Estimated reading time: 13 minutes

The global potato market has entered one of its most unsettled periods in recent memory. While the crop performed well in many regions, the overall picture is dominated by oversupply, declining prices, rising production costs, and growing uncertainty among producers.

The pressure is evident across the United States (US), Europe, and Asia, and its impact even reaches South Africa. The imbalance between supply and demand has reshaped trade flows, disrupted contract negotiations, and strained profitability throughout the value chain.

North America

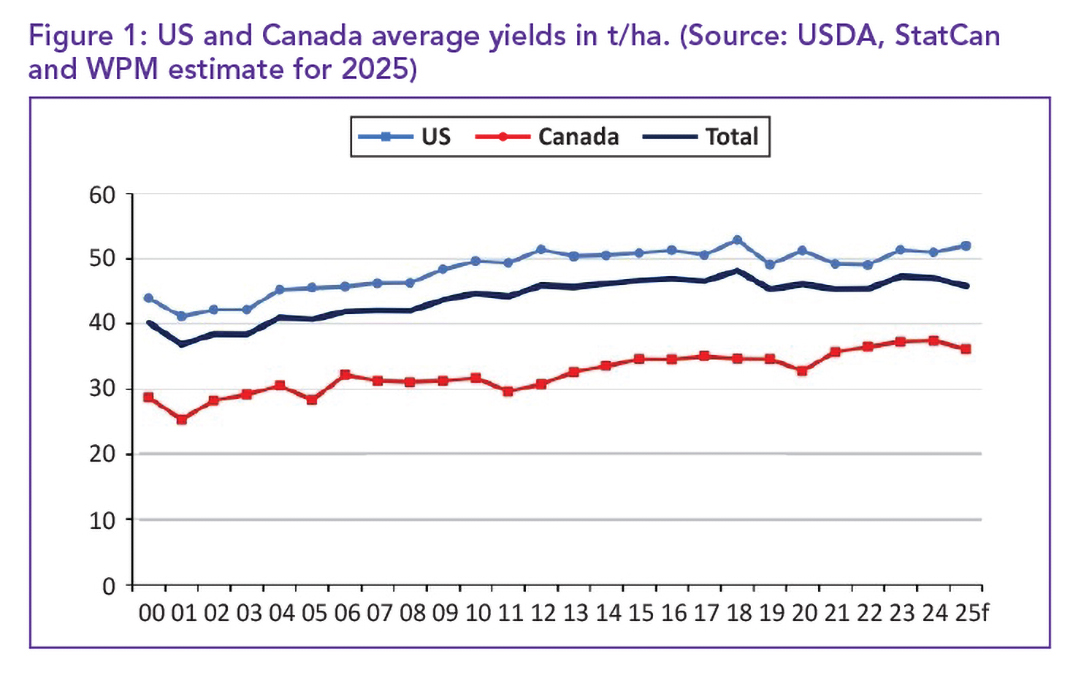

Across the US and Canada, potato production remained strong, with yields among the highest in recent years. The US harvested slightly less area than before, marking its smallest acreage of the century, yet still recorded yields of roughly 52 t/ha – the best recorded since 2018.

Canada’s harvested area grew modestly, though yields fell to around 36 t/ha following a challenging season in key producing regions.

The outcome was a US crop that was essentially unchanged from 2024.

The US held steady at just above 19 million tonnes, while Canada saw its output drop by nearly 3%. Some regions fared better than others: Idaho enjoyed strong yields after favourable weather, whereas Washington state’s production fell due to reduced plantings.

The continent’s processing sector is now well supplied with raw potatoes, and the abundance is expected to contribute to softer prices for frozen products, especially on the export market where the US is facing intense competition from Europe and Asia.

Canada

Despite generally favourable yields, Canada’s season was overshadowed by severe drought on Prince Edward Island, the country’s most important producing province. Some growers reported yield losses of up to 25%. Although the national crop figures appear stable, the regional impact has been significant, tightening supplies in certain markets and complicating the logistics of domestic movement.

United States

The US government shutdown has created further complications for growers. With US Department of Agriculture services suspended, producers have struggled to access emergency payments and routine support programmes just as market conditions have become more volatile.

Funding interruptions for the Supplemental Nutrition Assistance Programme (SNAP), America’s largest food assistance programme, have heightened concern, especially since potatoes remain the most-purchased vegetable among SNAP households.

Agricultural leaders have warned that the prolonged disruption threatens not only producer livelihoods but also the broader rural economy and the country’s long-term food security.

Europe

Europe is currently the heart of the global oversupply problem. Exceptional yields across nearly all major producing countries have collided with weakened consumer demand and rising storage costs, pushing prices sharply downward.

France

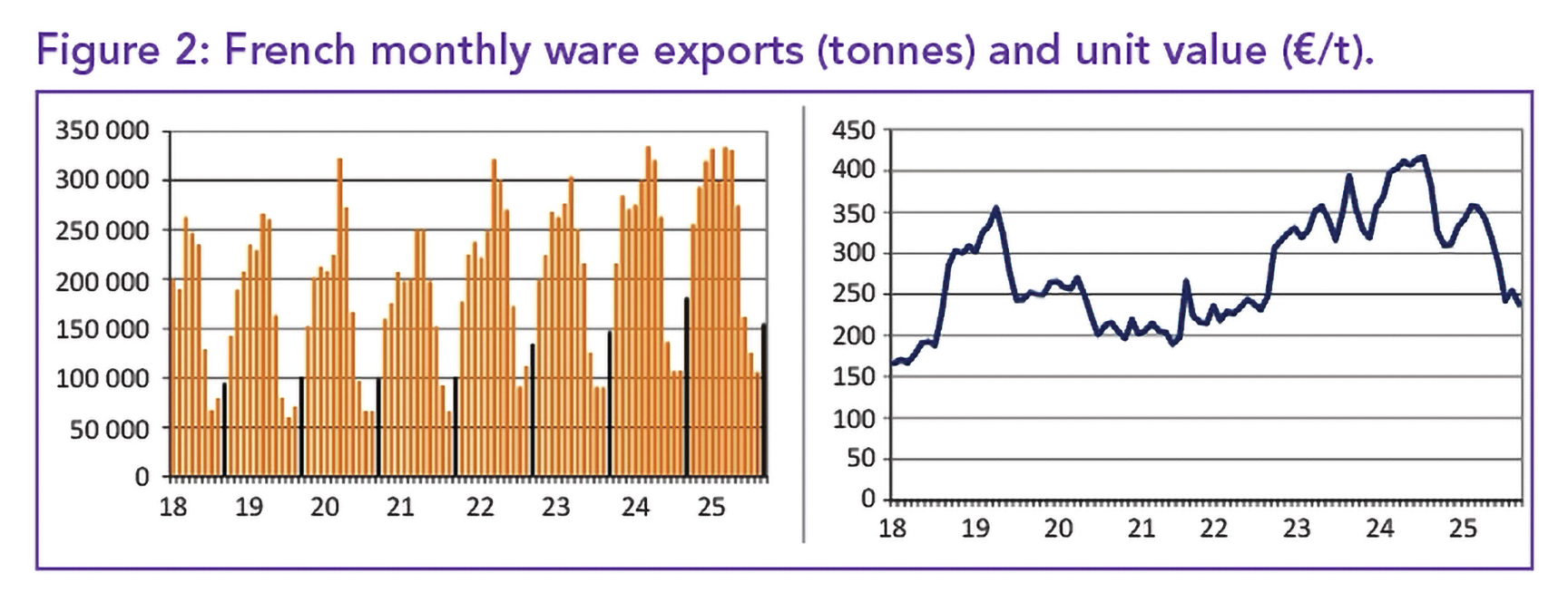

French retail potato sales softened slightly through September and early October, although prices dropped considerably compared with 2024.

Discount retailers performed strongly, while hypermarkets and online platforms recorded notable declines. Retail prices averaging just over €1.15/kg – almost a fifth lower than last year – were not enough to stimulate a broad rise in demand.

France enters the season with one of its largest crops in recent years, yet this has coincided with abundant supply across Europe. As a result, French exporters are facing strong competitive pressure in neighbouring markets. September ware exports fell nearly 15% year-on-year (YoY), with Spain and Belgium purchasing substantially less French product. Even premium quality lots have struggled to achieve strong prices, reflecting the oversupply across the continent.

Quality consistency has become essential, as buyers can select from abundant supply. Transport availability has improved, yet elevated fuel prices continue to compress margins. French processors are operating at high capacity: October utilisation neared 179 000 t, contributing to a record 666 000 t processed in the first three months of the season. More than 70% of this volume is contracted, leaving limited room for free-buy uptake.

Belgium

Belgium is experiencing a growing divide between contracted and free-buy potatoes. Contract prices recently rose to around €190/t, while free-buy potatoes have hovered near €15/t for several consecutive weeks, one of the widest gaps seen in years.

This disparity reflects the intense pressure on open-market trading amid heavy supply.

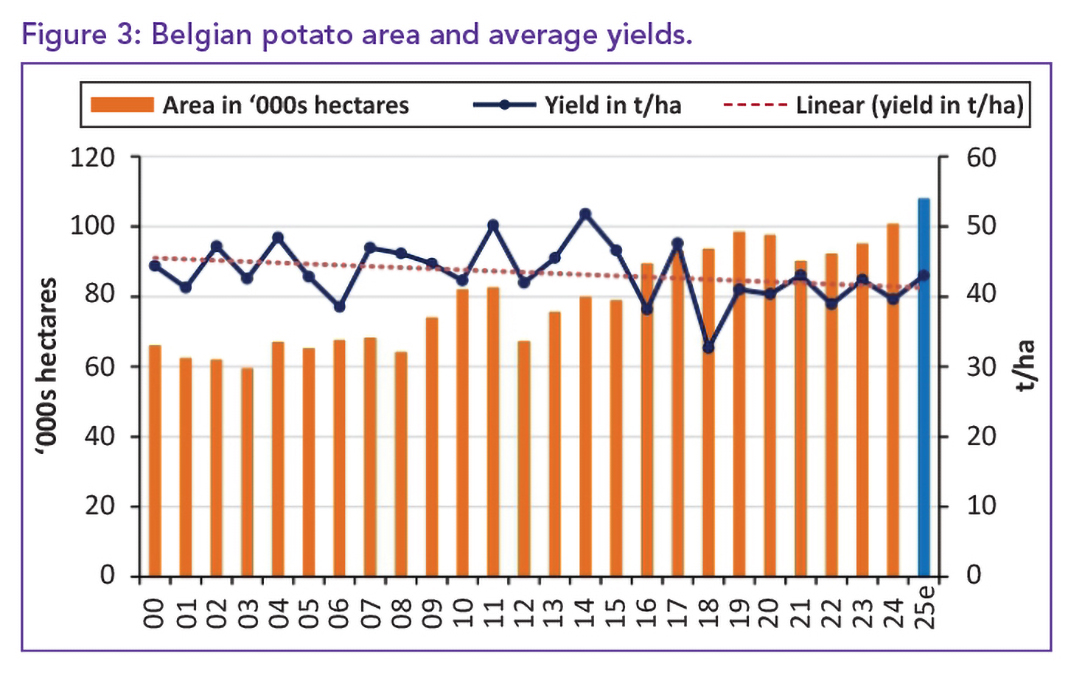

Belgium harvested a record 4.63 million tonnes of potatoes; an impressive result despite falling short of early industry expectations. The increase was driven by a 7.2% expansion in planted area, setting a new national record.

Early potato volumes rose sharply as growers anticipated favourable early-season pricing. However, these expectations did not materialise, resulting in significant financial losses as free-buy prices remained depressed.

Average yields climbed to 43 t/ha, supported by favourable late-season weather. Still, long-term yield trends indicate increased climate variability, with greater fluctuations than those recorded in earlier decades. Belgian processors are struggling to absorb the large crop, contributing to soft free-buy prices and reducing the flexibility within standard contracts.

Germany

Germany’s large harvest has placed significant downward pressure on prices. Processing potatoes frequently sold for far less than in 2024, with the average price more than €100/t below the 2024 season.

Retail potato prices have also fallen, with firm-fleshed and floury varieties trading nearly 40% below year-earlier levels. The situation resembles the pandemic period, when restaurant closures weakened demand for processed potato products.

The Netherlands

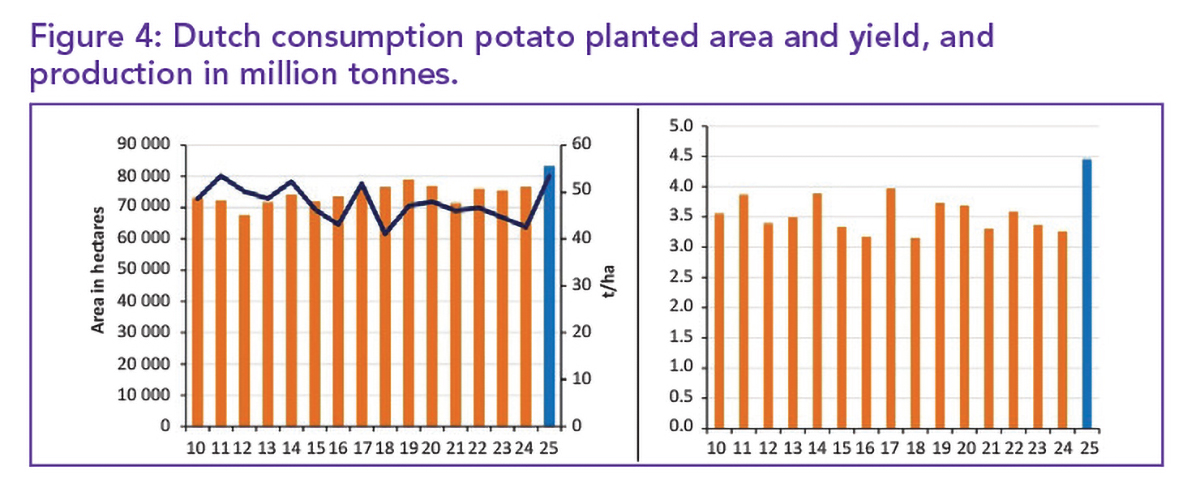

The Netherlands produced its largest potato crop in 25 years, with total production reaching nearly eight million tonnes. Yields climbed to record highs, particularly in the consumption potato category, where they exceeded 50 t/ha.

Despite strong export interest, prices have shown little improvement. Early-season quotations have hovered around €28/t, a fraction of prices seen one or two years ago. The market is saturated, and the abundant supply continues to limit recovery.

With the 2025 crop largely marketed or in storage, Dutch growers are turning their attention to the 2026 season. Many expect processors to reduce contract prices due to 2025’s oversupply, prompting some to consider shifting land into cereals or onions. Seed availability is high following a 5.8% increase in seed potato acreage. At recent seed days, breeders acknowledged the need for price corrections from last year’s elevated levels.

Poland

Poland is facing a similar situation, with heavy domestic supplies and limited processing demand driving prices downward. Wholesale prices for early-season potatoes fell to around €0.20 to €0.30/kg, and by late October, many varieties traded for even less. Retail chains paid roughly a quarter of a euro per kilogram – more than 20% below 2025 – yet demand has remained flat.

Spain

Growers in Xinzo de Limia endured a particularly difficult season marked by extreme weather. Heavy rains delayed planting, and prolonged heatwaves reduced tuber formation and size. Although some fields achieved yields above 50 t/ha, most saw substantial losses, with overall output expected to be 30% lower than 2024.

Market prices have not compensated for these challenges, and growers continue to face rising input costs. Spain’s increasing reliance on imported potatoes, up 8% YoY, highlights ongoing supply-demand imbalances in the domestic market.

Portugal

Severe storms in November brought exceptional rainfall and more than 47 000 lightning strikes, devastating potato fields in the Setúbal Peninsula. Flooded fields and heightened disease pressure could reduce yields by up to 40% in the most affected areas.

Growers also report significantly higher production costs due to repeated fungicide applications and field repairs. Despite broader European oversupply, Portuguese ex-farm prices for new potatoes surged to €450/t due to the abrupt tightening of local supply.

United Kingdom

Producers in the United Kingdom (UK) have been particularly vocal about growing pressures. A nationwide survey supported by McCain found that only about 12% of UK producers feel optimistic about their future.

Rising production costs have taken a heavy toll, and more than half of respondents have considered leaving agriculture entirely.

Since Brexit, the UK has overhauled its agricultural support system, phasing out traditional direct payments and introducing new environmental programmes, although these have faced temporary freezes due to oversubscription. Proposed inheritance tax changes have triggered further concern across the sector.

To survive, many producers have turned to diversification, adopting renewable energy systems, conservation projects, agritourism, or direct-to-consumer models. Although UK potato prices remain higher than those in continental Europe, growers are rapidly selling stock out of concern that prices will fall further as the season progresses.

UK potato production costs rose 4.8% in the year to September, more than any other major arable crop and driven primarily by increases in fertiliser and contractor prices. Labour availability remains a concern for many growers. Retail potato prices, however, have dipped slightly, further pushing margins. Wet autumn weather has slowed lifting in some regions while simultaneously replenishing water reserves. Maris Piper continues to trade around £160/t, with bagged chipping potatoes fetching around £140/t.

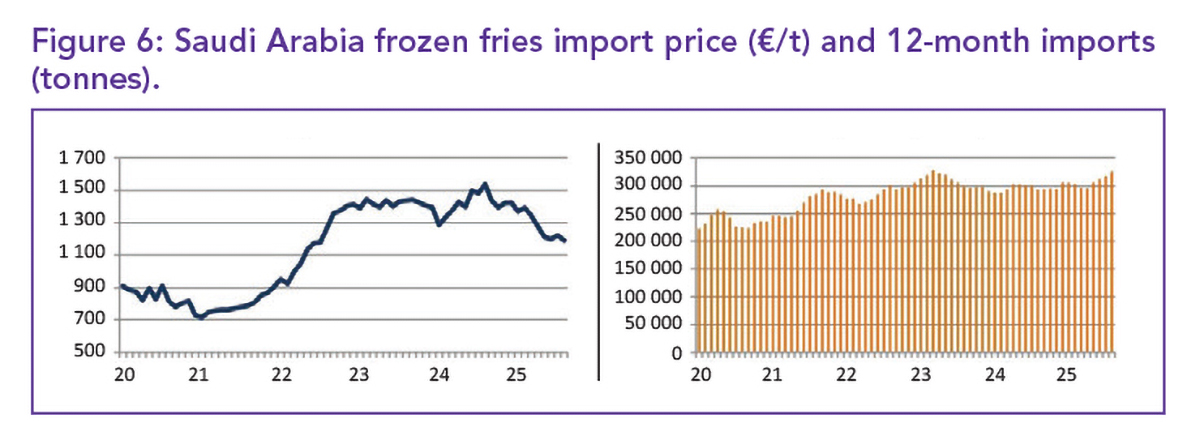

Saudi Arabia

Overall fry imports into Saudi Arabia declined in August, but France gained market share by cutting prices to €1 030/t, outperforming both Dutch and Belgian suppliers. India, China, and Egypt continue to offer the lowest-priced alternatives, reshaping the Kingdom’s sourcing patterns. Fresh potato imports continue to fall as domestic production expands.

Philippines

India and China raised fry prices in September, reducing total imports by nearly 4 000 t. Despite this monthly softening, both countries remain dominant in the Filipino market. US fries continue to lose market share due to significantly higher prices. Australia has overtaken New Zealand in monthly supply, gaining momentum in the region.

Indonesia

Indonesia’s fry imports reached 8 148 t in September, pushing annual totals above 90 000 t. China and India now control roughly 60% of the market due to their competitive pricing. Fresh potato imports rose 54% YoY, driven by increased shipments from India and Germany. Demand continues to expand in both retail and food service.

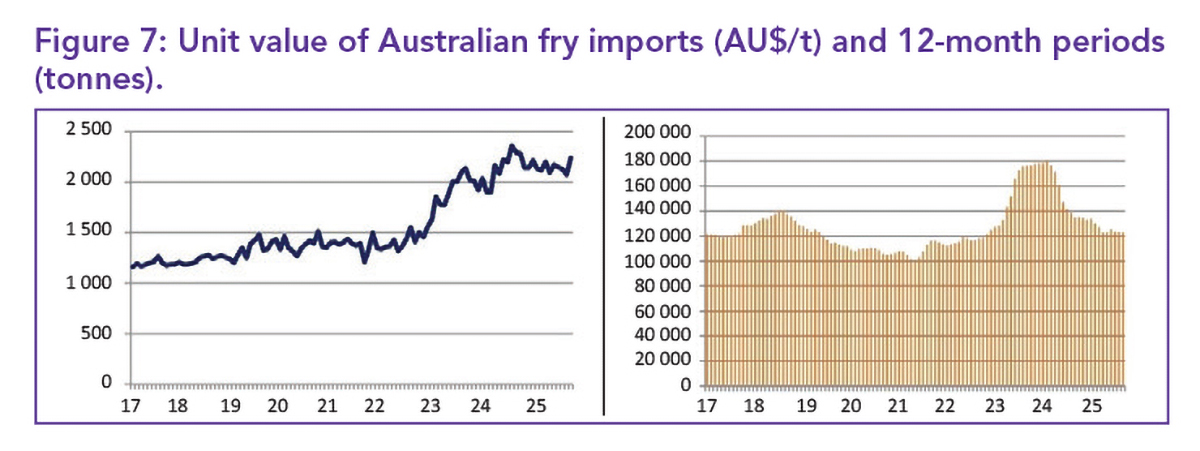

Australia

Australian fry imports fell 4.3% YoY in September. Dutch shipments nearly halved compared with the previous month, while Belgian and New Zealand imports show long-term declines. China recorded a stronger month, though annual volumes remain comparatively low.

Domestic supply remains tight due to ongoing restrictions on Tasmanian potato movements linked to mop-top virus. South Australia has become increasingly important in meeting national demand. Australian fry exports continue their strong growth trajectory, rising 60% YoY.

Turkey

Turkey’s frozen fry sector has suffered a significant setback. Export volumes have fallen sharply, notably following a collapse in Russian purchases. Russia, once the dominant buyer of Turkish frozen chips, has been reducing imports dramatically as it invests in expanding its domestic processing industry. As a result, Turkey’s export volumes dropped by more than half in September, and annual export revenues have fallen by more than €50 million compared with two years ago.

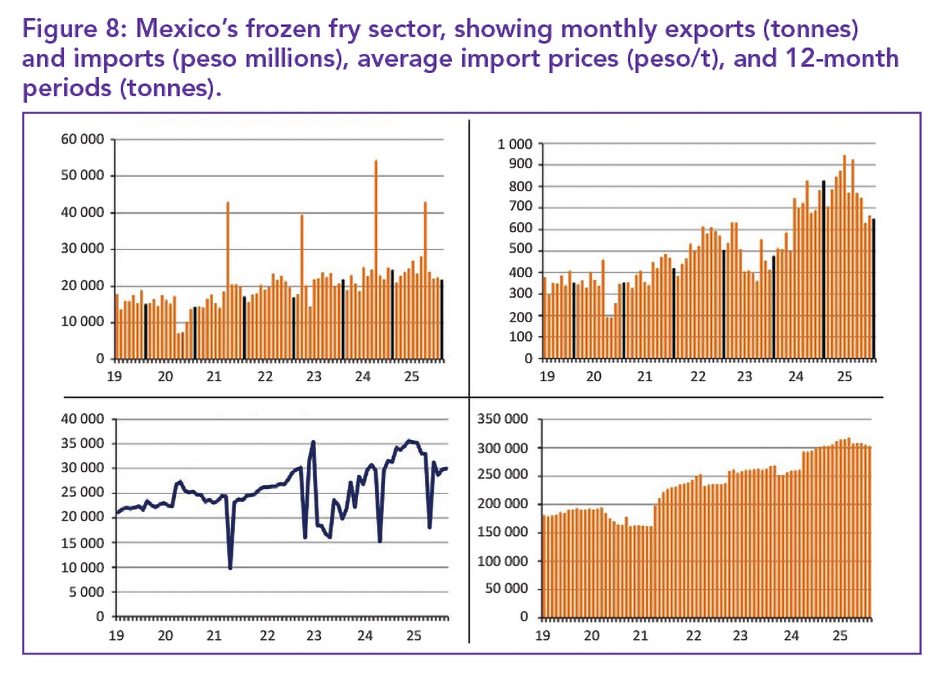

Mexico

Hong Kong and Singapore

Hong Kong’s import volumes surged to more than 4 000 t in August after China and the US reduced prices, but imports returned to normal levels in September. Chinese suppliers strengthened their market position during the temporary price war. Singapore, meanwhile, saw a decline in processed potato imports as average import prices rose for the second consecutive month. The market remains highly price-sensitive, and even small increases can lead to sizeable reductions in import volumes.

South-East Asia

In South-East Asia, both China and India have engaged in aggressive pricing strategies to expand their presence in frozen fry markets. Despite reducing prices, Chinese volumes dropped by around 100 t, while India saw an even sharper decline, losing more than half its sales YoY. The region’s competitive landscape continues to shift as both countries vie for dominance.

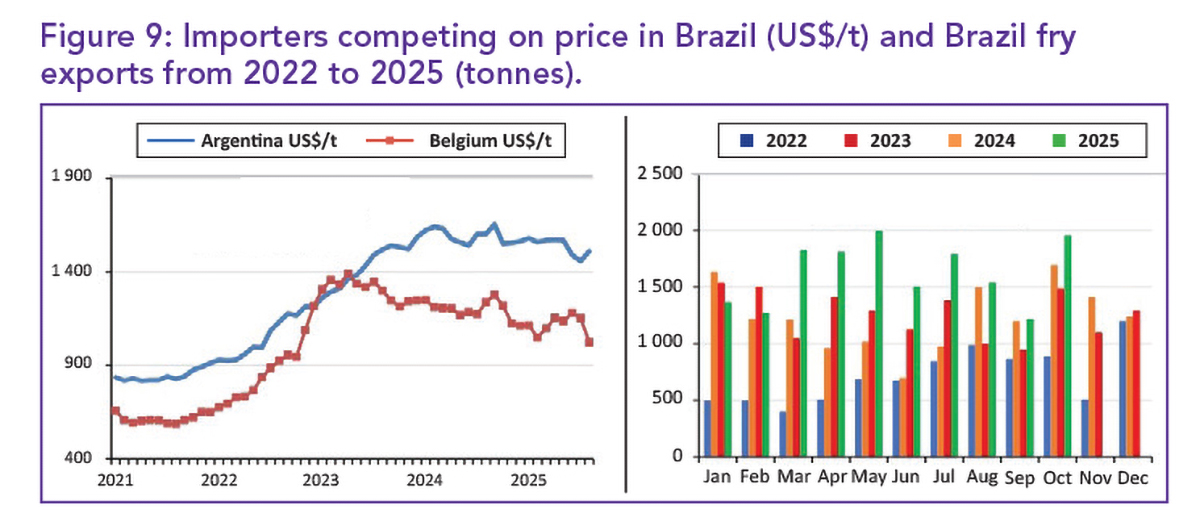

Brazil

Processed potato imports fell by more than 3 000 t in October. Even after multiple price reductions, Belgian fries lost further market share. Argentina increased sales despite higher prices and now holds a 45% market share. China supplies the lowest-cost fries in the Brazilian market, while Egypt and the Netherlands keep steady positions.

Brazil’s own processed potato exports rose 32% YoY, supported by growing demand across Latin America. McCain’s BRL 1.8 billion expansion of its Araxá plant reinforces Brazil’s emerging role as a regional processing hub.

South Africa

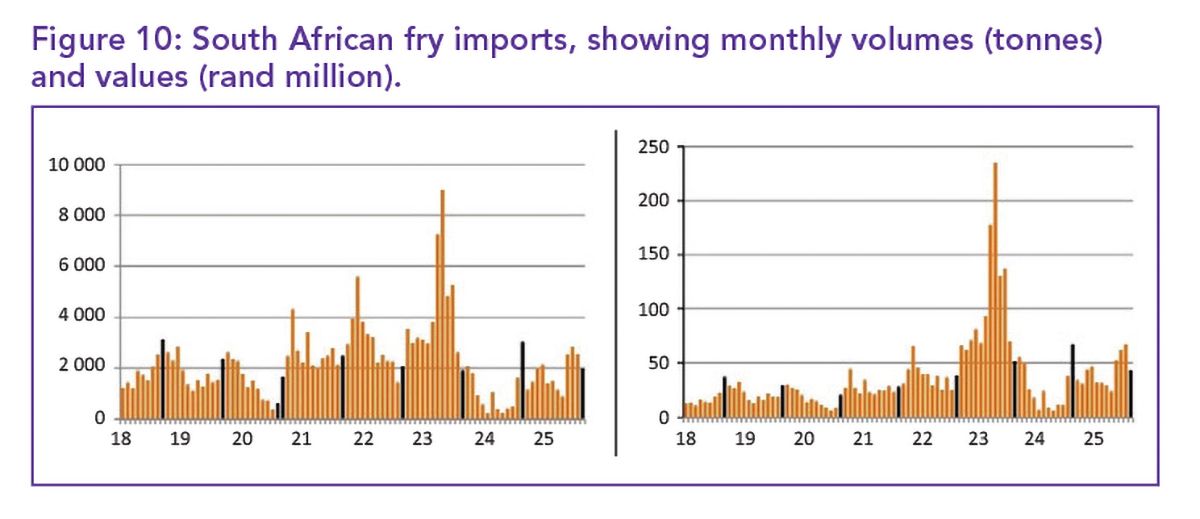

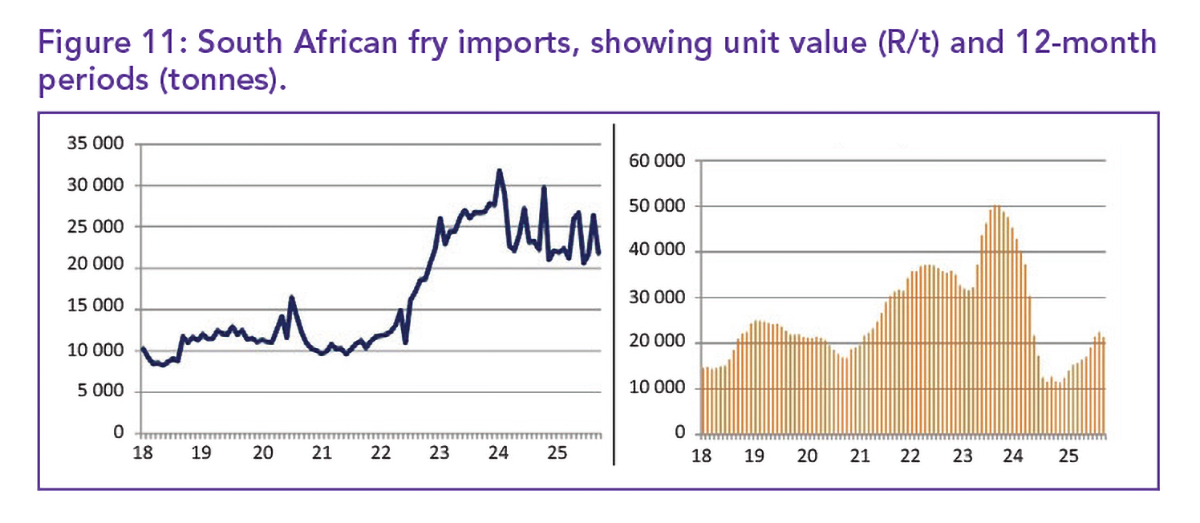

South Africa is feeling the influence of shifting global supply dynamics. Import volumes of frozen fries increased in September, although total import tonnages remain lower than 2024. The rise was driven largely by Dutch and Belgian processors, both benefitting from exceptionally strong harvests in Europe. Their record crops have pushed down European export prices, making frozen fries from the European Union more competitive in South Africa.

Average import values were slightly lower than the previous month, landing at around R17.45/kg. This price level reflects the broader global environment of oversupply and discounted offshore stock. Expectations are growing that South Africa will face even stronger import pressure in the weeks ahead, particularly from Northwestern Europe, where processors are holding large stock volumes and seeking relief in export markets.

While South Africa does not face the same extreme oversupply challenges as Europe, the influx of cheaper fry imports presents a significant competitive threat to domestic processors and growers. The situation underscores the importance of monitoring trade flows, adjusting procurement strategies, and supporting local value chain development, especially as global supply remains abundant and pricing continues to soften.

In conclusion

Across continents, the potato industry is grappling with a uniform set of challenges: too many potatoes, too few buyers, and an increasingly volatile economic and political landscape.

From the vast fields of the US to the export hubs of Europe and the processing markets of Asia, producers are contending with falling prices and tightening margins. South Africa, though not a major global exporter, is however deeply affected by these global imbalances through increased competition from low-priced imports.

As the season progresses, it is unlikely that the oversupply problem will resolve quickly. Many countries are entering the storage period with more stock than they can comfortably manage, and demand remains weak.

Growers worldwide are bracing for continued uncertainty, hoping for market stabilisation while preparing for a challenging year ahead. – Francois Strauss, Potatoes SA

For more information, email the author at francois@potatoes.co.za or visit www.potatoes.co.za