2025 remained 3.03 million bags below the five-year average for the same period. Nonetheless, the total sales volume exceeded 23.5 million 10 kg bags, as shown in Figure 4.

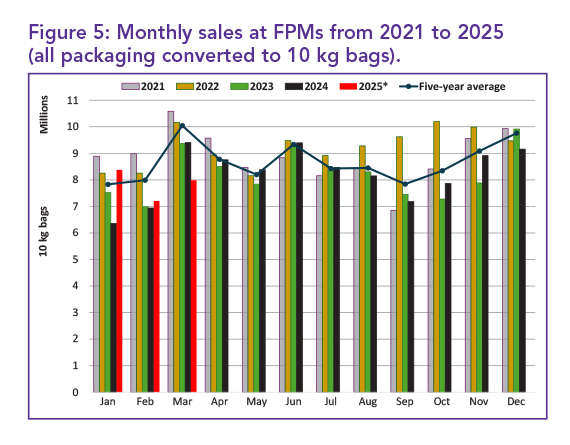

Monthly sales trends at FPMs, depicted in Figure 5, indicate a marginal month-on-month increase, with March 2025 recording 7.9 million 10 kg bags sold, compared to 7.20 million bags in February 2025.

This represents a volume increase of 783 000 10 kg bags and a 10.03% year-on-year decline from March 2024, reinforcing sustained consumption trends despite price fluctuations.

Sales at the FPMs

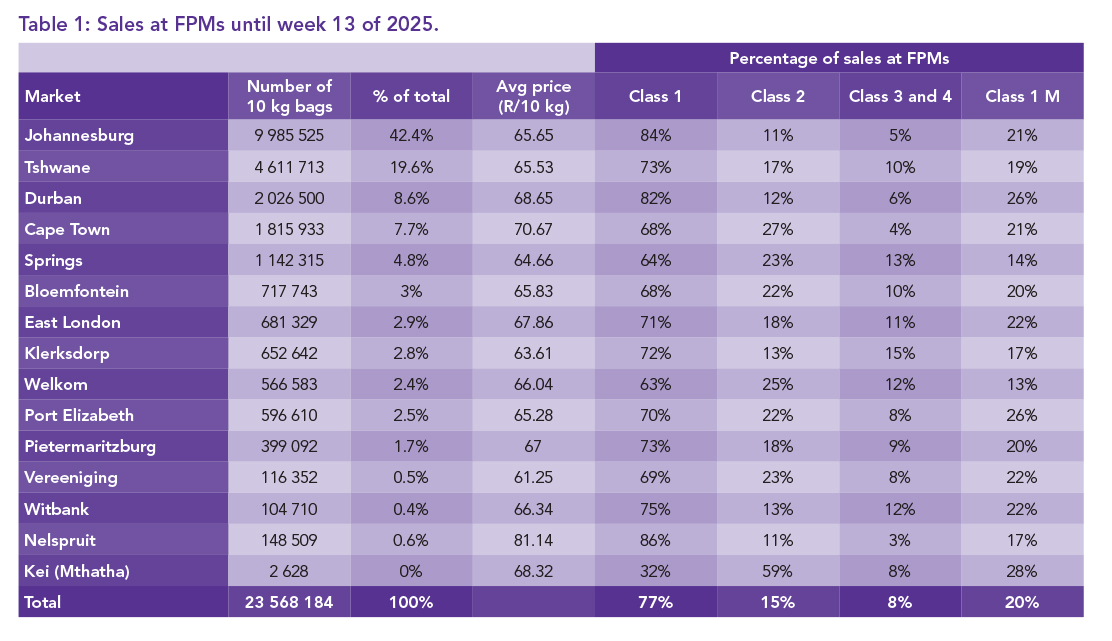

Table 1 outlines the number of bags sold at the various FPMs during the first 13 weeks of 2025. The five biggest markets during this period were collectively responsible for 83.1% of the country’s sales, showcasing their pivotal role in the potato supply chain. The average price per 10 kg bag across all classes and sizes is also reflected in Table 1.

In terms of the top average price per 10 kg bag received on the markets during the first 13 weeks, Nelspruit led with R81.14/10 kg bag followed by Cape Town with R70.67/10 kg bag, and Durban with R68.65/10 kg bag.

In terms of Class 1 (all sizes) sales, Durban, Johannesburg, and Nelspruit’s total sales consisted of 82, 84, and 86% bags, respectively – with Johannesburg being the highest of the top five markets.

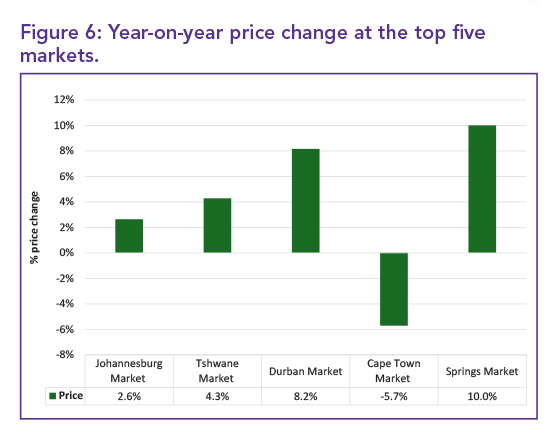

Figure 6 illustrates the year-on-year price change at the top five markets for the first 13 weeks of 2025, with all markets experiencing price appreciation except Cape Town. Springs’ price showed the greatest percentage increase with a price increase of 10%.

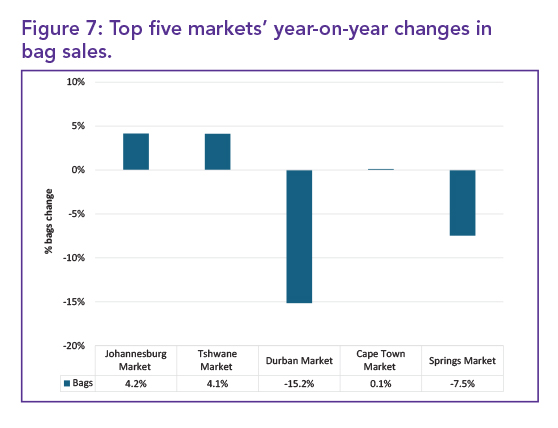

However, Figure 7 highlights a corresponding 7.5% year-on-year decline in sales volumes at this market. The volumes sold at the Johannesburg Market increased by 4.2% year-on-year.

Regional sales

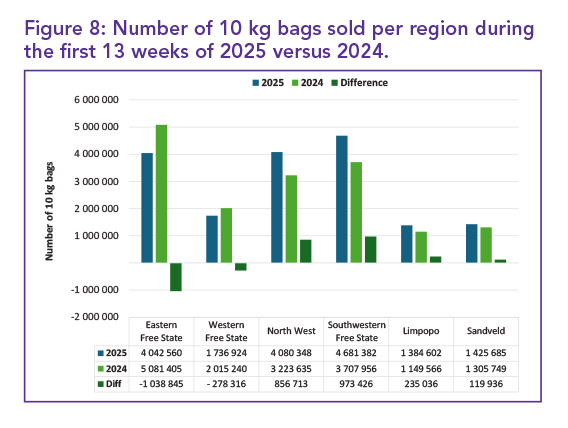

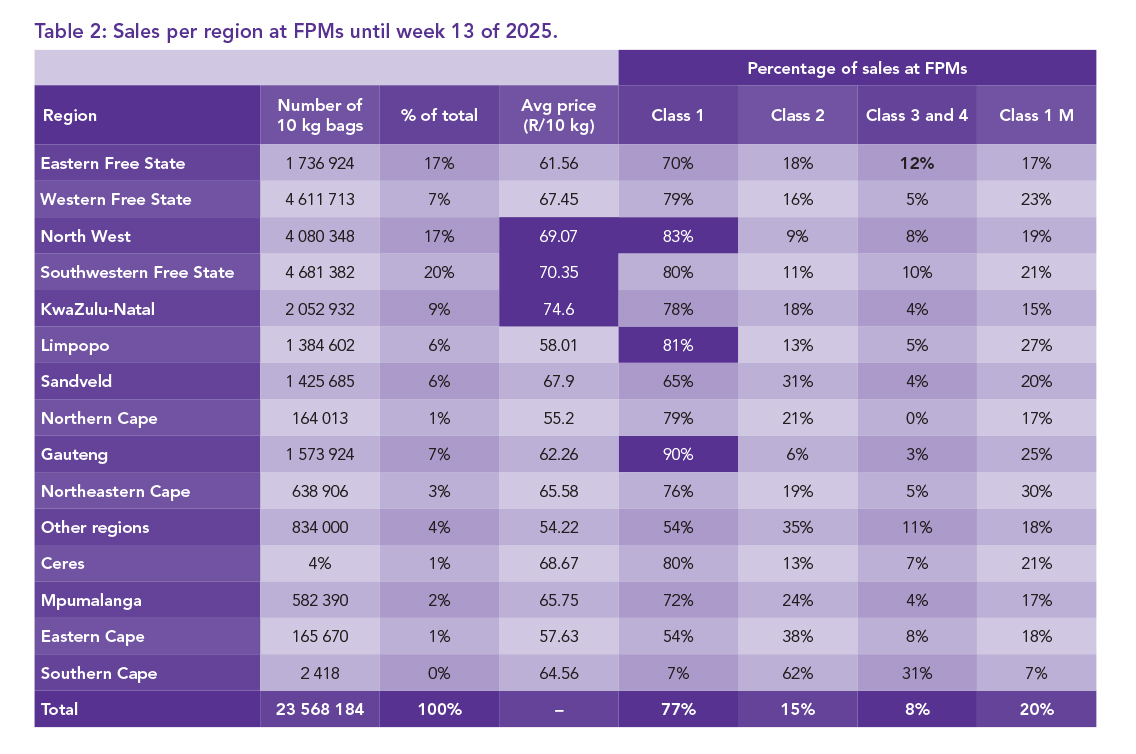

Figure 8 indicates sales performance at regional levels. The Eastern and Western Free State regions showed a decline in the first 13 weeks of the year. North West, the Southwestern Free State, Limpopo and the Sandveld regions recorded volume growth. The Eastern Free State, Southwestern Free State, Western Free State, North West, Limpopo and Sandveld collectively accounted for 74% of total national potato sales in the first 13 weeks of 2025, as summarised in Table 2.

The classification of potatoes also varies significantly by region, as shown in Table 2. Regions such as Gauteng and Northwest led in Class 1 sales, with 90 and 83% of their sales falling into this premium category, respectively. Overall, 12 of the 16 regions maintained a Class 1 sales ratio above 65%, reflecting consistent quality standards across much of the country. – Dikgetho Mokoena and Jodie Hattingh, Potatoes SA

For more information, email Dikgetho Mokoena at dikgetho@potatoes.co.za or Jodie Hattingh at jodie@potatoes.co.za.