Estimated reading time: 11 minutes

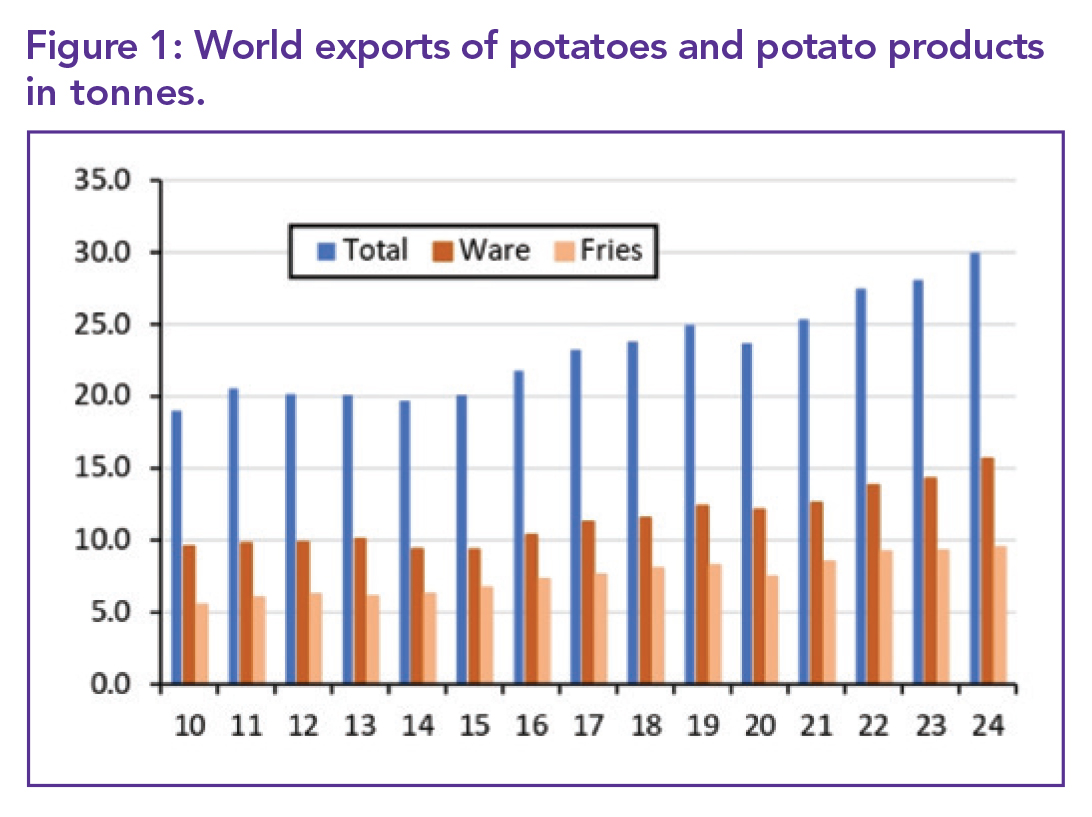

In 2024, the global potato industry experienced a historic peak in trade volumes and values. According to the latest figures, international potato and potato product exports totalled 29.96 million tonnes, reflecting a 6.6% increase from 2023. This equates to approximately 50 million tonnes of raw potatoes. Despite this volume growth, only 13.1% of global potato production was traded, underscoring the sector’s reliance on domestic consumption.

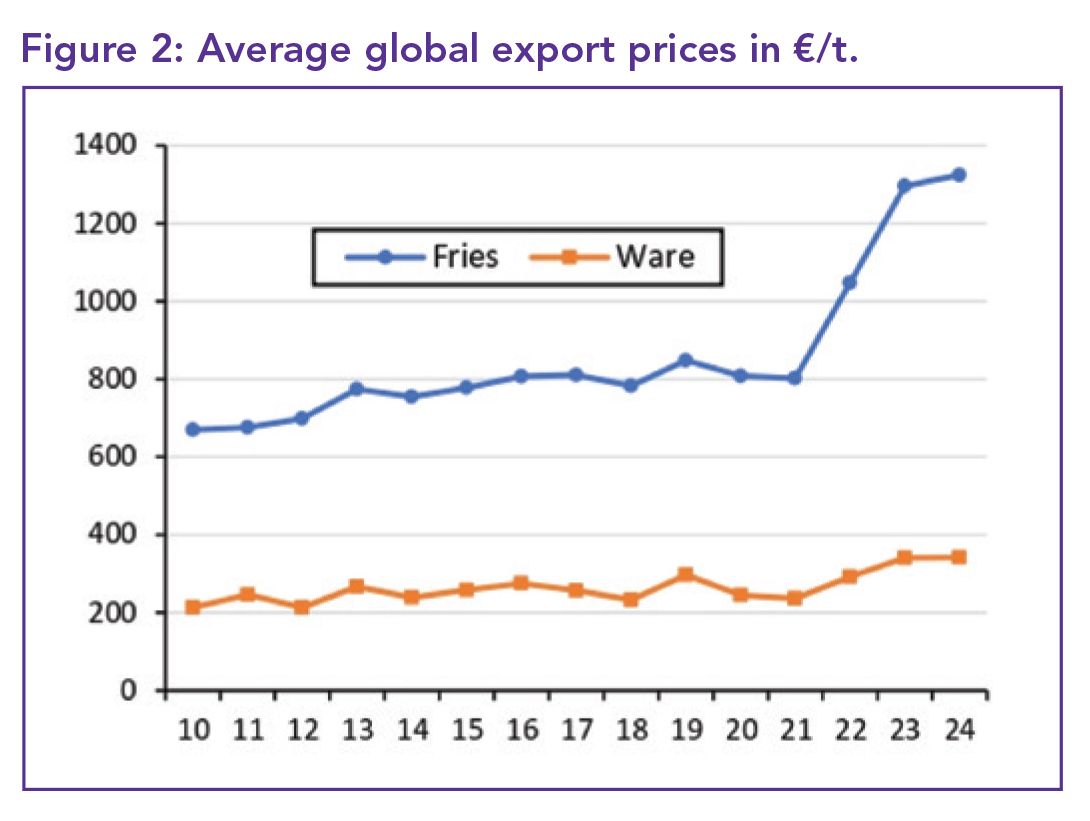

The total value of global potato exports reached an all-time high of €24.505 billion (US$26.524 billion), a 6.3% year-over-year (YOY) increase and a 131% rise compared to 2014. Frozen fries remained the most lucrative product category, representing over half of the total trade value at €12.63 billion. Ware potatoes were the leading export in volume terms at 15.66 million tonnes. Seed potato exports surged by 32% in value to €1.373 billion due to rising global demand and higher average prices.

However, trade prospects are clouded by emerging geopolitical tensions. The threat of new United States (US) tariffs, particularly under president Donald Trump’s administration, poses a significant risk to global supply chains and market stability. European and Canadian trades are showing early signs of a slowdown, suggesting 2024 may have been the high-water mark for potato exports.

United States

The US posted a US$925 million trade deficit in potatoes and related products for the year ending January 2025. While exports reached US$2.412 billion, imports soared to US$3.337 billion. Trump’s new tariff threats rattled markets. Canada, the most exposed partner (92% of its exports go to the US), is preparing retaliatory measures. European Union (EU) and Canadian fry exports have already seen early-year slowdowns, contrasting with US export growth of 22.3% in January alone.

The global potato market is facing heightened instability as geopolitical tensions between the US and China escalate. Trump’s newly announced 145% tariffs on Chinese exports – with reciprocal tariffs from China – are contributing to an already strained trading environment.

Although direct potato trade between the US and China is limited, the broader implications of a trade war are triggering ripple effects across the industry.

Signs of market disruption are becoming increasingly evident in major potato-producing and -exporting countries. Belgium’s processing usage is declining, with free-buy stocks at their second-highest level ever, suggesting weakened processor demand.

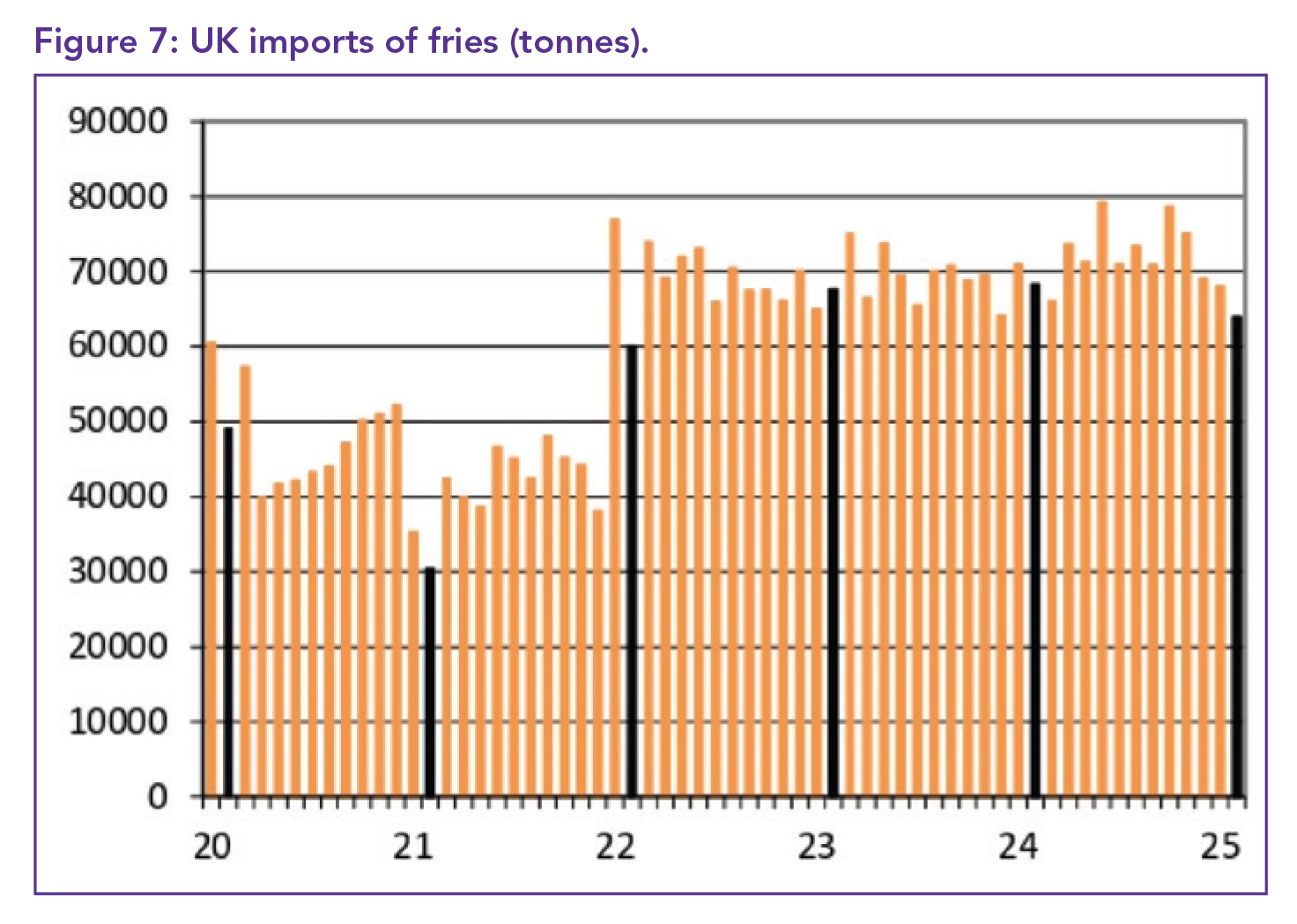

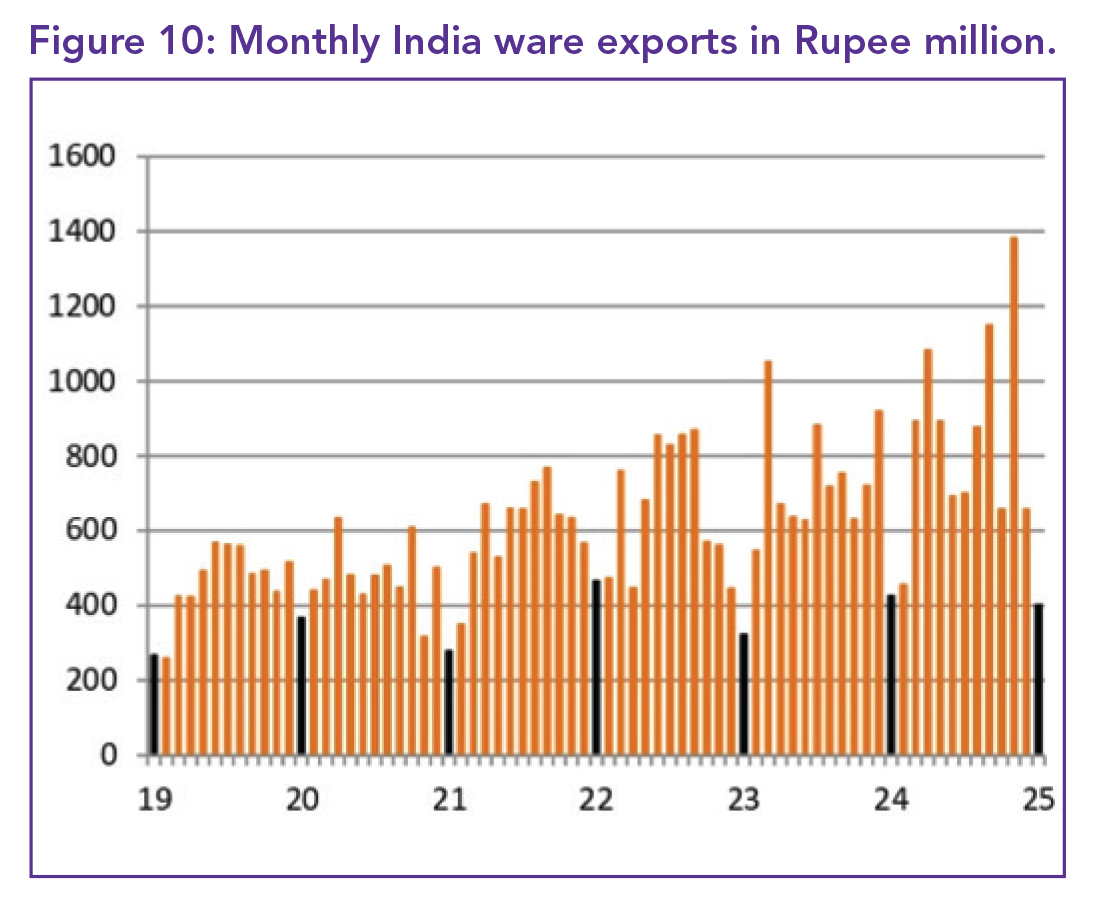

Meanwhile, United Kingdom (UK) imports of frozen fries dropped to their lowest level in three years, reflecting price fatigue among buyers. On a more optimistic note, India continues to thrive, recording another month of record fry exports.

Belgium

Belgium retained its crown as the world’s top potato exporter, although its total export value dipped slightly by 1.9% to €4.85 billion. This remains 88% higher than 2019 levels, affirming the country’s central role in the global market. Belgium’s competitive edge has been driven by some of the lowest processing potato prices in Europe, with Fontane and Challenger varieties averaging €167.50/t in the free-buy market.

The premium between contract and free-buy prices peaked at €78/t, the highest of the season. Demand from Eastern Europe and Spain remains robust, but transport logistics challenges, such as a shortage of available trucks, are hindering export growth. Despite dry weather enabling early planting, there are concerns about future water availability due to Belgium’s limited irrigation infrastructure.

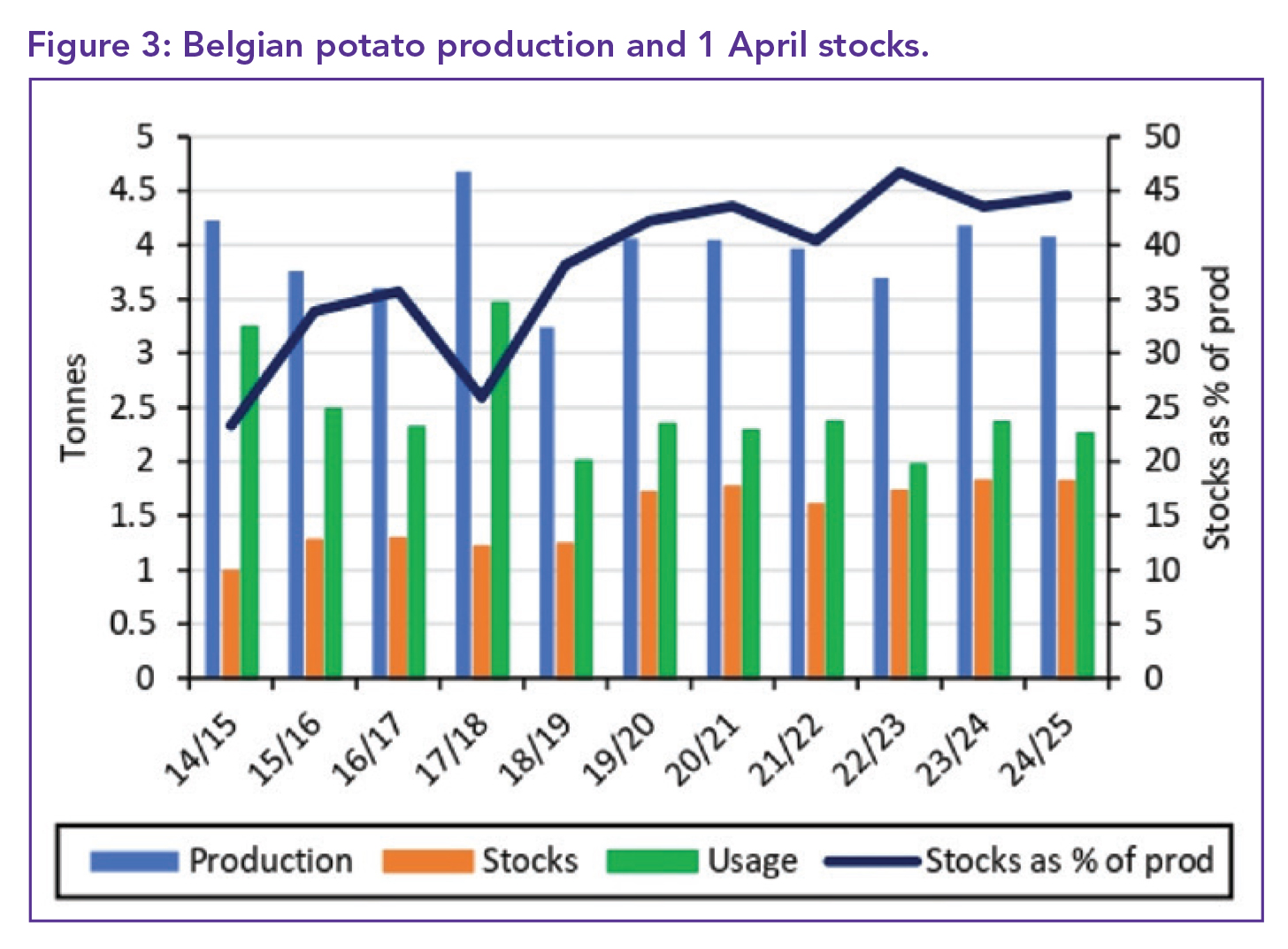

Belgium’s potato stocks stood at 1.818 million tonnes as of 1 April, just 0.2% below last year’s record. Free-buy stocks jumped 19.7% to 577 000 tonnes, the highest since 2013. Contracted stock usage is down, reflecting weak processing activity. Due to minimal trading, no official free-buy quotations were published by Belgapom or Fiwap, though a previous Fontane/Challenger price of €160/t was reported – well below contract averages. Imports surged 72% to help meet processing demand, especially from Belgium and the Netherlands.

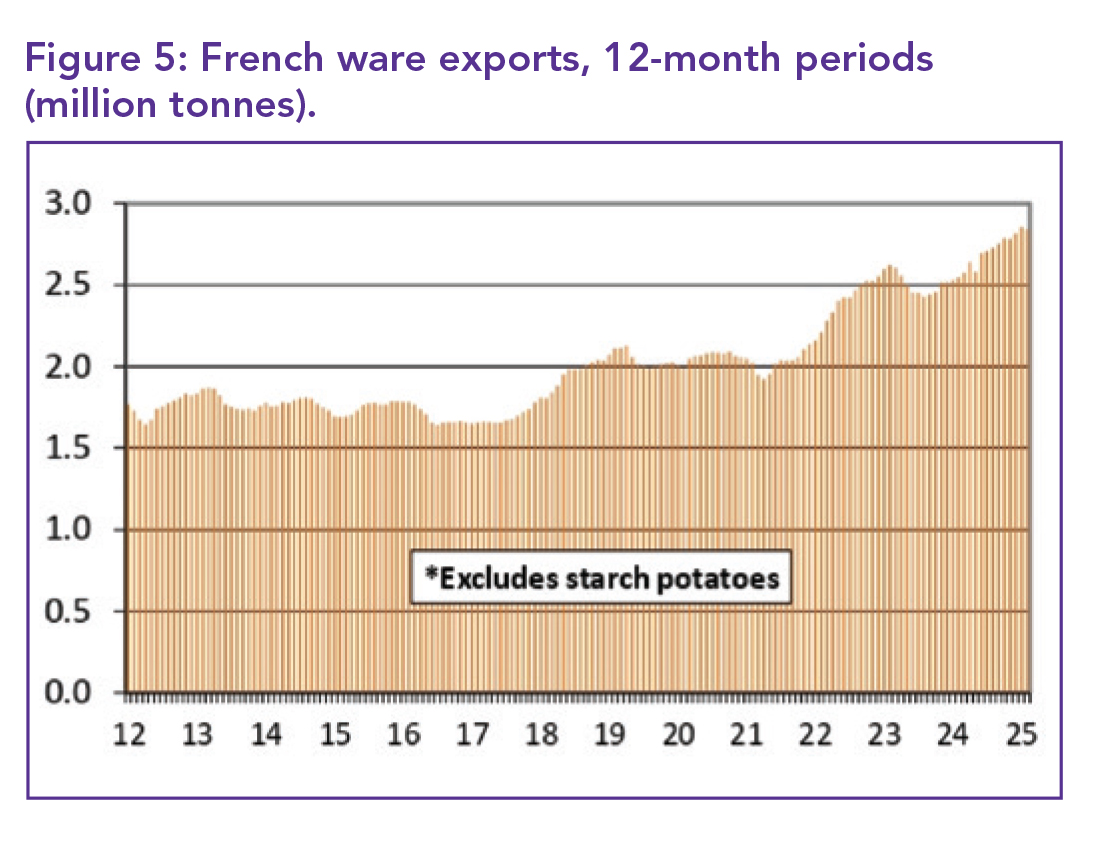

French seed potato exports rose 32.5% in volume and 8.9% in price. Retail performance was strong: sales were up 8.1% YOY in March, driven by hypermarkets and convenience stores.

Smaller packaging sizes (1 to 2 kg) and bulk purchases over 10 kg saw the highest growth.

Netherlands

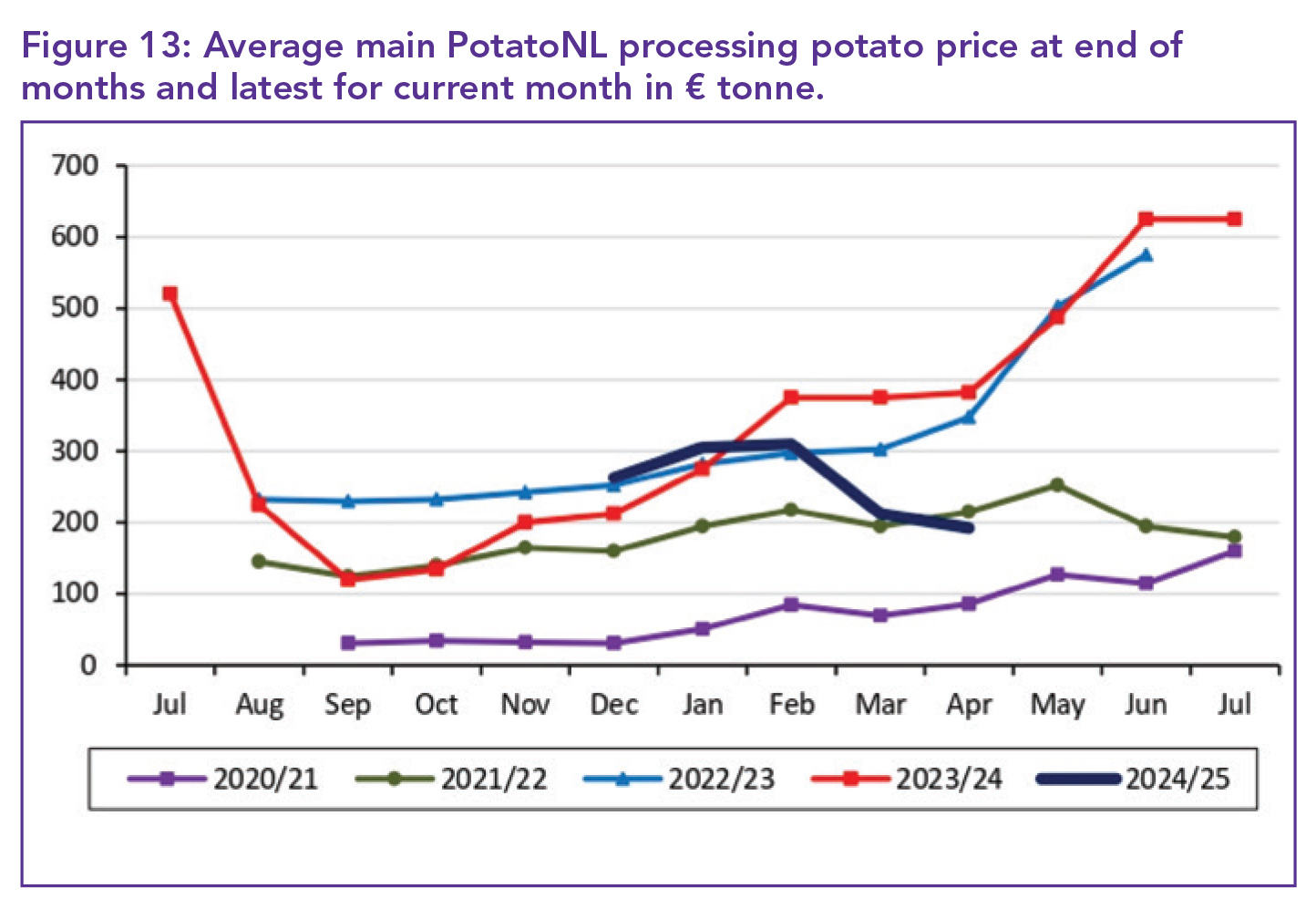

In the Netherlands, dry weather allowed for consistent planting but also contributed to softening market prices. The benchmark PotatoNL price for Category 1 potatoes held steady at €212.50/t, significantly lower than the previous year, while the reduction in price has improved the country’s export competitiveness.

Dutch farmers are concerned about the long-term impacts of continued dry conditions. Export demand remains steady, and seed potato shipments to Spain have increased, reflecting strong early-season demand.

France

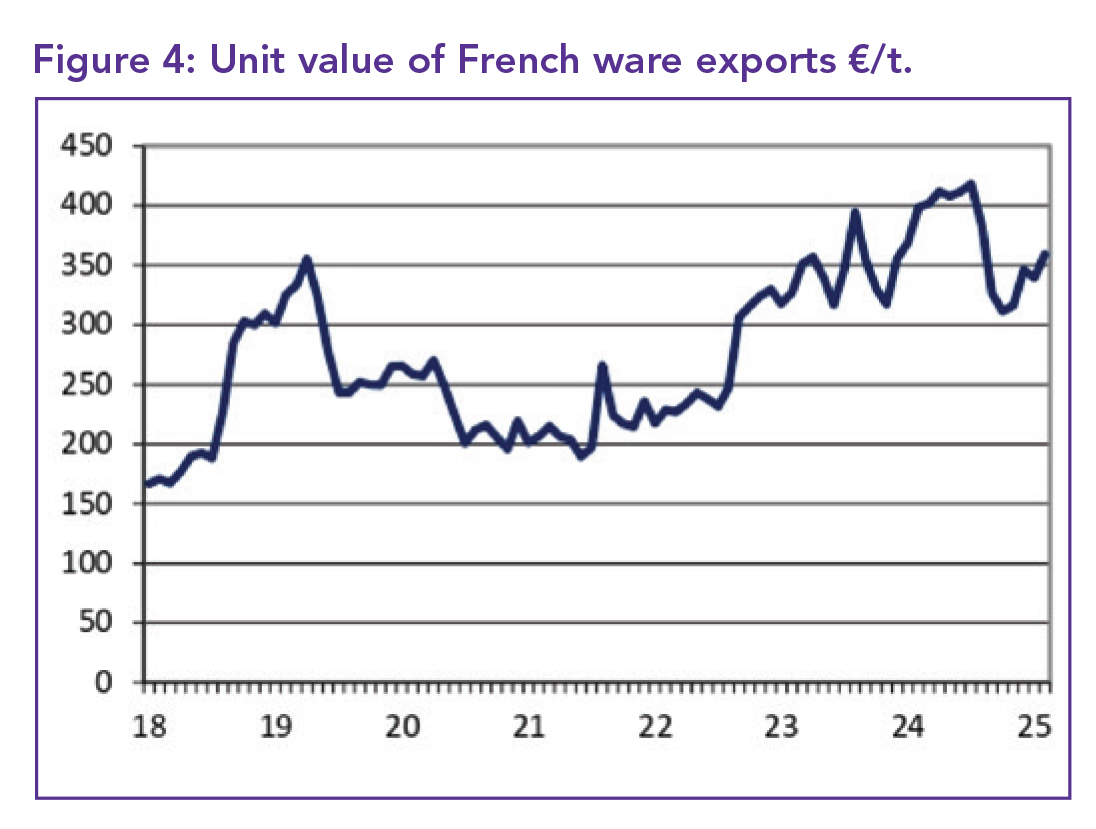

France saw significant price volatility in its potato export market. The benchmark RNM price for Category I Agata potatoes rose slightly to €360/t, but the overall range remained wide due to varying quality. Many lower-quality potatoes remain unsold, exerting downward pressure on prices. Processing prices have declined sharply to €160/t, a dramatic fall from previous years. Oversupply, combined with quality issues and lower export demand, has created a challenging environment for French growers. Eastern European buyers may provide some relief, but uncertainties persist.

France’s ware potato exports fell 4.7% in February, totalling 282 225 tonnes, but year-to-date volumes remain 11% higher YOY. Growth came from Spain (+4.1%), Portugal (+9.1%), and Germany (+31.9%), while exports to Belgium and Italy contracted.

Imports surged 72% to help meet processing demand, especially from Belgium and the Netherlands. French seed potato exports rose 32.5% in volume and 8.9% in price. Retail performance was strong: Sales were up 8.1% YOY in March, driven by hypermarkets and convenience stores. Smaller packaging sizes (1 to 2 kg) and bulk purchases over 10 kg saw the highest growth.

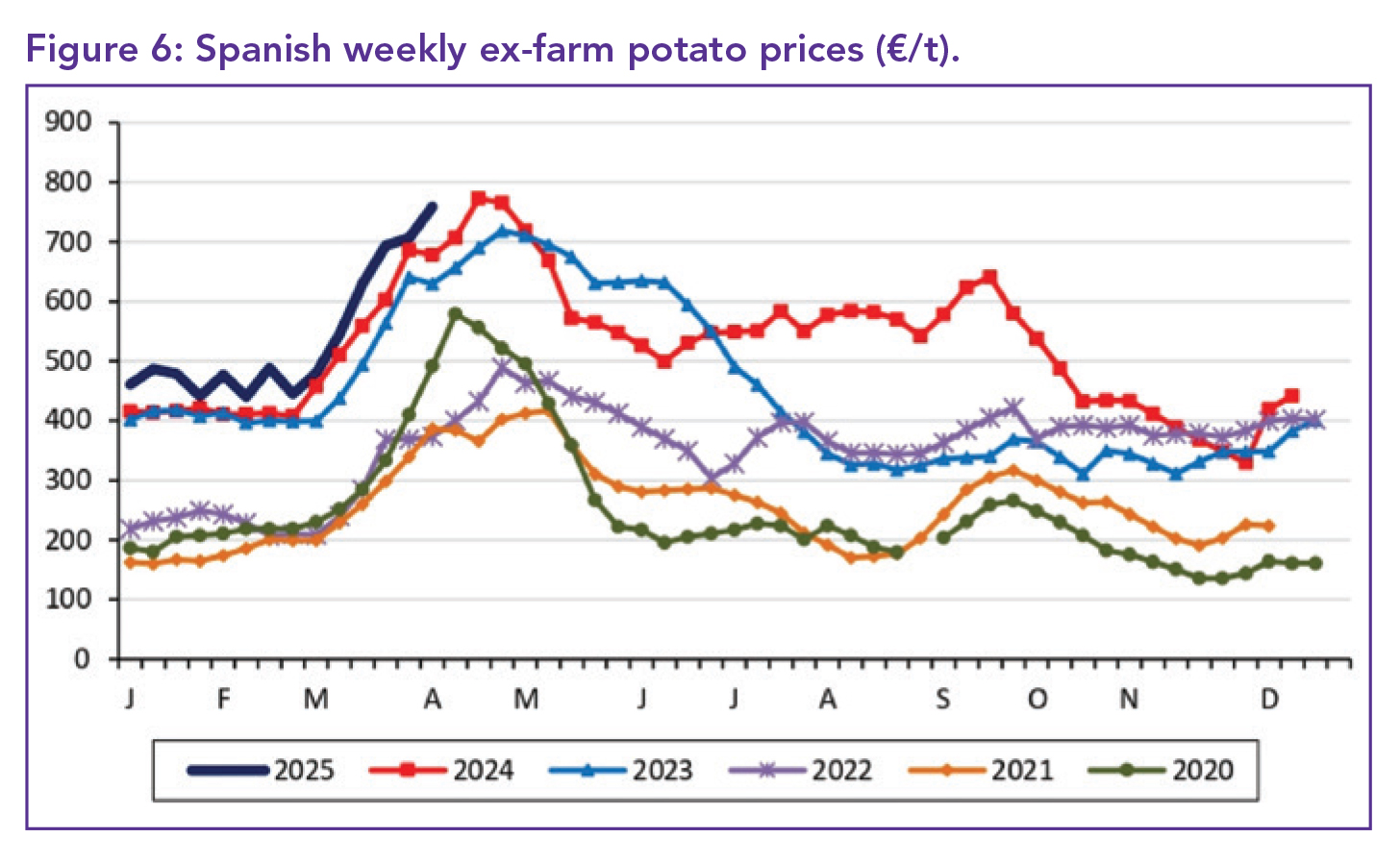

Spain

Spain’s early potato area grew by 3.3% to 15 742 ha. Extra-early potato cultivation increased by 4.5%, with yields holding steady at 25.3 t/ha. Major growth was reported in Galicia (+20%) and Comunidad Valenciana (+7.4%).

The increase in seed potato imports from the Netherlands and France signals high confidence among Spanish growers. However, recent heavy rains in the south have caused flooding and increased the risk of disease, especially in Cadiz and Jerez. Industry insiders are cautiously optimistic but await clearer assessments of crop damage.

As Spain begins its extra-early potato harvest, market activity has picked up, and prices are climbing in response to strong demand. Early season weather has been favourable in most regions, giving growers a good start and encouraging optimism for continued momentum. The expansion of early crop acreage and firm export interest from neighbouring EU markets are boosting early-season confidence.

Portugal

Portugal’s potato sector was heavily affected by adverse weather, as persistent rains resulted in 20 to 35% area losses across key regions such as Setúbal and Ribatejo. Plantings have been delayed, raising fears of a shortage in June followed by a glut in July. Ex-farm prices dropped to €350/t, down 12.5% from last year.

Disease risk has also increased due to warm and wet conditions, further complicating the harvest outlook.

Persistent rainfall across key potato-producing regions in Portugal has led to significant delays in planting. Fields remain waterlogged, preventing machinery access and putting producers behind schedule.

These delays are expected to shorten the growing season and potentially affect both the yield and timing of harvests. If conditions do not improve, Portugal may face a compressed harvesting window with implications for supply consistency.

United Kingdom

March brought exceptionally dry weather to the UK, with rainfall less than one-third of the monthly average. This facilitated early planting, particularly in southern regions, though cooler-than-average temperatures slowed crop emergence. Jersey potatoes are expected to hit the market within two weeks. Prices range from £280 to £350/t for top-quality potatoes. However, competition from lower-priced European imports is expected to intensify.

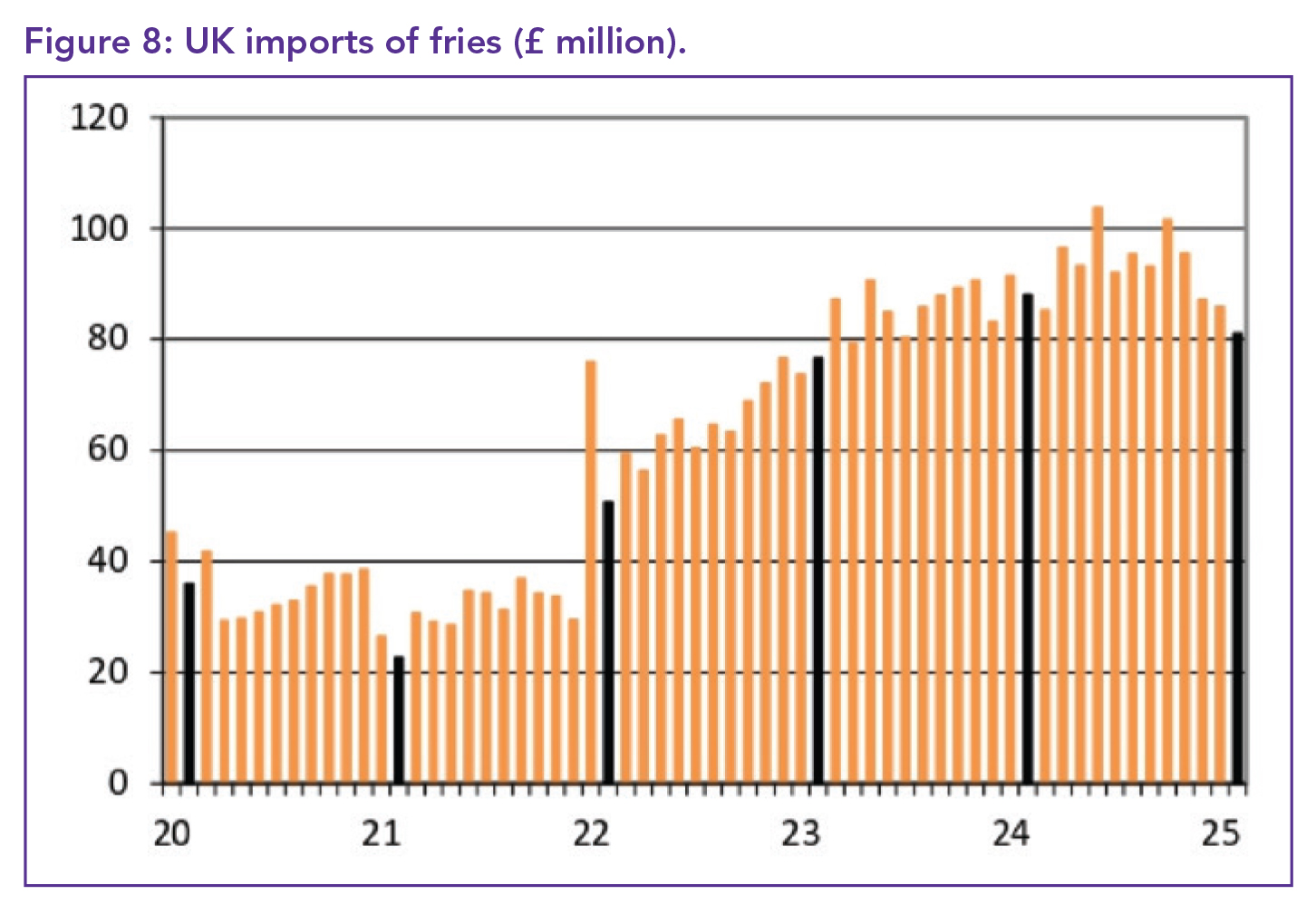

The UK imported 63 923 tonnes of frozen fries in February 2025, down 6.6% YOY – its lowest monthly level since early 2022. The average import price rose to £1 267/t, even though prices are slightly lower than a year ago. Overall, the UK’s annual import bill for processed potatoes reached £1.11 billion, 6.7% higher than in 2024.

Belgian and Dutch imports dropped significantly, while Germany and Austria gained market share by offering lower prices. Austria’s fries sold at £2 601/t, well above the market average, but still saw growth. Imports into Northern Ireland, classified as ‘unidentified’, fell 15.6%, although lower prices helped slow the decline.

Processed potato exports remained flat at 2 383 tonnes, with Ireland consuming 83% of that total. Annual export value fell 12.5% to £40.4 million. The UK’s second-largest buyer was the US, though their February imports halved compared to January.

Japan

Japan’s imports of frozen fries increased 29.8% YOY in February, reaching 31 507 tonnes. This marks the strongest February on record. The average import price fell to ¥266 798/t, improving affordability. Top suppliers included the US (19 141 tonnes), the Netherlands (3 347 tonnes), and Belgium (3 075 tonnes). The Netherlands has gained ground, expanding its annual share at the expense of Belgium. US sales were boosted despite ongoing trade tensions.

Thailand

Thailand’s fry imports plummeted in February 2025 to 3 647 tonnes, down 36.1% from last year. The decline followed disappointing tourist arrivals, particularly from China. An earthquake in Myanmar and domestic uncertainty surrounding gambling laws are expected to further reduce arrivals. India, once Thailand’s largest supplier, saw sales drop by 62.5%. China now leads imports, offering significantly cheaper products at Bht 35 633/t.

New Zealand

New Zealand’s total fry exports fell by 14.8% to 45 577 tonnes over the past year. Sales to Australia, its largest market, dropped sharply. However, sales to the Philippines (+66.6%), Indonesia (+229.9%), and Taiwan (+212.7%) rose, highlighting diversification efforts. Average export price rose to NZ$1 818/t, contributing to decreased demand from price-sensitive regions.

India

India’s fry exports in March reached 956 tonnes, up 116.3% YOY. Annual exports now stand at 7 549 tonnes, reflecting 107.4% YOY growth. The country has become a vital supplier to markets such as the Philippines and Taiwan, leveraging cost advantages and expanding production capacity.

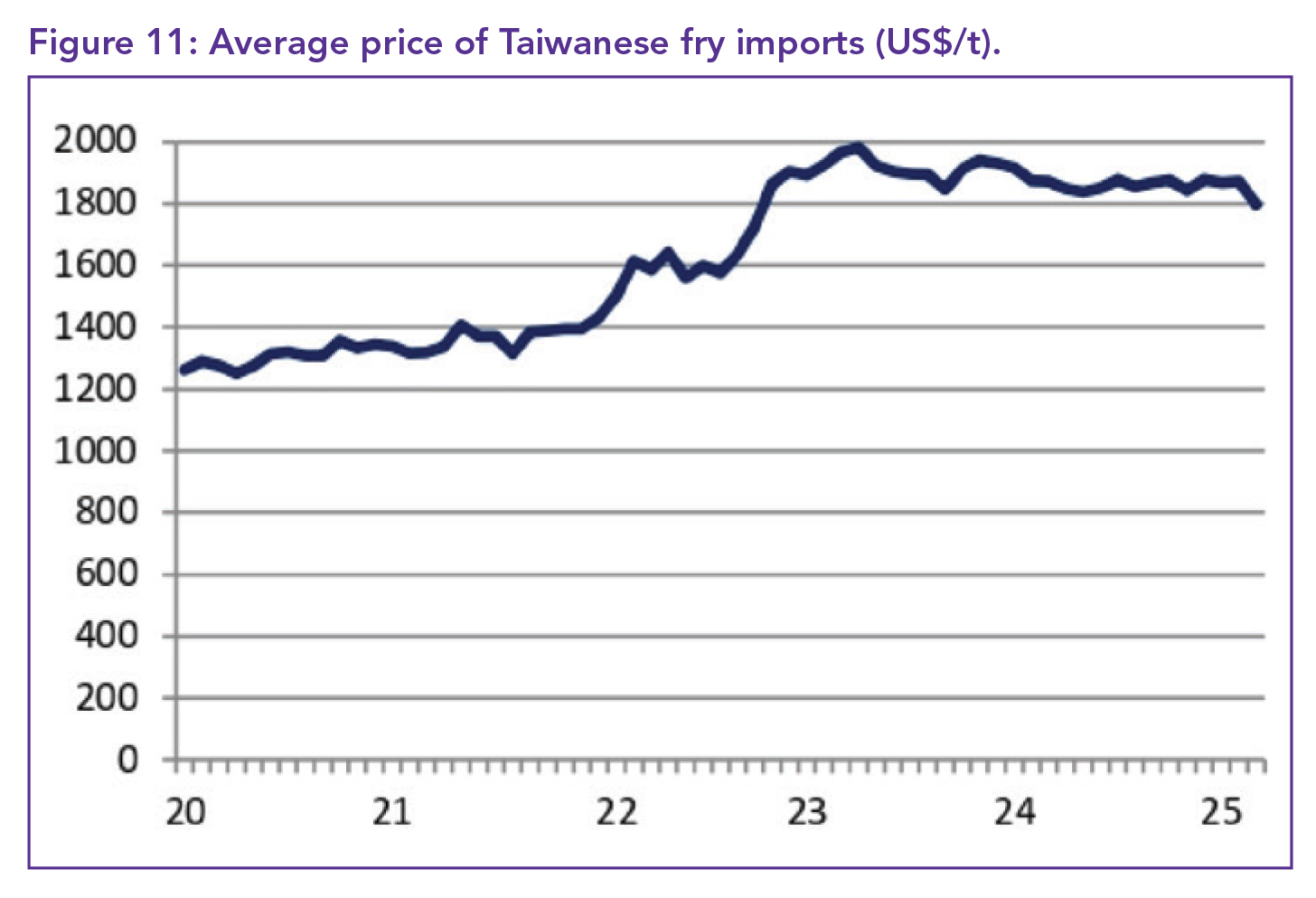

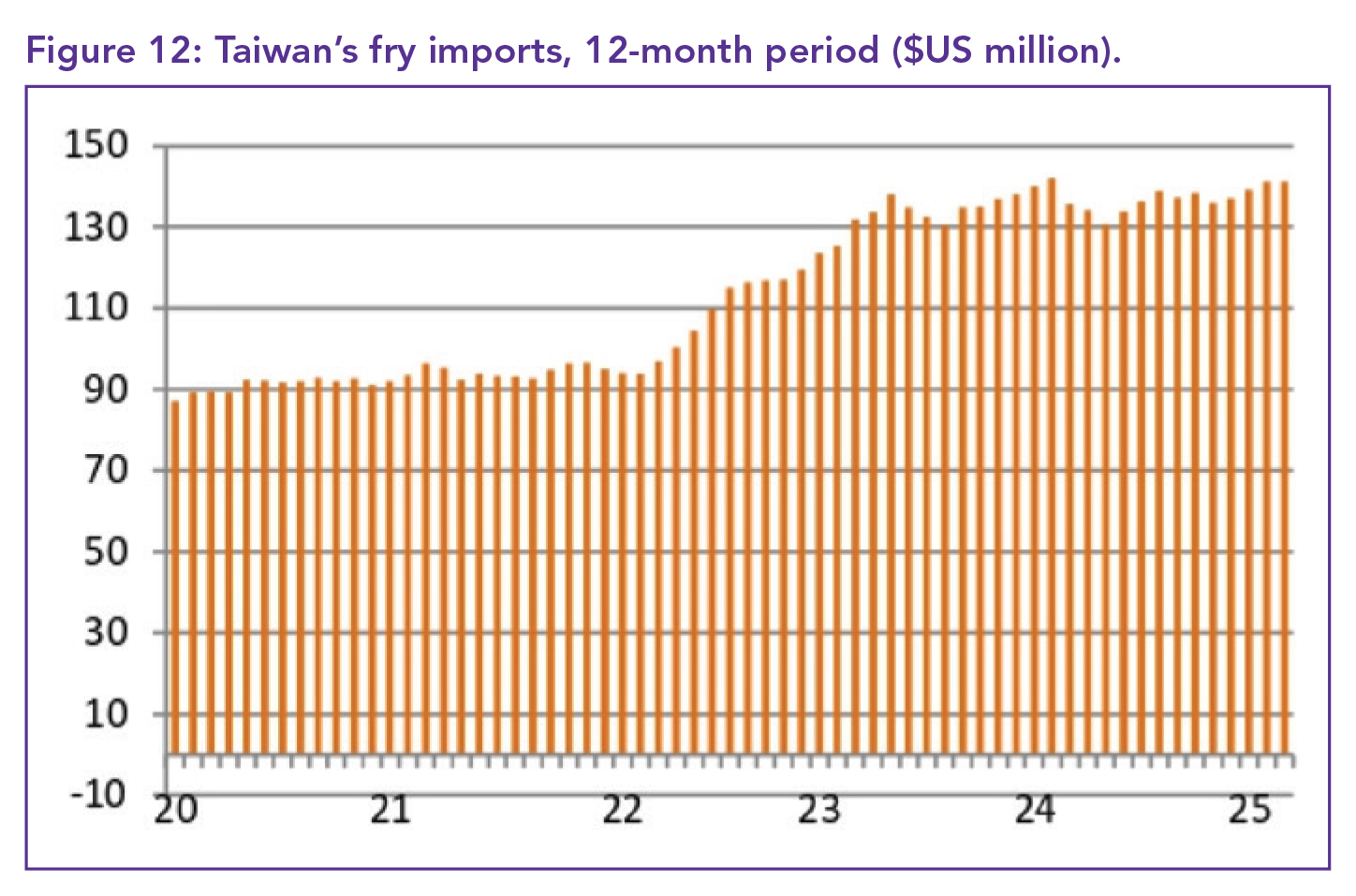

Taiwan

The Taiwanese import market showed a sharp shift as demand for US frozen fries declined, while Indian exports gained traction. India’s cost-efficient supply and rising reliability in logistics have allowed it to carve out a growing niche in the Taiwanese market, potentially reshaping regional sourcing dynamics.

Argentina

Argentina’s fry exports in February reached 1 552 tonnes, up 6.9% YOY. Prices dropped to US$1 556/t, 3.3% lower than last year, giving Argentina a strong pricing advantage. The country is well-positioned to benefit if a stronger US dollar materialises under future US policy shifts.

The Netherlands and Germany

In the Netherlands, over two-thirds of planting is complete. Rapid progress is pressuring prices, which fell to €192.50/t for Category I processing potatoes. Export prices range between €170 to €220/t. Germany experienced a boost in planting, now covering over 60% of acreage. Rain has helped ease drought concerns, with processing prices softening to €180/t, down from €195. – Francois Strauss, Potatoes SA

For more information, email the author at francois@potatoes.co.za or visit www.potatoes.co.za.